Stock Indices:

| Dow Jones | 38,996 |

| S&P 500 | 5,096 |

| Nasdaq | 16,091 |

Bond Sector Yields:

| 2 Yr Treasury | 4.64% |

| 10 Yr Treasury | 4.25% |

| 10 Yr Municipal | 2.53% |

| High Yield | 7.63% |

YTD Market Returns:

| Dow Jones | 3.47% |

| S&P 500 | 6.84% |

| Nasdaq | 7.20% |

| MSCI-EAFE | 2.23% |

| MSCI-Europe | 1.23% |

| MSCI-Pacific | 3.98% |

| MSCI-Emg Mkt | -0.27% |

| US Agg Bond | -1.68% |

| US Corp Bond | -1.67% |

| US Gov’t Bond | -1.59% |

Commodity Prices:

| Gold | 2,051 |

| Silver | 22.87 |

| Oil (WTI) | 78.25 |

Currencies:

| Dollar / Euro | 1.08 |

| Dollar / Pound | 1.26 |

| Yen / Dollar | 150.63 |

| Canadian /Dollar | 0.73 |

Macro Overview

The Federal Reserve decided to leave rates unchanged in February, igniting concerns among the financial markets that interest rates may not fall as soon as many had expected. Larger than anticipated inflation data and resilient employment is deterring the Fed from lowering rates too soon.

The Consumer Price Index (CPI) revealed that inflation was running at 3.1% for the past year as of January, down from 3.9% in December. Some analysts believe that it may be too soon for the Fed to determine as to when it will lower rates, even though inflation seems to be alleviating.

