Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Macro Overview

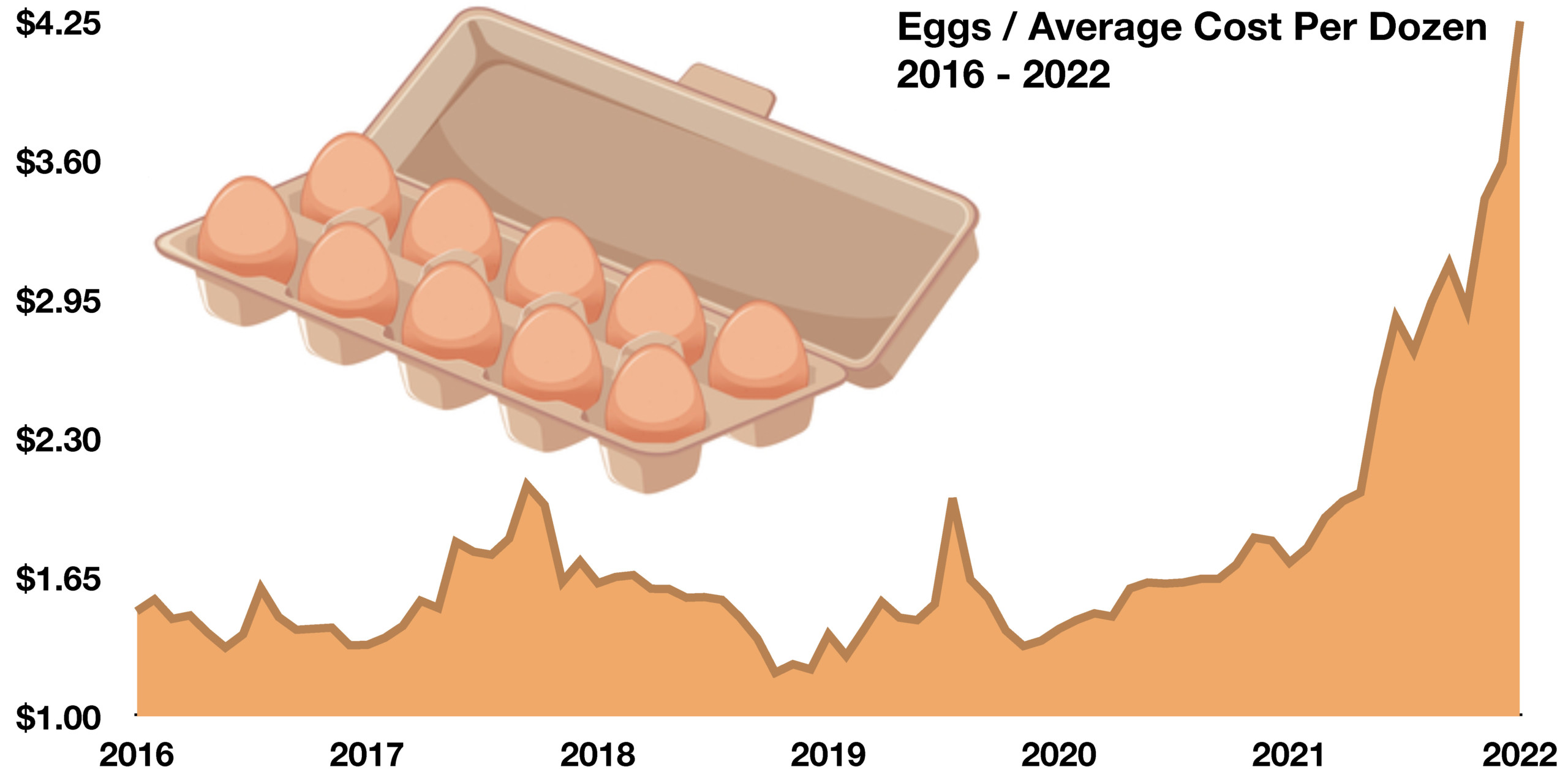

Inflation persisted in February as government data revealed stubbornly elevated prices for food and energy. As a result, the Federal Reserve’s stance on additional interest rate increases continues to pressure equity and bond markets. The Fed’s primary concern right now is to combat the spiraling effect of severe inflation, so it is expected to continue on its trajectory of rate increases until economic data proves otherwise.

Economic terms often mentioned in the media recently include soft landing and hard landing. A soft landing indicates a non-recessionary outcome with successfully reduced inflation after the Fed stops raising rates, while a hard landing denotes a recessionary environment due to the excessive slowing of economic activity. Economists note that it is too soon to determine which will occur in this case.

