Stock Indices:

| Dow Jones | 49,652 |

| S&P 500 | 7,209 |

| Nasdaq | 24,892 |

Bond Sector Yields:

| 2 Yr Treasury | 3.88% |

| 10 Yr Treasury | 4.40% |

| 10 Yr Municipal | 2.96% |

| High Yield | 6.87% |

YTD Market Returns:

| Dow Jones | 3.31% |

| S&P 500 | 5.31% |

| Nasdaq | 7.10% |

| MSCI-EAFE | 5.04% |

| MSCI-Europe | 2.95% |

| MSCI-Far East | 9.09% |

| MSCI-Emg Mkt | 13.94% |

| US Agg Bond | 0.07% |

| US Corp Bond | -0.09% |

| US Gov’t Bond | -0.08% |

Commodity Prices:

| Gold | 4,641 |

| Silver | 74.65 |

| Oil (WTI) | 105.76 |

Currencies:

| Dollar / Euro | 1.16 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 159.95 |

| Canadian /Dollar | 0.73 |

Macro Overview

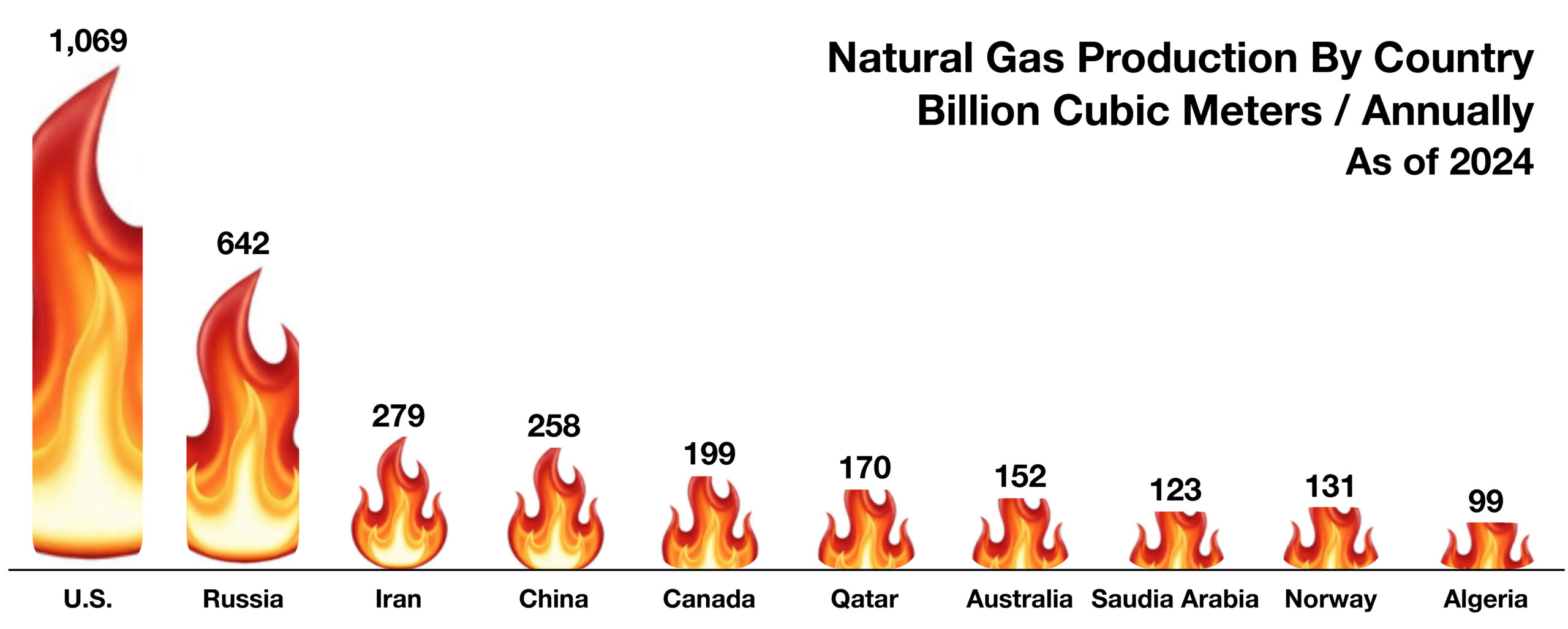

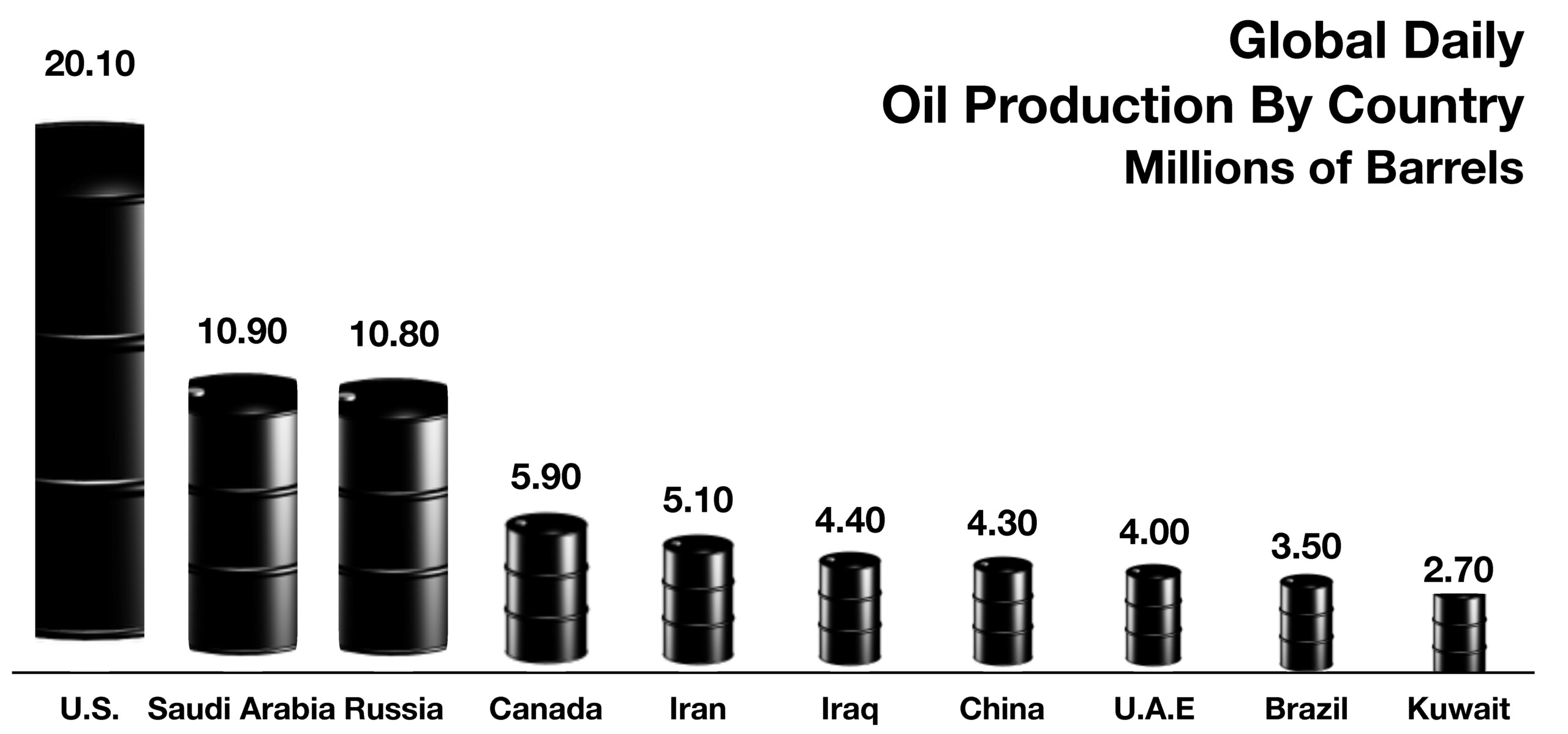

The most pronounced effects of the Middle East conflict on U.S. financial markets have been heightened inflation concerns, driven by elevated oil and gasoline prices, and rising Treasury yields. International markets have borne a greater impact from the conflict than U.S. markets. As the world’s largest producer of oil and natural gas, the United States has emerged as a leading global energy supplier, while many other nations have grown increasingly dependent on U.S. energy exports.

Oil lies at the center of concern surrounding the Iranian conflict, as more than 20% of global oil shipments pass through the Strait of Hormuz. Iran has threatened to target any vessel attempting to navigate the Strait, stoking fears that oil tankers could be seized or immobilized.

The attack on Iran has sent shock waves across the Middle East, affecting numerous countries amid rising risks to infrastructure and economic stability. Any escalation of the conflict could further disrupt energy markets and regional travel.

