Sustainable Income Planning | Investments | Retirement

MFA 2025 Winter

Market Update

(all values as of 04.30.2025)

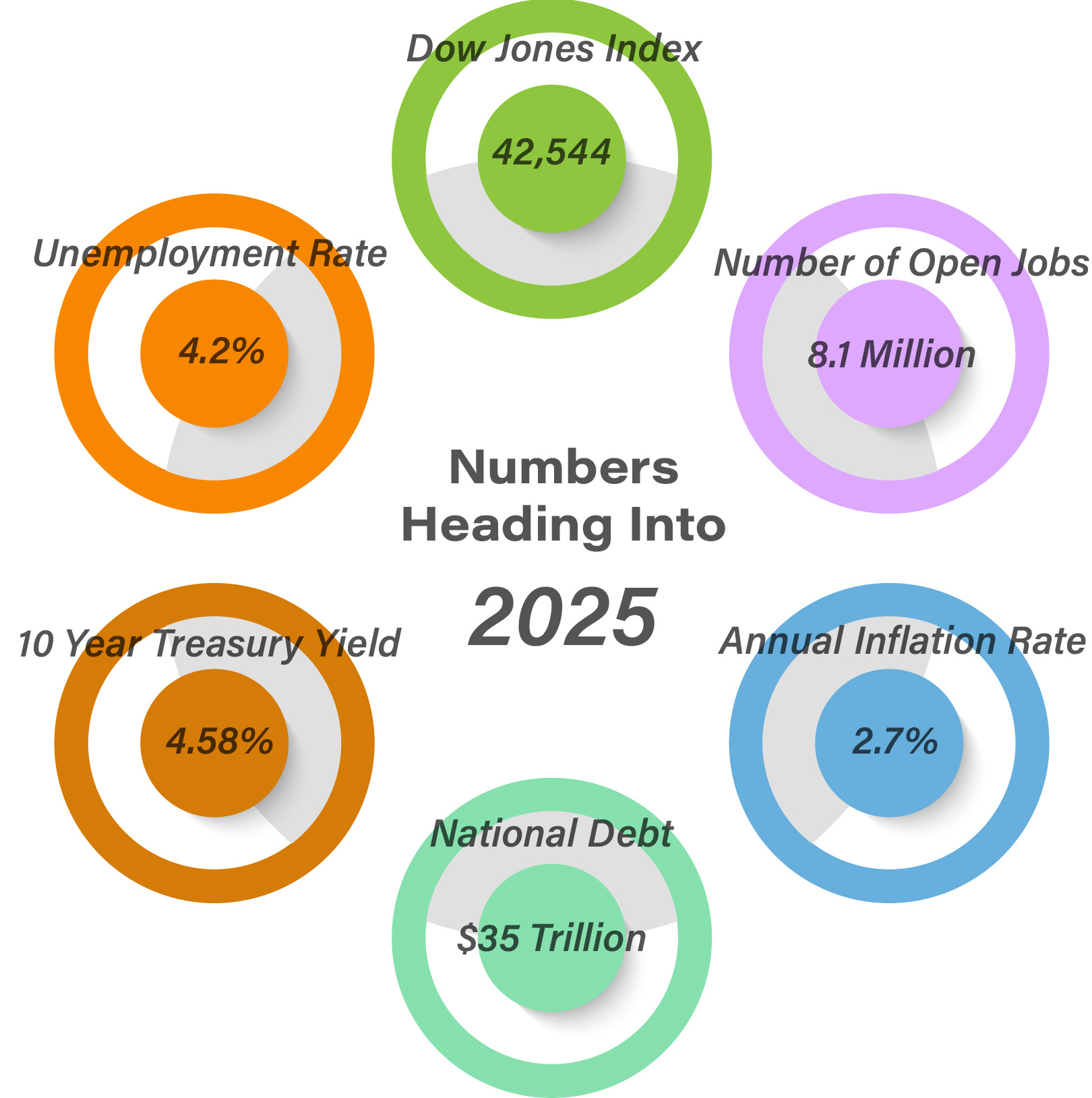

Stock Indices:

Dow Jones

40,669

S&P 500

5,569

Nasdaq

17,446

Bond Sector Yields:

2 Yr Treasury

3.60%

10 Yr Treasury

4.17%

10 Yr Municipal

3.36%

High Yield

7.69%

YTD Market Returns:

Dow Jones

-4.41%

S&P 500

-5.31%

Nasdaq

-9.65%

MSCI-EAFE

12.00%

MSCI-Europe

15.70%

MSCI-Pacific

5.80%

MSCI-Emg Mkt

4.40%

US Agg Bond

3.18%

US Corp Bond

2.27%

US Gov’t Bond

3.13%

Commodity Prices:

Gold

3,298

Silver

32.78

Oil (WTI)

58.22

Currencies:

Dollar / Euro

1.13

Dollar / Pound

1.34

Yen / Dollar

142.35

Canadian /Dollar

0.72

“Predictions are difficult, especially about the future” – Neils Borh, Nobel laureate in Physics and father of the atomic model

Dear Friends,

I’m going to start with a few predictions. I’m sure I’ll be wrong in many ways.

