Macro Overview – July 2021 Financial markets are becoming more sensitive to the Delta variant mutation of Covid-19, as some countries in Europe reconsider easing restrictions on businesses and travel. Regardless, global equities finished the 2nd quarter on a positive note and rates stabilized following an upward trending environment earlier in the year. A lack of spending and stay home orders during the pandemic has left millions of consumers with abundant cash hoards, which has been a factor in the recent economic activity occurring nationwide. Some economists and analysts question as to how long it will be until the plentiful cash positions are depleted.

Comments by St. Louis Federal Reserve Bank member James Bullard suggested that there is a “housing froth that seems to be developing” and indicated a pullback on mortgage bond purchases by the Federal Reserve could happen in 2022. Half of existing home buyers in April that took a mortgage out put 20% down, while a quarter of buyers paid cash according to the National Association of Realtors. Cash offers as well as large down payments are pushing some less capable buyers out of the market, consequently forcing many to rent until conditions change.

There is growing concern that the more infectious Delta variant of Covid-19 may evolve into a dominant strain in the U.S. The highly transmissible variant made up 30% of positive samples sequenced in the U.S. for the two-week period ending June 19th according to the U.S. Centers for Disease Control and Prevention. The Delta mutation first emerged in India and has since been spreading worldwide, forcing some countries to reevaluate loosened restrictions on businesses, travel and public events.

An eviction moratorium for tenants set to expire on June 30th was extended to July 31st after a Supreme Court decision. The moratorium was initiated in August by the prior administration to help tenants that were experiencing financial hardships due to Covid-19. Some landlords across the country have consequently seen months of non-payment by some tenants with the inability to evict them. The U.S. Department of Agriculture also extended through July 31st a moratorium on foreclosures from properties financed by USDA Single-Family Housing Direct and guaranteed federal loans.

Data from the Department of Labor revealed that roughly 9 million people that applied for some form of unemployment benefit never received anything despite the largest deployment of economic assistance in U.S. history. Staff shortages, overwhelmed administrative systems, and fraud prevention efforts hindered the unemployment benefits process during the pandemic. The higher costs of crude oil and gasoline will eventually become a burden to company margins and operating expenses. Consumers may eventually be impacted should prices stay elevated for an extended period of time.

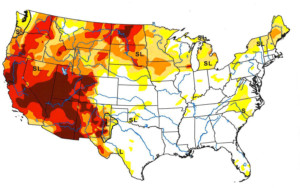

The U.S. Drought Monitor shows that nearly ten percent of the United States is experiencing exceptional drought characteristics as of June 30th. Severe drought conditions are primarily inflicting the western states even as excessive rains pound other parts of the country. Food crops such as wheat, corn and grains are expected to be affected, pushing prices higher in an already inflationary environment. Sources: Dept. of Labor, U.S. Drought Monitor, USDA, National Association of Realtors, Federal Reserve, CDC

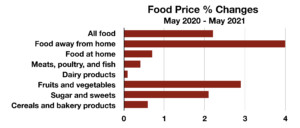

The Cost of Eating Out has Seen the Largest Increase in Years

Equity Indices Post Positive Second Quarter – Domestic Equity Markets

The 2nd quarter ended positively for major global indices, with the S&P 500 index posting gains for 10 of the 11 sectors. Top performing sectors for the quarter included technology, communications, healthcare, and financials.

The SEC said that it is closely monitoring frantic moves in the market caused by memes to determine if there have been any market disruptions, manipulative trading or other misconduct. It also said that it will act to protect retail investors if violations of federal laws are found.

Inflation, higher taxes, and the Delta variant are the focal point of concern for equity markets, especially at recent new highs. There is some momentum in revenue & earnings growth for particular sectors, but not on a broad level.

