Stock Indices:

| Dow Jones | 44,130 |

| S&P 500 | 6,339 |

| Nasdaq | 21,122 |

Bond Sector Yields:

| 2 Yr Treasury | 3.94% |

| 10 Yr Treasury | 4.37% |

| 10 Yr Municipal | 3.27% |

| High Yield | 6.86% |

YTD Market Returns:

| Dow Jones | 3.73% |

| S&P 500 | 7.78% |

| Nasdaq | 9.38% |

| MSCI-EAFE | 15.67% |

| MSCI-Europe | 18.44% |

| MSCI-Pacific | 10.55% |

| MSCI-Emg Mkt | 15.60% |

| US Agg Bond | 3.75% |

| US Corp Bond | 4.24% |

| US Gov’t Bond | 3.72% |

Commodity Prices:

| Gold | 3,346 |

| Silver | 36.79 |

| Oil (WTI) | 69.38 |

Currencies:

| Dollar / Euro | 1.15 |

| Dollar / Pound | 1.33 |

| Yen / Dollar | 148.58 |

| Canadian /Dollar | 0.72 |

Macro Overview

Economists note that the Fed’s reluctance to lower rates may jeopardize economic momentum as consumer expenditures continue to be sensitive to elevated interest rates. The most recent Consumer Price Index (CPI) data confirms that inflation has been steadily falling for the past year, while unemployment has slowly increased since the beginning of 2024. The Federal Reserve determines adjustments in rates primarily based on inflation and employment data.

Consumers will likely see higher prices as tariffs work through inventories and some companies begin to pass the costs on to consumers. Inventories with assessed tariffs are expected to reach consumers by fall of this year, if not this summer. Some retailers have thus far absorbed most of the costs from tariffs, which has resulted in smaller profit margins for companies, helping to alleviate inflationary pressures in the near term.

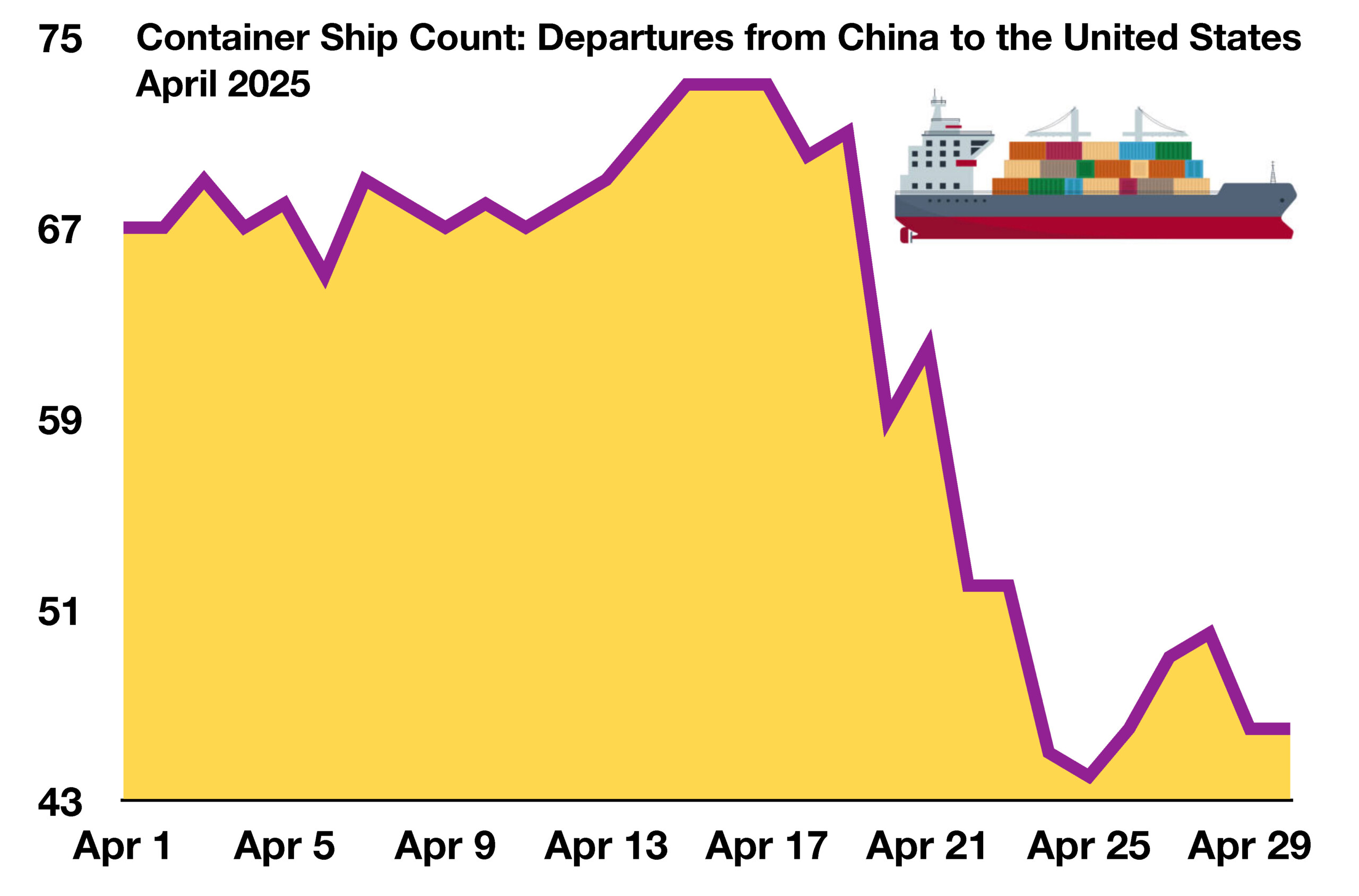

Equity markets received some reprieve in May as the U.S. administration agreed to a provisional trade deal with China and the implementation of many tariffs were postponed for 90 days. Due to volatile markets and growing concerns among allies, the President is widely expected to extend tariff negotiations as the administration searches for trade deals with allies and adversaries alike.