Powder is more fun with friends.

The US Economy will continue to grow, which will provide support to risk assets like stocks and real estate. Whatever you may think of Trump as a person, Wall Street analysts are convinced he will be great for stocks over the next 12 months.

Financial Flexibility will become the new buzzword in retirement planning. It means having access to your money when you want it without sacrificing your goals or incurring penalties. It’s what we do and it is what creates happy clients.

Inflation will not come down on the things you want it to. This is the new normal and we need to plan for it.

Using social media or otherwise letting a computer decide what you see online will generally not make you happier or smarter. Free speech is important, and fake news is here to stay.

Cybercrime will be the greatest threat to your money and time. The Treasury Department confirmed reports that it was hacked by China last December and you could be next! Install a Password Manager today! Dashlane, 1Password, and Lastpass are the most popular and reliable. Call me if you ever suspect you are being scammed.

Rates will continue to be high and periodically cause sell-offs in the market. Last year, escalating federal deficits and expanding government debt issuance rattled the U.S. Treasury debt market, sending Treasury yields higher. This drama will continue.

Happy 2025! I hope to help make it a great one for you.

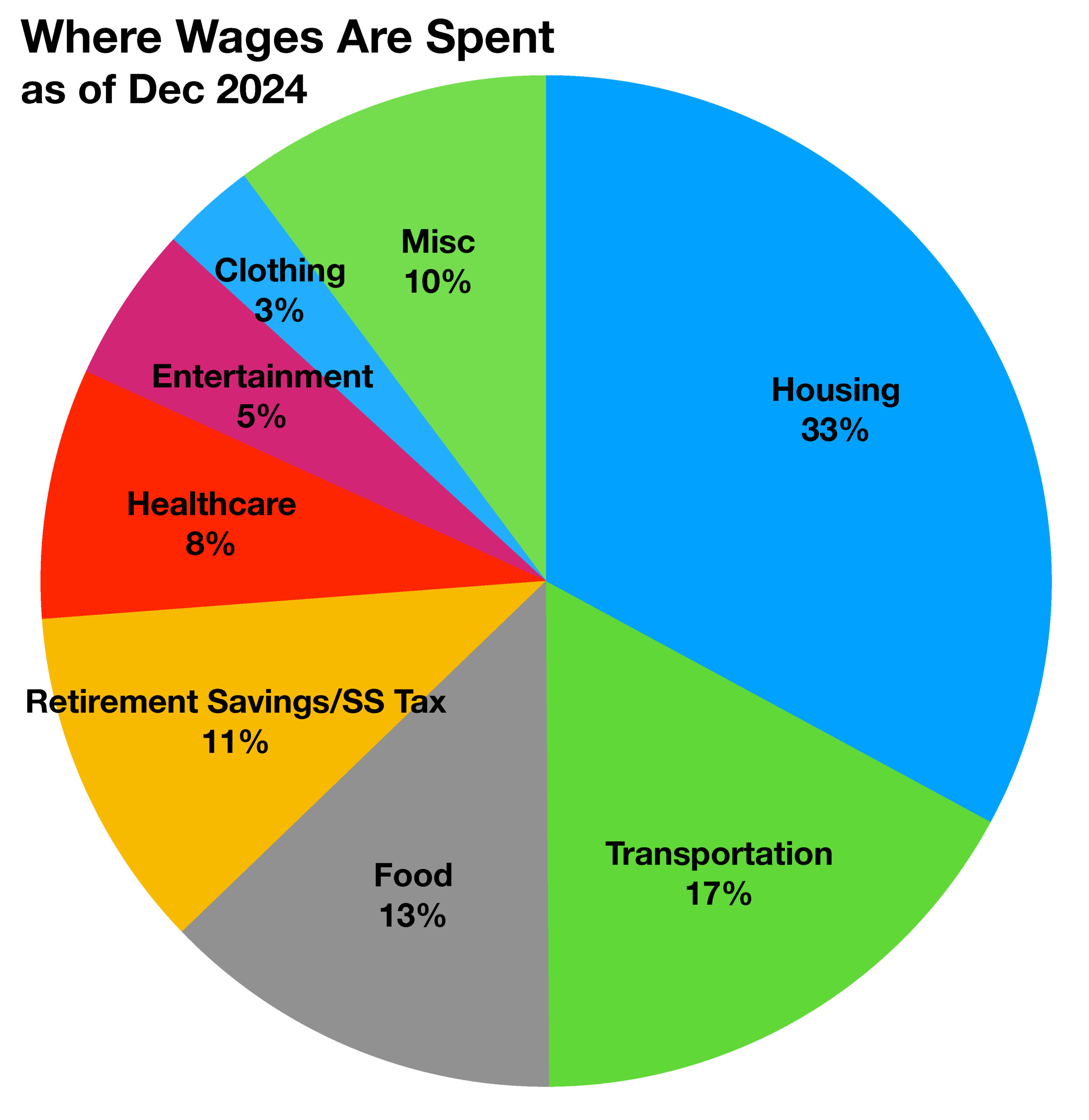

The average American household spends about 32.9% of their income on housing

Rates End Year With Uncertainty – Fixed Income Overview

Tensions rose surrounding the Treasury market as the weighted average interest rate on outstanding Treasury debt is currently around 3.3%, a 15-year high. Additional Treasury debt issuance has become a contention as weakened demand for new bonds became more apparent.