Sources: S&P, SEC, Bloomberg

Rates Cease Upward Trend – Fixed Income Update

Treasury bond yields stabilized in the 2nd quarter after rising earlier in the year. Short-term rates rose slightly resulting in a flattening yield curve, an indication of possible slower economic growth as the Fed considers raising rates higher.br>

Comments by St. Louis Federal Reserve member James Bullard indicated that the Fed may start increasing rates in 2022 via buying fewer bonds through their asset purchase program. A scale back on mortgage bond purchases is expected to occur initially before pullbacks on other government bonds.br>

Rates on mortgages stood steady at 2.98% for a 30-year fixed conforming loan as of July 1, 2021 as posted by FreddieMac. Other consumer loans also held steady as the Fed deliberated on possible future rate increases.br>

Source: U.S. Treasury, Federal Reserve, FreddieMac

Going Out To Restaurants Has Become Expensive – Food & Dining Update

With the pandemic subsiding and alleviated restrictions enticing consumers to head out, restaurants have seen an enormous surge in business. While many restaurants suffered tremendous setbacks during the height of the pandemic, some have reopened and hired back once laid off employees. Adding to the challenges are increasing costs for food and labor, which have both risen substantially since last year. Consequently, many restaurants are passing along higher costs in the form of more expensive menu prices.

The Bureau of Labor Statistics tracks prices on what consumers use regularly, such as food. What it found is that the costs of eating at restaurants, categorized by the bureau as “food away from home,” had gone up the most relative to other food options.

Source: Bureau of Labor Statistics

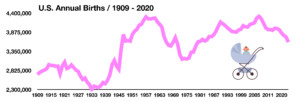

The U.S. BIRTHRATE FELL 4% OVER THE PAST YEAR, THE LARGEST DECLINE SINCE 1973

Births In U.S. Fall Following Pandemic – Domestic Demographics

The Centers for Disease Control and Prevention reported that the U.S. birthrate fell 4% to about 3.6 million births over the past year, the largest decline since 1973.

Births have been declining since the Great Depression as Americans got married later and held off on having children over the decades. The pandemic pronounced the effects of child birth due to the fear of visiting hospitals and lack of child care. Higher costs associated with raising children also inhibited families from growing especially for those that were unemployed during the pandemic.

It is expected that the drop in births due to the pandemic may have long-term consequences for the U.S. population, limiting growth relative to other developed countries. Source: The Centers for Disease Control and Prevention

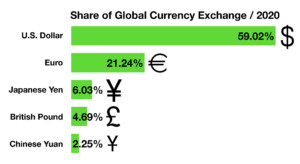

Dollar Share Of Global Exchange Reserves Drops To 25 Year Low – Currency Market Update

For decades the U.S. dollar has been the most dominant of the reserve currencies in the world. The liquidity and transparency of the dollar versus other world currencies has made it the primary reserve currency for foreign governments and international trading entities.br>

Dollar supremacy has recently become more challenged as the U.S. struggles with a growing budget deficit and expanding Treasury debt, which can put downward pressure on a country’s currency. A weakening dollar may also become inflationary for U.S. consumers by limiting purchasing power as well as increased borrowing costs for the U.S. government.br>

The most recent data compiled by the International Monetary Fund (IMF) show the U.S. dollar representing 59% of global exchange reserves, down from 65% in 2016 and the lowest in 25 years. Other expanding economies, such as China’s, have seen their currency gradually increase as a reserve currency status over the past few years.br> Sources: IMF Currency Composition of Foreign Exchange Reserves, Federal Reserve

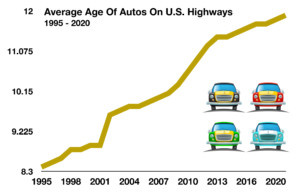

THE AVERAGE AGE OF A CAR ON U.S. HIGHWAYS IS NOW 12 YEARS OLD

It May Be Time To Review Homeowners Insurance Coverage – Consumer Awareness

As home values have increased, so has the need to review insurance policies to be certain that appropriate coverage is in force. It is recommended that homeowners review their current coverage on their insurance policies in order to avoid under coverage circumstances.

When reviewing homeowners insurance, there are two basic types of coverage: replacement cost and market value. Replacement cost is the cost necessary to replace your entire home based on an estimated replacement cost. Market value is the amount that a buyer would pay to purchase your home and property in its current condition.

Replacement cost is preferred because it takes into account current material costs that may not be reflected in a market value. Over the past year, the pandemic drove the costs of lumber and copper significantly higher, increasing replacement costs. Homeowners that plan to stay put and not sell should review their policies for appropriate coverage.