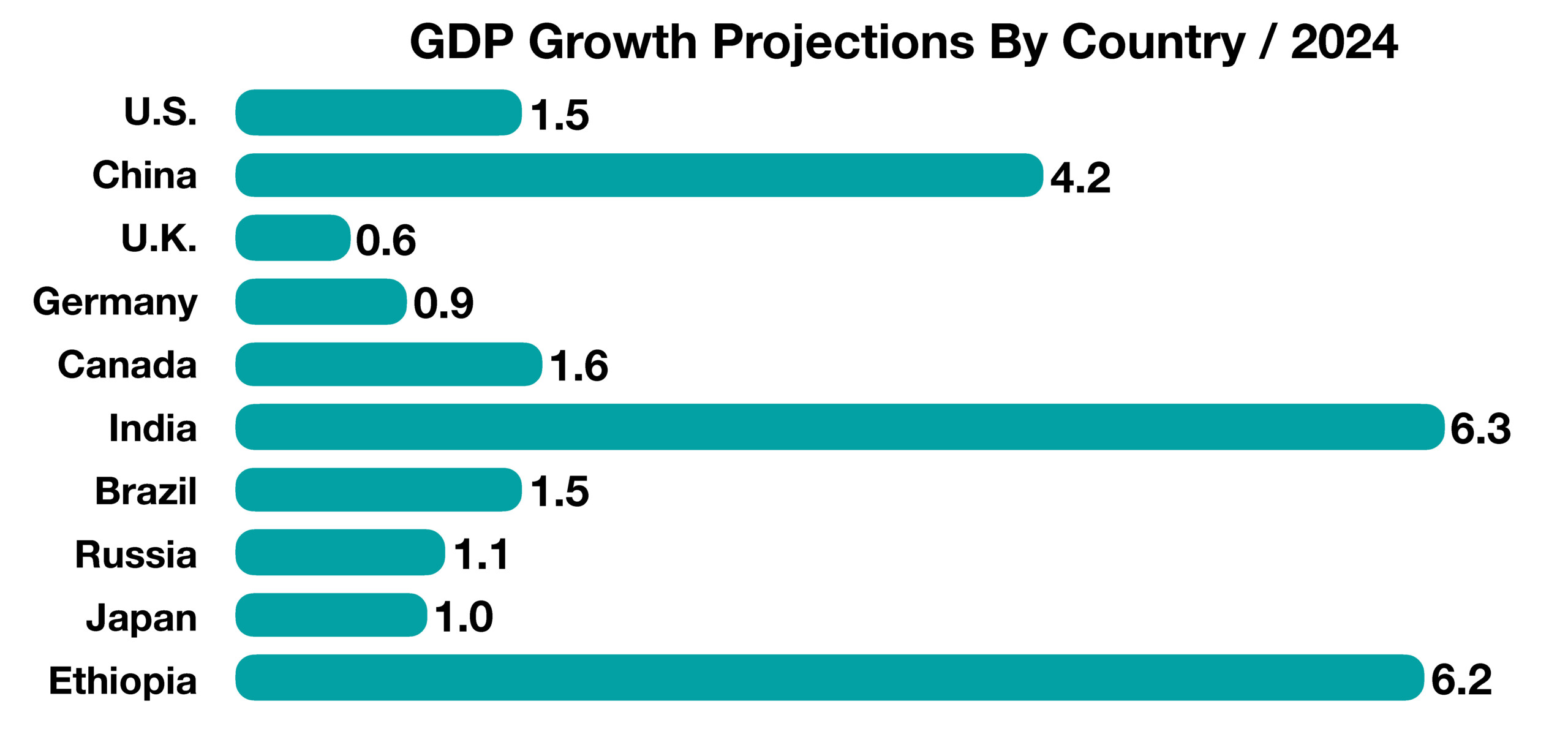

A global recessionary environment is evolving, with recent economic data showing that the U.K. and Japan have both fallen into a technical recession. Global growth forecasts by the International Monetary Fund (IMF) indicate a broad pullback in economic expansion among various countries worldwide.

Interest rates remained stubborn in February as Treasury bond yields rose slightly across all maturities, known as a shift up in the yield curve. Larger than expected inflation data as well as the Fed’s hesitancy to lower rates, drove bond yields higher in February.

Three Federal Reserve officials announced that the pace of rate cuts by the Fed will be contingent on yet to be released economic data. Fed officials differed as to when any rate cuts would materialize, two suggested “later this year” while one estimated this summer. The Fed’s most significant factors when determining any reduction in rates remain inflation, employment, and economic growth.

The growing interest and recent rise in Artificial Intelligence (AI) has reinforced a lingering belief that the domestic economy has begun to shift from an industrial economy to a digital economy. Economists believe that such a transformation, should it ever completely occur, might take decades to evolve.