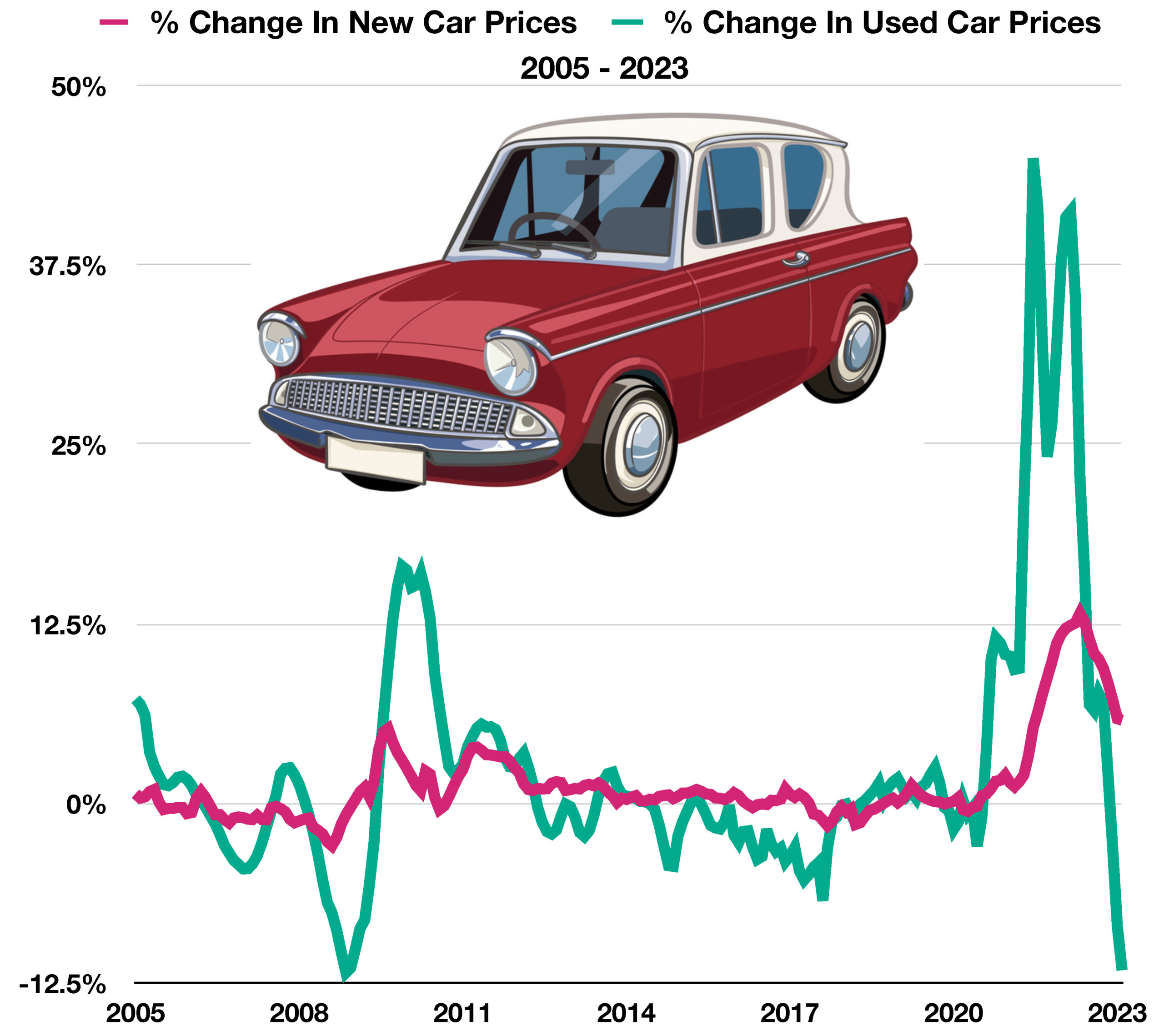

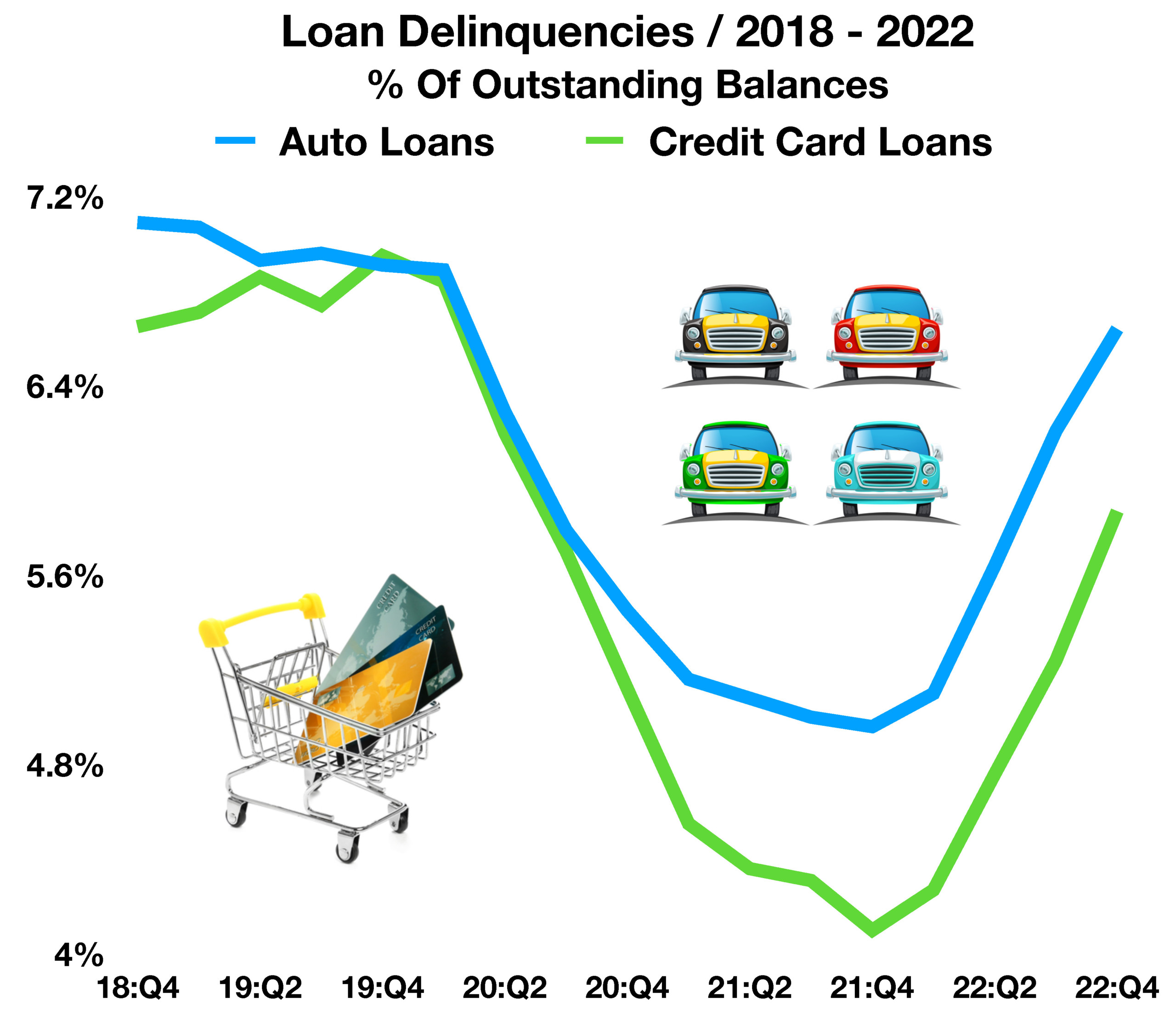

Stronger-than-expected employment data and surprisingly resilient consumer demand drove the Federal Reserve to again raise short-term rates over the past month. Mortgage and consumer loan rates rose in February, adversely affecting prices for housing and consumer durables, which are frequently financed with debt and therefore significantly impacted by interest rates.

Recently released data from the Bureau of Labor Statistics reveals that consumers pulled back on cyclical goods such as clothes and electronics, while focusing on food and essential products like toilet paper and toothpaste. Larger ticket items, which are more expensive products such as appliances and autos, saw a drop in sales as consumers redirected funds.

Internationally, the European Union inflation is at 10% alongside a 6.1% unemployment rate, translating into economic stagnation per the most recent data releases. Similar to the U.S., stubbornly high food and energy prices continue to divert consumers from buying discretionary items to buying necessities. The Russian invasion of Ukraine continues to pose a challenge to global supply chains and inflationary pressures. Reduced trade with Russia has led numerous countries to replace inexpensive Russian imports with other pricier sources.