Source: Consumer Financial Protection Bureau, U.S. Bureau of Labor Statistics; Producer Price Index by Commodity: Lumber and Wood Products: Softwood Lumber

Average Age Of Autos On U.S. Highways Reaches 12 Years Old – Automotive Market Overview

Circumstances over the past year have driven prices for used and new cars higher, shifting consumer buying behavior. Supply constraint issues for critical components needed for autos and light trucks have made it extremely difficult to purchase new automobiles. As a consequence, demand and prices for used cars has also gone up, leaving many drivers to hold on to their existing cars.

The Bureau of Transportation Statistics identified that the average age of vehicles on U.S. highways is now 12 years old, a reflection of drivers holding on to their cars longer. Improvements in technology and efficiency over the decades has allowed more automobiles to reach higher mileage and keep running.

Source: Bureau of Transportation Statistics

GASOLINE ROSE ROUGHLY 50% OVER THE PAST YEAR

How Inflation Creeps Up On Consumers – Consumer Behavior

Over the past year, global economies went from a slow expansion at the beginning of 2020, to an abrupt halt with the onset of the pandemic in March 2020. Supply chain bottlenecks have become rampant as increasing demand has evolved from a slowly recovering global economy.

Historically, rising producer prices have been a predecessor to consumer inflation when manufacturers and distributors pass along the higher cost of materials and labor to consumers in the form of higher retail prices.

A lack of critical components for everything from automobiles to cellular phones brought about production shortages that led to decreases in supply simultaneously as demand fell across the globe. As demand has begun to rekindle, shuttered factories and supply chains have not been able to keep up with rising demand, resulting in order backlogs and higher prices.

Some economists believe that current inflationary pressures may be temporary until production ramps up to meet current demand, while others believe that higher prices have become permanent for many products in order to maintain delicate margins. Source: Bureau of Economic AnalysisWhat To Do With That

USPS Struggling – Government Agency Overview

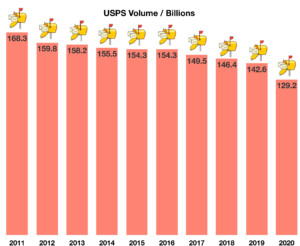

The United States Postal Service (USPS) remains an integral part of the economy and the country’s infrastructure even as the popularity of electronic payments and digital transactions have dramatically reduced the volume of mail processed by the USPS.

Of the more than 129 billion pieces of mail delivered in 2020, the most widely used service of the USPS is its first class mail service. As the volume of all mail has been dwindling, so has first class mail, falling from over 103 billion pieces in 2000 to just over 52 billion pieces in 2020, roughly a 50% drop in twenty years.

As the volume has decreased, so have the number of postal employees. There were nearly 700,000 postal employees in 2006, falling to less than 496,000 in 2020. There have been numerous rate increases over the years, with the most recent rate increase up to 55 cents for a 1 ounce letter in January 2019.

Source: USPS

GRANDPARENTS CAN CONTRIBUTE UP TO $15,000 PER YEAR PER GRANDCHILD

Unused Travel Budget – Financial Planning

As millions of Americans stayed home during the pandemic and traveled nowhere as hotels, resorts, and restaurants closed, budgets created for travel and vacation went idle. Many are still deterred, if not discouraged, to travel in fear of another virus outbreak or simply out of paranoia. Travel has become a bit more complicated and burdensome, especially for the elderly who just don’t travel as easily as during their younger years.

With inflation the topic of concern, higher educational costs are an issue for recent grads. A consideration might be to migrate some of the idle funds in the travel budget to a grandchild’s college saving’s plan, such as a 529. Named after the IRS Code it falls under, Section 529 plans have amassed over $425 billion in assets since their inception in 1997. Their popularity soared over the years as parents and grandparents realized their favorable tax benefits while also saving for college expenses.

These plans offer two primary benefits: assets grow tax deferred and come out tax free for qualified expenses; and, contributions made by parents and grandparents are considered a gift, thus proving a tax benefit for some contributors. Over the years, both wealthy and lower-income parents and grandparents have been the main contributors to these plans.

