Ocean Park Capital Management

2503 Main Street

Santa Monica, CA 90405

Main: 310.392.7300

Daily Performance Line: 310.281.8577

Stock Indices:

| Dow Jones | 49,652 |

| S&P 500 | 7,209 |

| Nasdaq | 24,892 |

Bond Sector Yields:

| 2 Yr Treasury | 3.88% |

| 10 Yr Treasury | 4.40% |

| 10 Yr Municipal | 2.96% |

| High Yield | 6.87% |

YTD Market Returns:

| Dow Jones | 3.31% |

| S&P 500 | 5.31% |

| Nasdaq | 7.10% |

| MSCI-EAFE | 5.04% |

| MSCI-Europe | 2.95% |

| MSCI-Far East | 9.09% |

| MSCI-Emg Mkt | 13.94% |

| US Agg Bond | 0.07% |

| US Corp Bond | -0.09% |

| US Gov’t Bond | -0.08% |

Commodity Prices:

| Gold | 4,641 |

| Silver | 74.65 |

| Oil (WTI) | 105.76 |

Currencies:

| Dollar / Euro | 1.16 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 159.95 |

| Canadian /Dollar | 0.73 |

Portfolio Overview

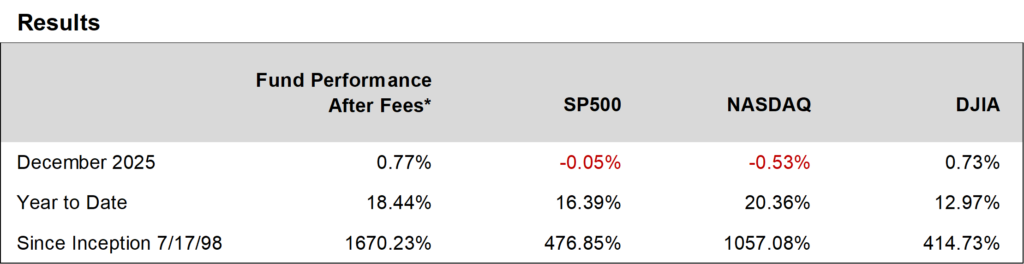

Ocean Park Investors Fund delivered solid returns in 2025, gaining 18.44%* for the year while the S&P 500 gained 16.39% and the NASDAQ Composite gained 20.36%.

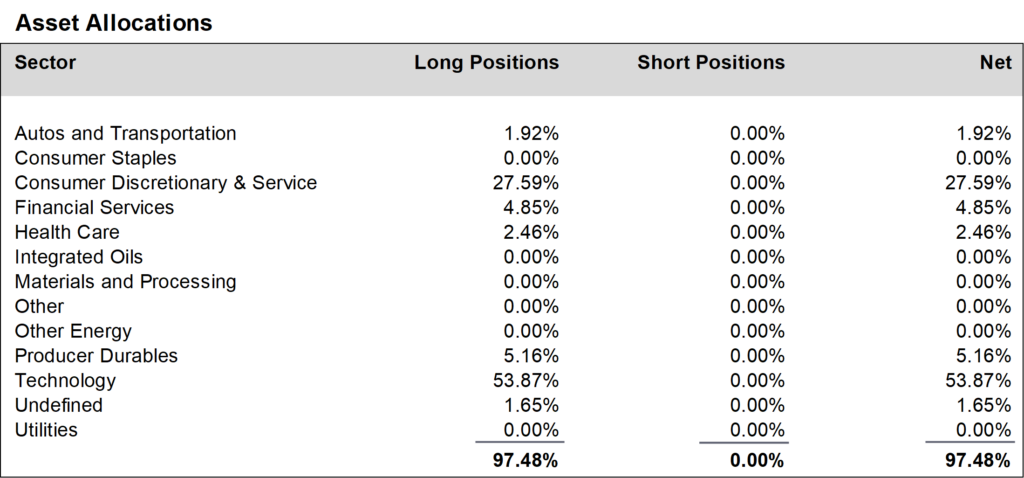

Our investment approach remains unchanged: identifying companies whose earnings are likely to exceed consensus expectations. In recent years, we have further concentrated the portfolio toward our highest-conviction opportunities in businesses benefiting from technological innovation, reducing the number of holdings from 64 at the end of 2022 to 44 by the end of 2024. This focus on fewer, higher-conviction positions has served our investors well and contributed to one of the strongest multi-year performance periods in the Fund’s history.

In December, the Fund rose 0.77%* while the S&P 500 declined 0.05% and the NASDAQ Composite declined 0.53%. The month was characterized by modest volatility and continued sector rotation as investors repositioned heading into year-end.

We remain grateful for your investment in the Fund as we work to build on our long-term performance and earn your continued confidence.

Daily updates on our activity are available on our Results Line, at 310-281-8577, and on our website at www.oceanparkcapital.com. Enter password opcap.

*These results are pro forma. Actual results for most investors will vary. Additional disclosures on page 4. Past performance does not guarantee future results.