Ocean Park Capital Management

2503 Main Street

Santa Monica, CA 90405

Main: 310.392.7300

Daily Performance Line: 310.281.8577

Stock Indices:

| Dow Jones | 47,716 |

| S&P 500 | 6,849 |

| Nasdaq | 23,365 |

Bond Sector Yields:

| 2 Yr Treasury | 3.47% |

| 10 Yr Treasury | 4.02% |

| 10 Yr Municipal | 2.74% |

| High Yield | 6.58% |

YTD Market Returns:

| Dow Jones | 12.16% |

| S&P 500 | 16.45% |

| Nasdaq | 21.00% |

| MSCI-EAFE | 24.26% |

| MSCI-Europe | 27.07% |

| MSCI-Emg Asia | 26.34% |

| MSCI-Emg Mkt | 27.10% |

| US Agg Bond | 7.46% |

| US Corp Bond | 7.99% |

| US Gov’t Bond | 7.17% |

Commodity Prices:

| Gold | 4,253 |

| Silver | 57.20 |

| Oil (WTI) | 59.53 |

Currencies:

| Dollar / Euro | 1.15 |

| Dollar / Pound | 1.32 |

| Yen / Dollar | 156.21 |

| Canadian /Dollar | 0.71 |

Portfolio Overview

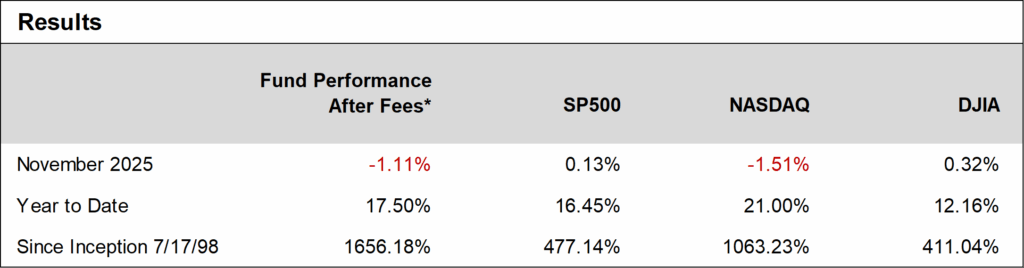

Ocean Park Investors Fund declined 1.11%* in November, modestly ahead of the NASDAQ Composite (down 1.51%) and behind the S&P 500 (up 0.13%). A broad downdraft in technology stocks impacted the portfolio, as investors took profits in crowded AI and growth names. The fund’s position in Lumentum was a notable exception, gaining 61% on a strong earnings beat, as well as higher guidance tied to AI and cloud‑optics demand, and several analyst upgrades.

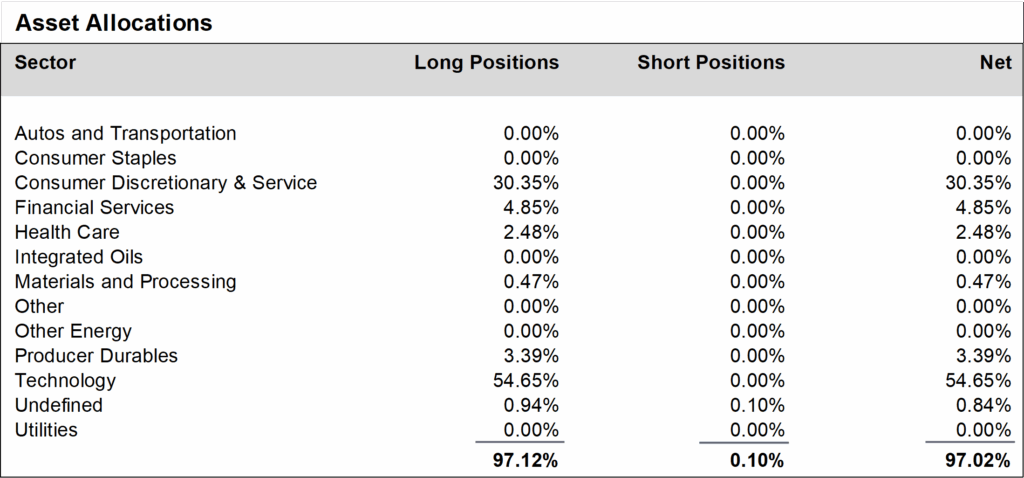

The Fund’s November results reflected a mix of earnings-driven volatility in several growth holdings and active repositioning around analyst estimate revisions and guidance changes. During the month, we trimmed or exited positions in Axon, HubSpot, Disney, Celsius, and selected semiconductors after disappointing or mediocre earnings reports and guidance. We replaced them with positions in companies where analysts raised earnings estimates meaningfully higher, including ASML, Seagate Technology, Ross Stores, CrowdStrike, and Morgan Stanley. We finished the month at about 97% net long, unchanged from October.

Daily updates on our activity are available on our Results Line, at 310-281-8577, and on our website at www.oceanparkcapital.com. Enter password opcap.

*These results are pro forma. Actual results for most investors will vary. Additional disclosures on page 4. Past performance does not guarantee future results.