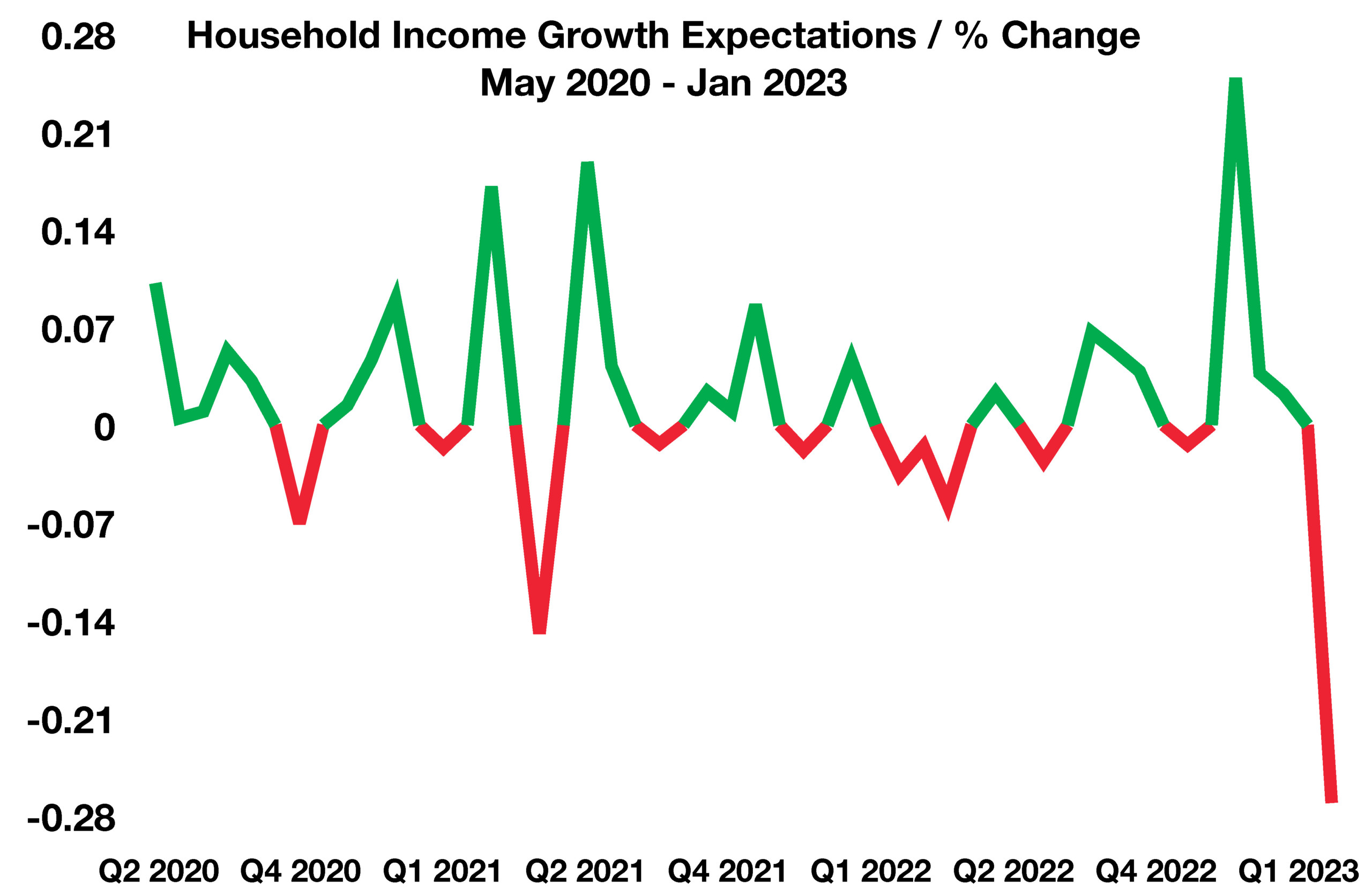

A Federal Reserve Bank of New York survey showed that households expect income growth to drop, creating pressure on consumer confidence, which is a major driver of economic activity. However, U.S. unemployment currently sits at a 53-year low of 3.4%, providing a counterpoint of strong consumer spending power. (Sources: Eurostat, U.S. Treasury, Federal Reserve, BLS, Labor Department)