Any parent or grandparent can make gifts of up to $15,000 per year per individual person (child) and to as many individuals as they wish. Section 529 plans allow gifts to be made five years ahead all at once. Thus, a grandparent can gift $75,000 per grandchild at once for the next five years. If the grandparent has five grandchildren, then they have the ability to contribute $375,000 at once to the 529 plans, which are considered gifts. There would be no gift tax, assuming no other gifts were made to that child over those years.

Such generous contributions allow a reduction in the contributor’s taxable estate. This is an ideal strategy for parents and grandparents that may have estates valued at over $11.7 million, the current federal estate tax exemption level. The federal estate tax exemption, that’s the amount an estate can leave to heirs without having to pay federal estate tax, is $11.7 million for 2021. Source: www.irs.gov/businesses/small-businesses-self-employed/estate-tax

Job Openings Surpass 8 Million – Labor Market Update

A growing demand for workers by eager companies to fill positions nationwide has led to unfilled job openings exceeding 8 million as of the end of March, according to the most recent data available from the Department of Labor. Economists and analysts believe that generous unemployment benefits along with stimulus payments have discouraged many of the unemployed from returning to work. Lower paying job positions are the toughest to fill as unemployment payments equal if not exceed regular pay.

Various occupations in manufacturing, hospitality, transportation, and food services have seen the largest growth in openings since the pandemic began in March 2020. Some companies have announced higher wages and increased hourly pay in order to entice workers, yet still struggle to fill open positions.

Sources: U.S. Department of Labor, BLS

HOME PRICES ROSE ROUGHLY 12% FROM FEBRUARY 2020 TO FEBRUARY 2021

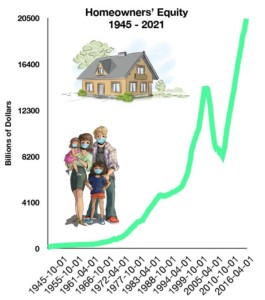

Home Equity Surpasses $21 Trillion – Housing Market Overview

With home prices rising roughly 12% from February 2020 to February 2021, equity levels have risen producing heightened wealth among millions of homeowners. Elevated equity has allowed homeowners to remodel and improve existing homes, resulting in further home value increases.

A tight supply of homes nationwide has added to rising home values as growing demand for homes has produced multiple offers on homes. The lack of inventory has also locked homeowners into their homes for longer periods as they upgrade and modernize.

A closely followed gauge of housing prices tracked by the Federal Reserve, the S&P/Case-Shiller U.S. National Home Price Index, rose the most in 15 years, sending home prices to new highs throughout most of the country. The data also found that the lack of new homes spurred heightened demand for previously owned home

s. The acceleration of prices for previously owned homes versus new homes hasn’t occurred in 15 years. Such elevated prices reflect a historically low level of homes available for sale nationwide. Some economists identify the rapid rise in home prices as inflationary, while the Fed has dismissed the rise as merely transitory due to effects brought about by the pandemic.

The pandemic, which triggered a migration from cities to suburbs throughout the country, has propelled home prices higher as a lack of inventory has not kept up with rising demand.

Rising home values translate into rising equity for homeowners, which in-turn enhances household wealth, credit availability and consumer confidence. Economists view these characteristics as supportive for an economic recovery, allowing for more borrowing and spending.

Source: Federal Reserve; //fred.stlouisfed.org/series/CSUSHPINSA

Equities Maintain Some Upward Momentum – Domestic Stock Market Overview

Strong earnings and economic data helped propel equities higher in April, along with abundant liquidity provided by the Fed in the form of bond buying and continued low rates. Strengthening economic data has also helped maintain equity valuations, anticipating expanding growth across the economy.

The anticipated effects of the proposed increases in capital gains may be muted since roughly 25% of U.S. stocks are in taxable accounts, while the balance are in retirement and pension accounts where capital gains tax is not applicable.

Higher prices on numerous consumer products are leading to rising margins for many companies, translating into elevating earnings and stock prices. Comments by Fed Chair Jerome Powell on April 28th suggested that parts of the market “are a bit frothy”, alluding to some overpriced valuations.