John Rathnam, CFA

Rathnam Capital

50 Catoctin Cir, NE, Suite 101

Leesburg, VA 20176

703.245.6662

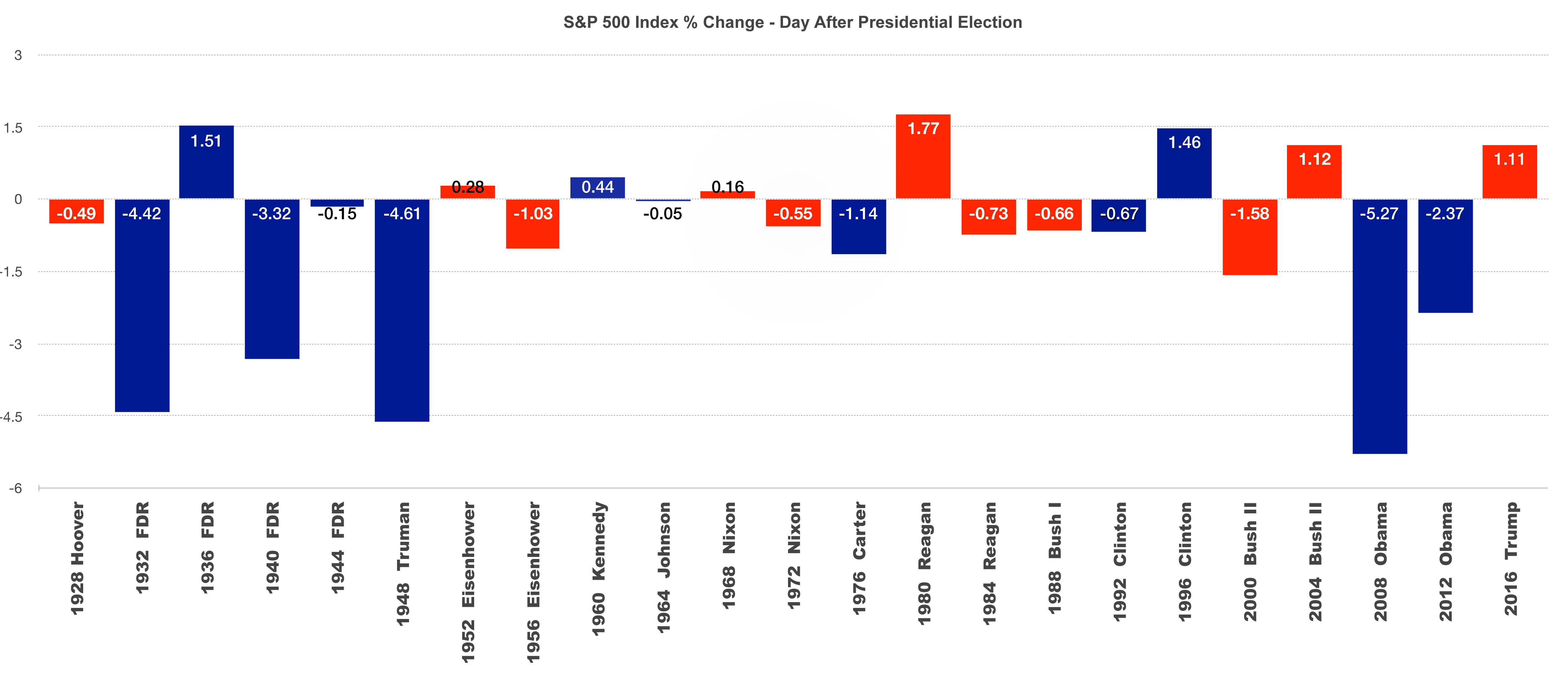

2016 Election Results

The financial markets embraced a Trump victory, sending stock prices to higher levels following a nine day consecutive decline in anticipation of uncertain election results.

U.S. Treasury yields rose dramatically with the expectation that a Trump presidency along with a Republican controlled Congress will inevitably ramp up government spending in order to boost economic growth. During the campaign, Trump was very critical of the Federal Reserve not acting to raise rates soon enough, insinuating political influence.

The Republican win in the Senate and House along with a Republican president means that legislation and laws will flow much more quickly through Congress, rather than running into stalemates as with a divided Congress.

Trump and many republicans have been calling for a rollback of various laws and regulations put in place during the Obama administration. A focal regulatory act is the Dodd-Frank Act, put in place following the financial crisis of 2008/2009, creating immense regulatory costs for the banking sector.

Ratings agency Standard & Poor’s affirmed the investment-grade ‘AA+/A-1+’ rating of U.S. government debt, a day after the presidential election, while maintaining its stable outlook. The agency stated that it will “assume the longstanding institutional strengths and robust checks and balances of the U.S. that will support policy execution in a Trump administration, despite the president-elect’s lack of experience in public office, which raises uncertainty on policy proposals.”