U.S. government debt was downgraded by credit-rating agency Moody’s, stripping the U.S. of its last remaining triple-A credit rating from a major rating firm. The downgrade follows similar downgrades by Fitch in 2023 and S&P in 2011. The downgrade may raise the cost of borrowing for the U.S. federal government.

Labor department data revealed that consumer spending rose 1.2%, down from an initial estimate of 1.8%, the weakest pace in almost two years. Major retailers reported that consumers have become more price-sensitive and value-oriented over the past few months. Several economists believe that the Federal Reserve’s stance to hold rates steady is a deterrent to already-strained consumer expenditures.

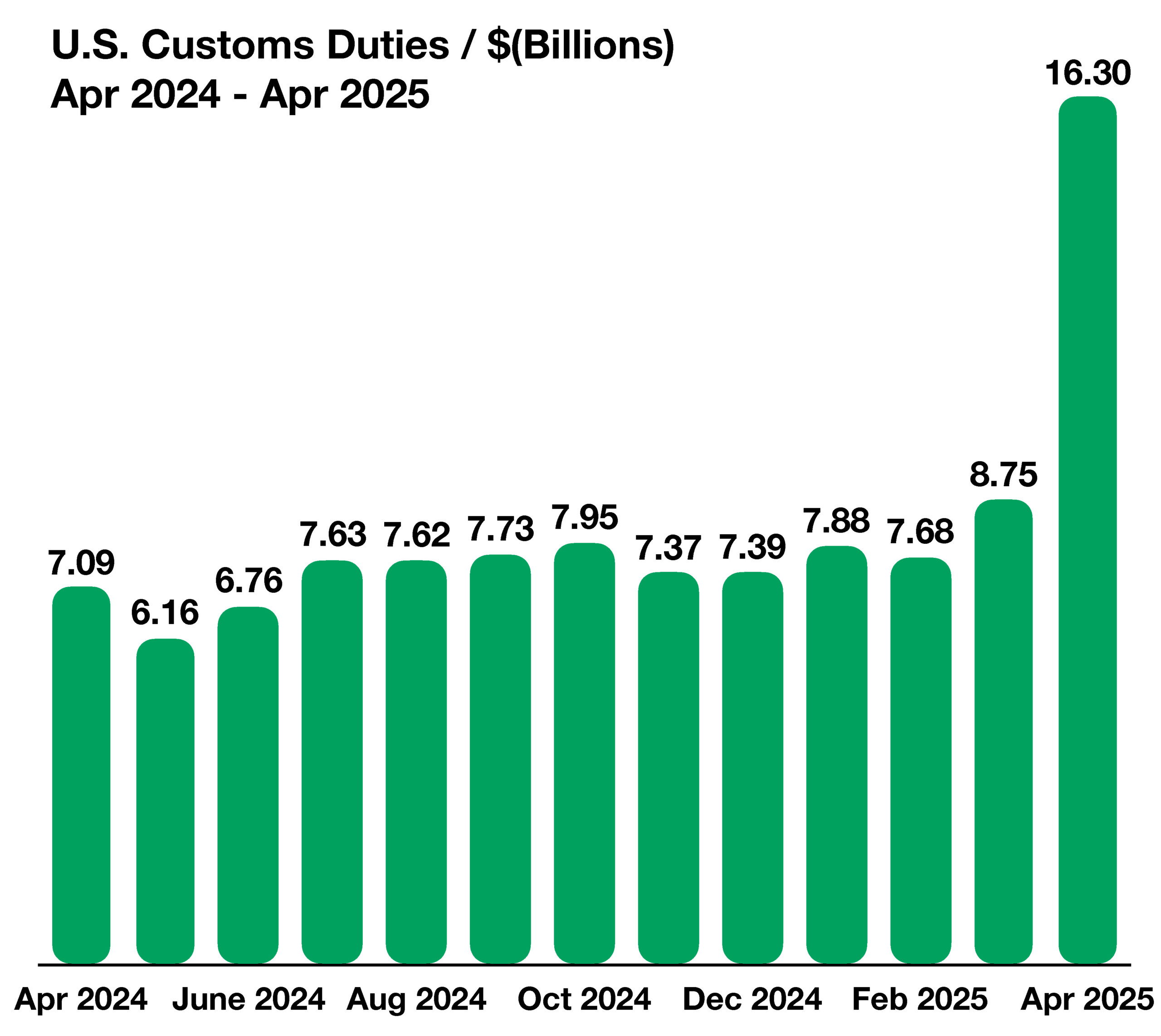

Revenue from newly-imposed tariffs in early April nearly doubled to $16.3 billion, up from $8.75 billion in March. Duties collected were imposed on a wide range of products including raw and finished products from a multitude of countries. Monthly tariff revenue has averaged roughly $7.5 billion for the past twelve months.

Sources: U.S. Depart. of Labor, Federal Reserve, Treasury Depart., U.S. Commerce Depart., Moody’s