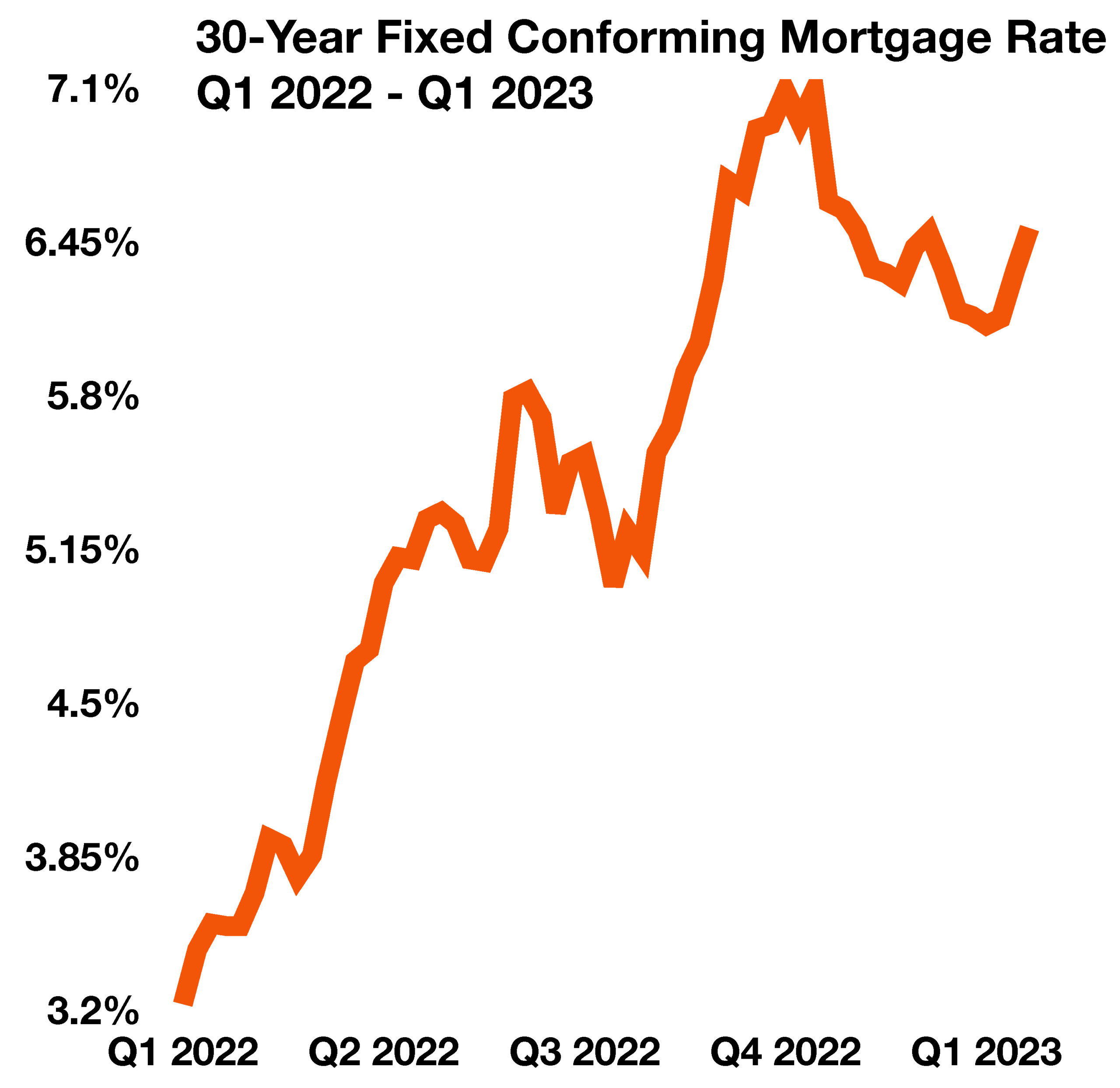

With interest rates breaching higher levels, mortgages are becoming less affordable for millions of Americans. As a result, demand for new mortgages is reaching decades-long lows, influencing many homebuyers to either wait for rates to fall or for home prices to drop significantly. The average 30-year fixed mortgage rate reached 6.65% in early March, its highest point since November of last year. Mortgage loan rates reached as high as 7.08% in October and November of 2022, a 20-year high that the housing market last saw in 2002. (Sources: Federal Reserve of St. Louis, Freddie Mac)

With interest rates breaching higher levels, mortgages are becoming less affordable for millions of Americans. As a result, demand for new mortgages is reaching decades-long lows, influencing many homebuyers to either wait for rates to fall or for home prices to drop significantly. The average 30-year fixed mortgage rate reached 6.65% in early March, its highest point since November of last year. Mortgage loan rates reached as high as 7.08% in October and November of 2022, a 20-year high that the housing market last saw in 2002. (Sources: Federal Reserve of St. Louis, Freddie Mac)