Bond yields were challenged throughout 2024 as uncertainty surrounding the Fed’s decision to reduce rates lingered. The Fed’s initial rate reduction in September 2024 was the commencement of additional rate cuts over the next couple of years. Inflation data will be the primary driver of the Fed’s trajectory for rate cuts in 2025. (Sources: Treasury Dept., Federal Reserve)

Equity Indices Enter 2025 With Hesitation – Domestic Equity Update

Equity indices finished 2024 with gains across all eleven sectors of the S&P 500 Index. The communication services, financials, consumer discretionary, and the utilities sector saw the largest gains in 2024.

Equity indices hesitated their upward trend in December as inflation data hindered the Fed from reducing rates more aggressively. Analysts will be focused on earnings and cabinet appointments whose influence on company directives and initiatives can be critical. (Sources: S&P, Bloomberg, Dow Jones, Nasdaq)

Percentage of Average Wage Going Towards Housing Highest Since 2007 – Housing Market Update

A persistent shortage of housing along with elevating mortgage rates and rising insurance costs have made the cost of home ownership and renting excessive for many. The percentage of income spent on housing has increased significantly in recent years, making affordability a major concern for many households.

The average American household spends about 32.9% of their total earnings on housing costs. However, this figure can vary widely depending on location and whether someone rents or owns their home. Some parts of the country command much higher housing and rental costs than other parts of the country, thus encompassing varied percentages on how much is spent on housing relative to income. Additionally, incomes also vary among various states and cities contingent on demographics.

It has been generally recommended spending no more than 30% of gross income on housing costs, a guideline known as the “30% rule”. The guideline has been a standard benchmark for decades, however, it may now be considered outdated and overly simplistic today.