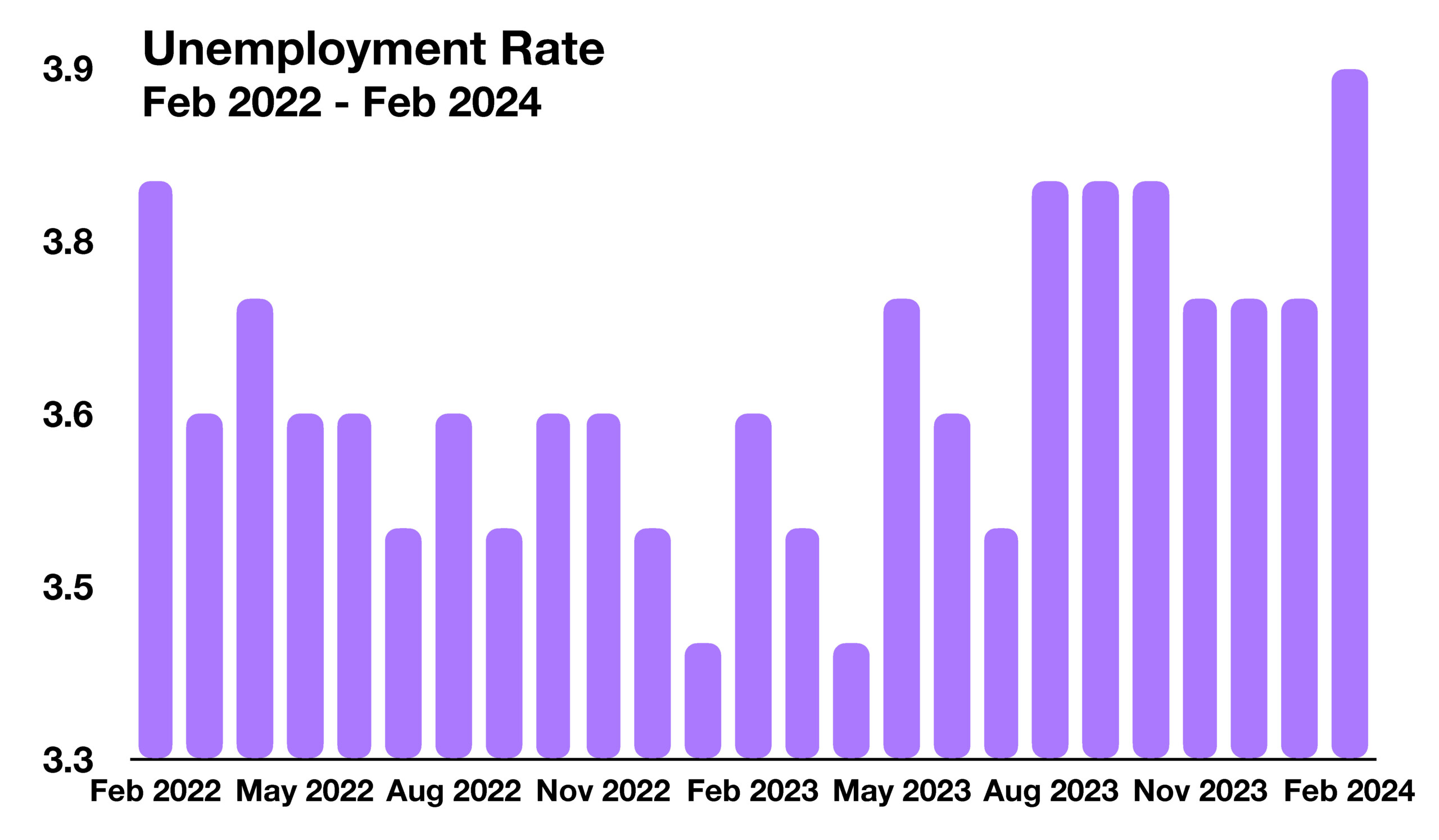

Unemployment rose to the highest level in two years, hitting 3.9% in February, as reported by the Department of Labor. Wage growth also slowed from the previous month, possibly signaling a cooling labor market as perceived by economists.

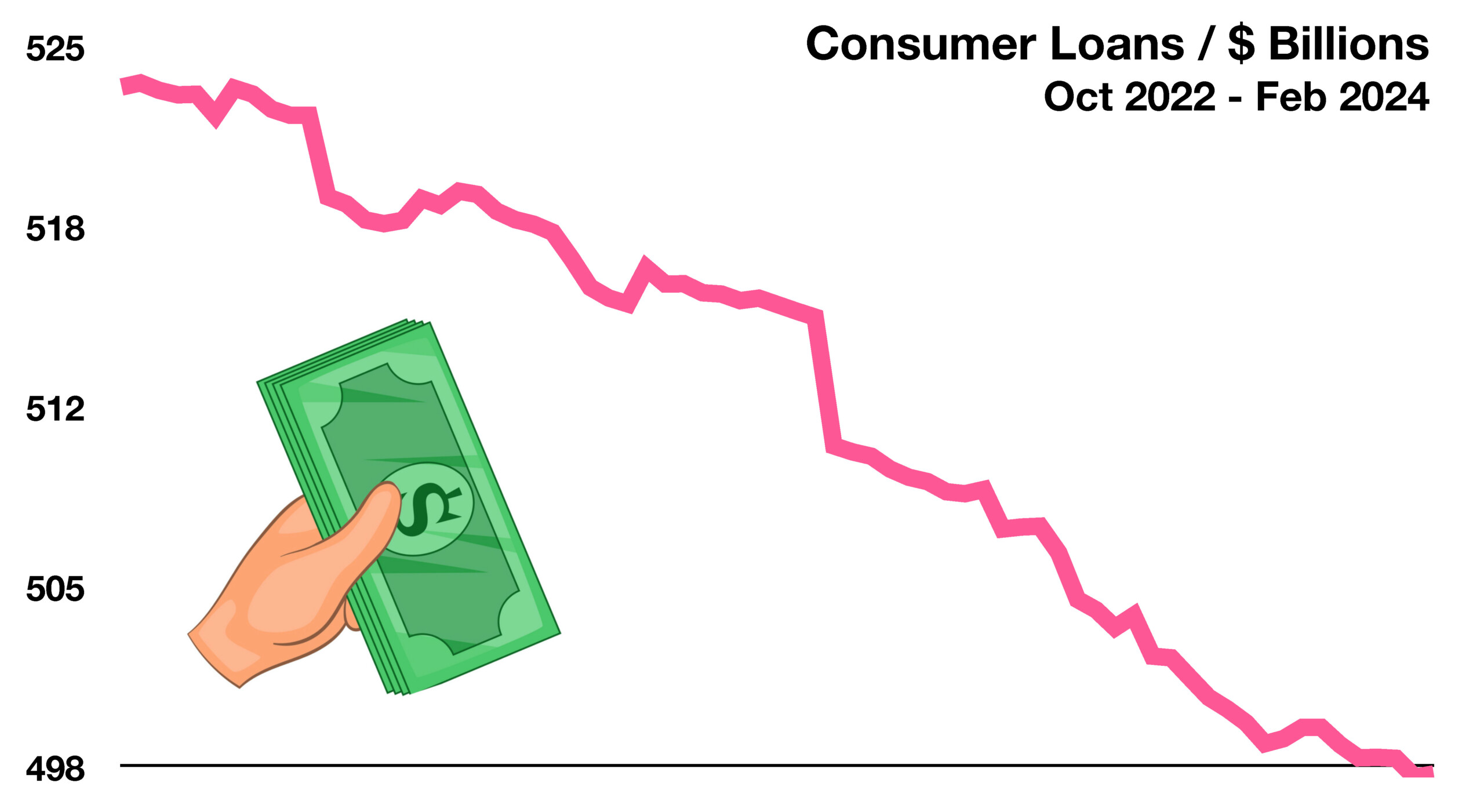

Requirements for large banks to hold more capital are being proposed by the Federal Reserve. A proposal to boost bank capital by 19% is seen as a preparation for a possible retraction in economic activity as well as defaults among bank holdings. Regulators including the FDIC and the Office of the Comptroller of the Currency support the heightened capital requirements. Banks argue that the additional capital requirements would increase lending costs and tighten loan availability for consumers and businesses.

