Stock Indices:

| Dow Jones | 38,996 |

| S&P 500 | 5,096 |

| Nasdaq | 16,091 |

Bond Sector Yields:

| 2 Yr Treasury | 4.64% |

| 10 Yr Treasury | 4.25% |

| 10 Yr Municipal | 2.53% |

| High Yield | 7.63% |

YTD Market Returns:

| Dow Jones | 3.47% |

| S&P 500 | 6.84% |

| Nasdaq | 7.20% |

| MSCI-EAFE | 2.23% |

| MSCI-Europe | 1.23% |

| MSCI-Pacific | 3.98% |

| MSCI-Emg Mkt | -0.27% |

| US Agg Bond | -1.68% |

| US Corp Bond | -1.67% |

| US Gov’t Bond | -1.59% |

Commodity Prices:

| Gold | 2,051 |

| Silver | 22.87 |

| Oil (WTI) | 78.25 |

Currencies:

| Dollar / Euro | 1.08 |

| Dollar / Pound | 1.26 |

| Yen / Dollar | 150.63 |

| Canadian /Dollar | 0.73 |

Macro Overview

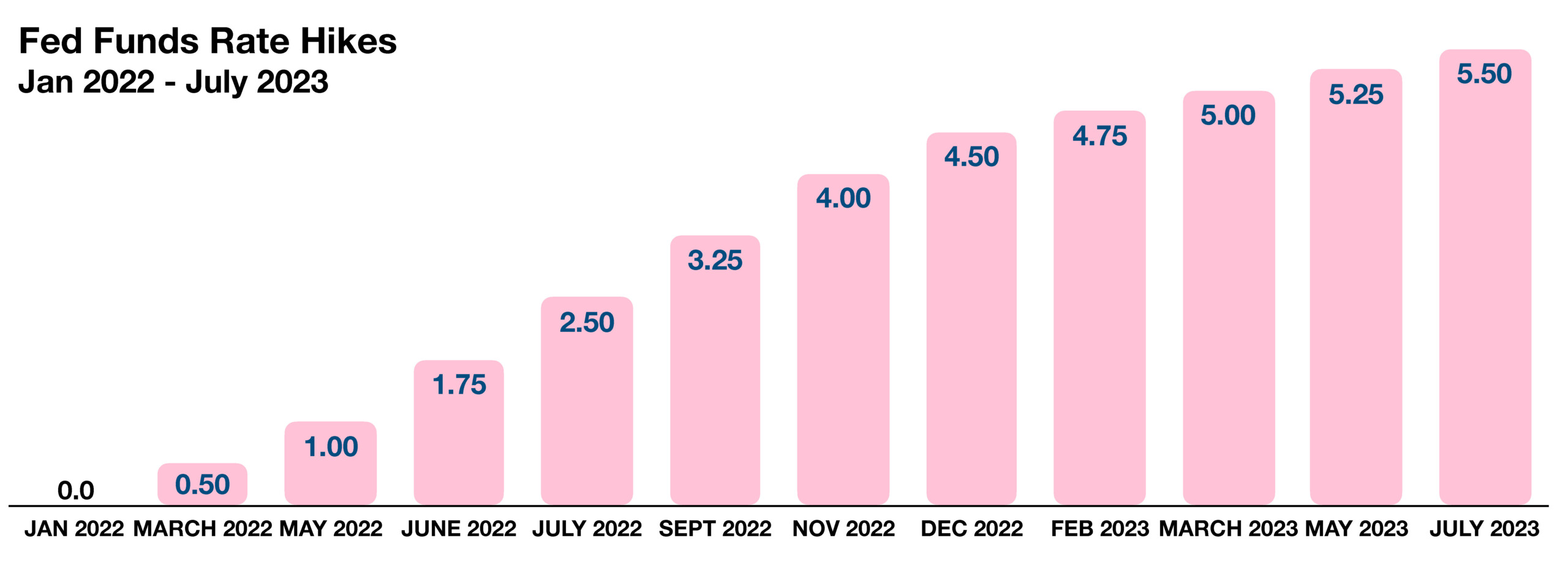

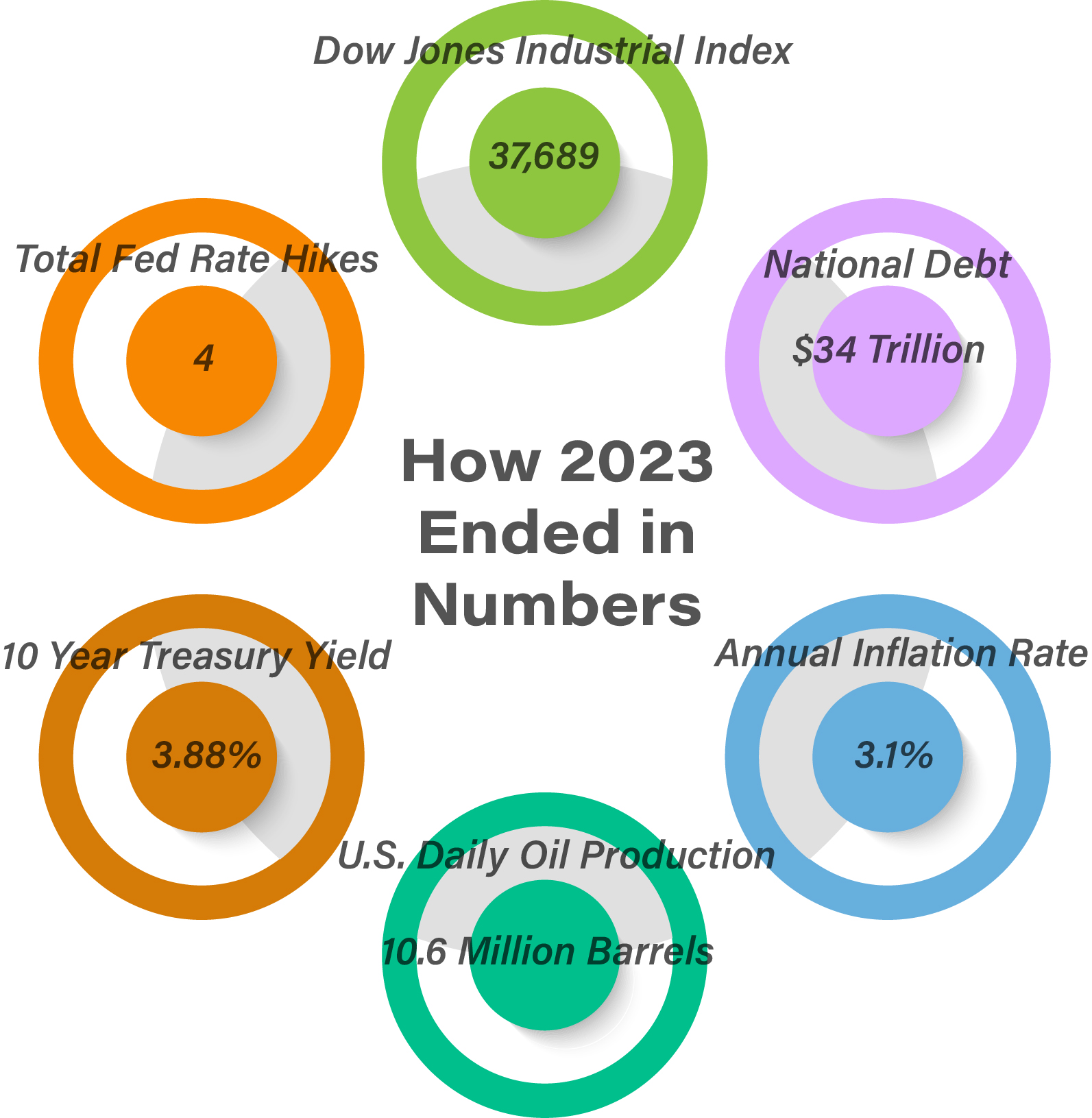

Last year witnessed one of the most ambitious executions of interest rate hikes by the Federal Reserve in history, with rates increased four times in 2023. Optimism dominated markets as equities and bonds rose in a rare positive correlation. Stocks and bonds historically tend to drift in opposite directions.

Inflation-focused concerns in 2023 led to deflationary concerns heading into 2024. The Federal Open Market Committee’s vigilance in combating inflationary pressures translated into hard-landing concerns as recession fears evolved due to rising rates. A robust labor market continues to challenge the FOMC’s potential easing policy in 2024, as wage pressures continue to abound.

Geopolitical tensions continued from 2023, as the invasion of Ukraine and the Middle East conflict weigh on financial markets. The hostilities hinder supply routes in various regions and fuel economic uncertainty. Russia’s invasion of Ukraine directly affects Europe, while the Middle East conflict impacts oil shipping throughout the region.

Bank failures at the beginning of 2023 made for one of the worst years for bank collapses in history. Three of the top five bank failures ever occurred in 2023, as the demise of Silicon Valley Bank, Signature Bank, and First Republic Bank totaled over $350 billion in assets.