Sources: Department of Labor

The U.S. government holds more than $13 billion in bitcoin

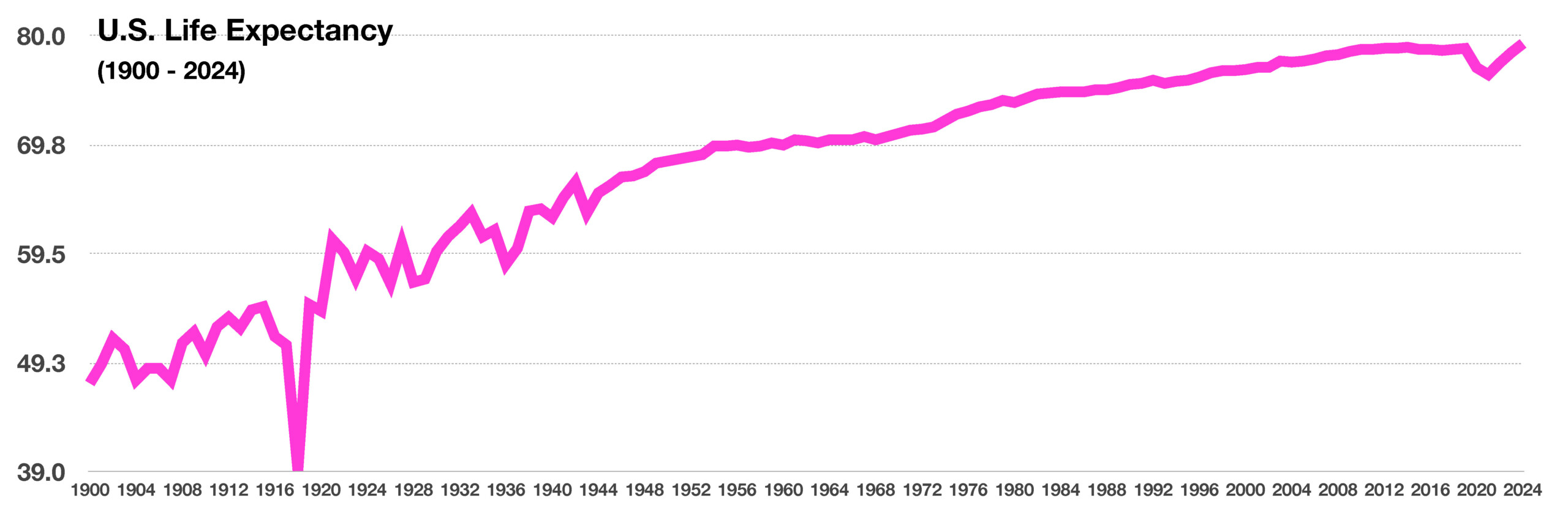

U.S. Life Expectancy Rates Increased To Highest Level Since Pandemic – Health & Well Being

Recently released data by the Center of Disease Control and Prevention reveal that life expectancy in the U.S. increased to 79.3 years in 2024. During the pandemic, life expectancy fell as the three leading causes of death in 2020 were heart disease, cancer and Covid-19. Life expectancy for all Americans in 2019 was 78.8 years, falling to 77 years in 2020. Those aged 85 and older saw the most deaths, many experiencing medical complications from Covid-19. In 2020, Covid related deaths exceeded deaths caused by strokes, Alzheimers, diabetes, and kidney disease.

The U.S. Department of Health & Human Services tracks factors contributing to life expectancy including age, gender and race. The most recent data revealed that females are estimated to live to age 83.8 while males are expected to live to 76.1, a seven year difference.

Medical advancements and safer living conditions over the decades have led to a gradual increase in life expectancy. In 1860, life expectancy in the United States was 39, increasing to 69 in 1960, representing a 30 year life span increase in 100 years. (Sources: U.S. Department of Health & Human Services, CDC)

Imports & Tariffs – Domestic Trade Policy

As the president-elect prepares to enter the White House, foreign imports into the U.S. have become a leading agenda item. According to the Commerce Department, the top imports into the U.S. include electronic devices such as mobile phones, computers and TVs, followed by machinery and automobiles. The onset of additional tariffs and import duties might change the makeup of imports dramatically, as consumers tackle higher prices along with some manufacturing possibly shifting to the U.S.

The biggest question everyone has is, how will higher tariffs affect U.S. consumers and the economy. The most dominant imports currently tend to be high margin products such as mobile phones, laptops, and computers. Any additional tariffs might either be partially absorbed by the exporters or passed along to consumers in the form of higher prices. What’s interesting is that the onset of cheap Chinese made products have actually altered consumer behavior in the U.S. over the past twenty years. Before inexpensive TVs made their way into electronic superstores, a typical TV would last years. Today, TVs are considered disposable and are easily replaceable. Should import prices rise, consumers might reconsider replacing products regularly, and instead maintain existing products for longer periods. (Source: Department of Commerce)

life expectancy in the U.S. increased to 79.3 years in 2024

Looking to reduce your taxes through charitable giving? If you received a windfall that is putting you in a higher bracket, you may be able to give to causes you care about and save money on taxes at the same time. Call us if you want to learn more.

About Us

Our clients enjoy the feeling of having their financial lives kept in order. Freedom from worry comes from working with an experienced advisor that understands your entire financial life and is accessible and attentive to your needs. As a fiduciary, Mike is unable to receive commissions from financial products and free to make recommendations that are unbiased by Wall Street. With over a decade of experience caring for a small family of clients, our specialties are preserving wealth and generating sustainable income. Our average client net worth ranges from $5 to $30 Million. Go outside, we’ve got this.

Cancel or move to digital? mike@mccormickfinancialadvisors.com with your preference. No worries!