According to data released by the Bureau of Labor Statics, the past year has seen an increase in the purchase of lottery tickets and an increase in gambling. Some analysts believe that the proliferation of online gambling and lotto purchases is facilitating an increase in speculative consumer behavior.

Sources: Federal Reserve, Labor Dept., BLS, IMF

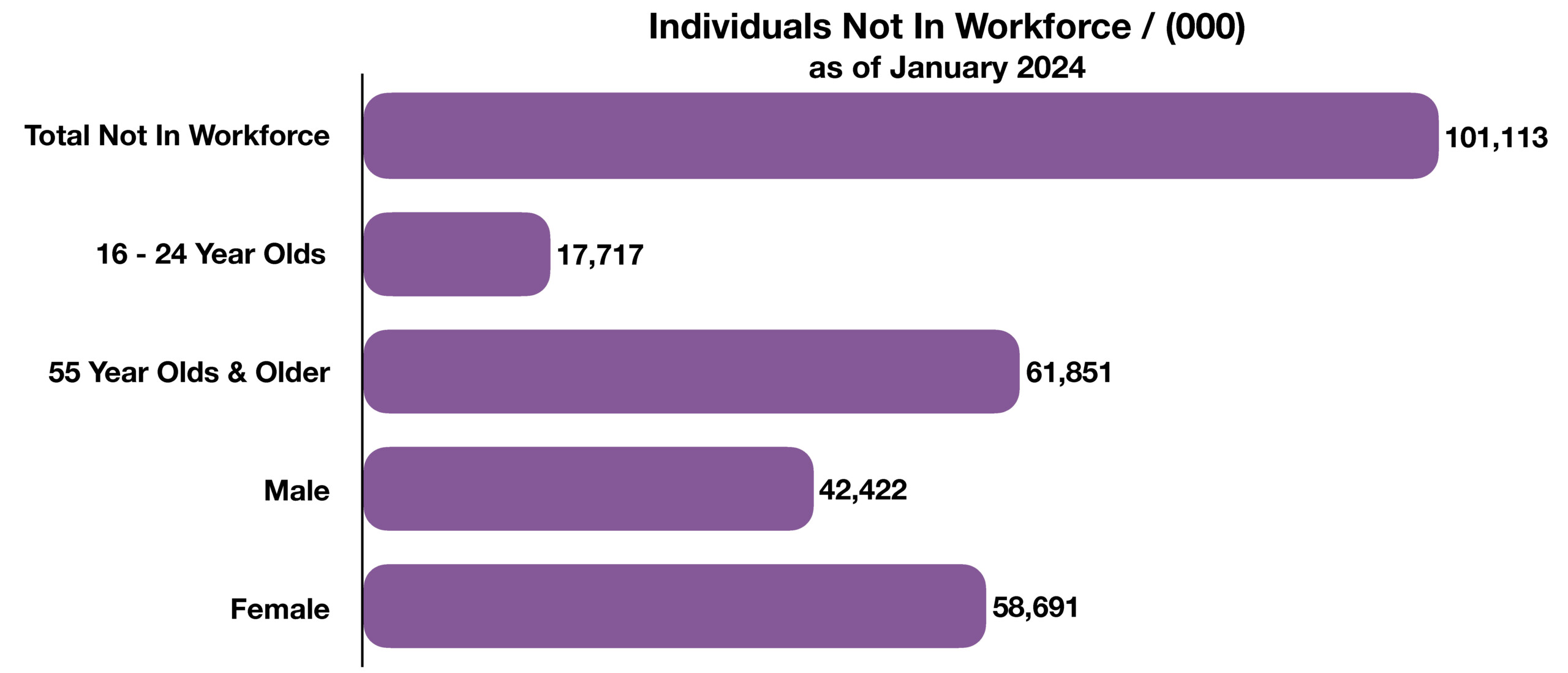

The Department also identified that native born Americans with a job fell by 881,000 over the past year to 129.3 million, while foreign born workers with a job rose by 1.5 million to 31 million over the same period. Sectors experiencing employment gains include some lower paying jobs in healthcare, government, and food services.(Source: Department of Labor)

The Department also identified that native born Americans with a job fell by 881,000 over the past year to 129.3 million, while foreign born workers with a job rose by 1.5 million to 31 million over the same period. Sectors experiencing employment gains include some lower paying jobs in healthcare, government, and food services.(Source: Department of Labor)