Analysts note that the performance of the S&P 500 Index in 2023 may not be truly representative of comprehensive market characteristics, due to a concentration in just seven stocks known as the magnificent seven. Roughly half of the performance for the S&P 500 Index in 2023 was attributable to these seven stocks, with the remaining 493 stocks in the index representing the balance of the return for 2023.

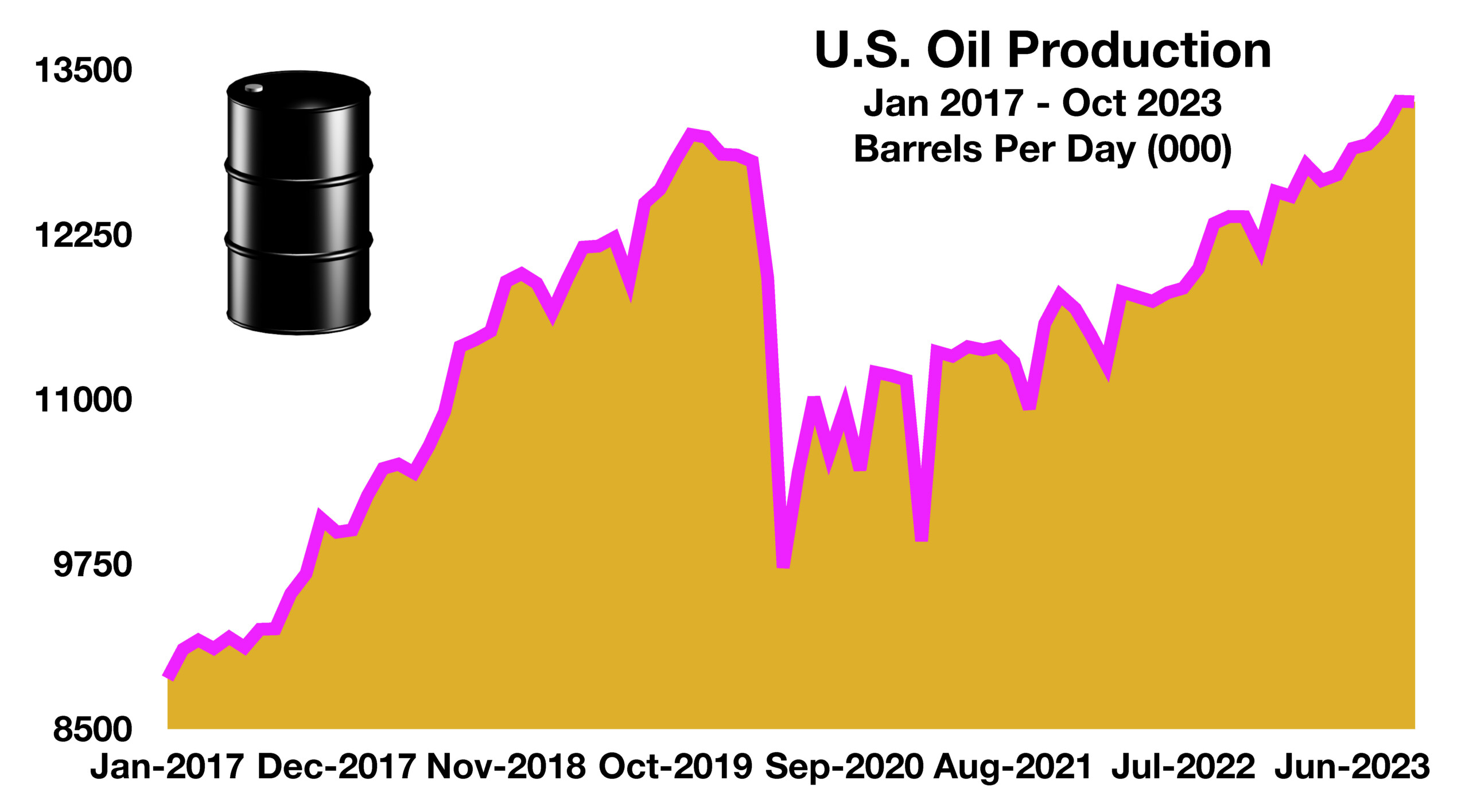

The U.S. exported approximately 75% of total domestic oil production in 2023, supplying both developed and emerging countries worldwide. Supply constraints for oil may pose a challenge as a result of worsening shipping disruptions in the Middle East, affecting prices globally.

Total Federal Debt for the U.S. reached $34 trillion at the end of 2023, up from $27.6 trillion at the beginning of 2021. Rising rates added debt costs for the U.S. government, as interest expense on outstanding U.S. debt increased substantially. (Sources: Fed, BEA, Treasury Dept., EIA)