China’s involvement in the conflict has so far been limited but is expected to intensify, as more than 90% of Iran’s oil exports are sold to China, accounting for nearly 15% of China’s oil imports. China has continued to circumvent U.S. sanctions imposed in 2018 by purchasing Iranian oil, effectively in violation of those restrictions.

Prospects for Federal Reserve rate cuts have come into question as policymakers contend with renewed inflation pressures alongside weakening employment conditions. Rising inflation risks reduce the Fed’s flexibility to offset a softening labor market through lower interest rates.

Meanwhile, a federal trade-court judge ruled that the U.S. government must begin refunding more than $130 billion collected under last year’s global tariffs, which were invalidated by the Supreme Court in January. More than 1,800 U.S. companies are seeking reimbursement for tariffs paid to date.

Rising oil prices, combined with the court ruling requiring tariff refunds, have pressured Treasury bonds, pushing yields higher and prices lower. Elevated Treasury yields translate into higher borrowing costs for consumers, potentially constraining economic growth.

The Labor Department reported that the U.S. economy lost 92,000 jobs in February, defying expectations for modest job gains. The unemployment rate edged up to 4.4%, though it remains well below the pre-pandemic peak of 10% reached in October 2009. The latest data underscore ongoing weakness in a labor market that has shown limited hiring momentum in recent months.

Mounting inflation concerns alongside a weakening labor market have revived fears of stagflation, marked by rising prices and slowing economic growth. Tepid job creation and higher unemployment risk dampening consumer spending, a critical driver of economic expansion. (Sources: Dept. of Labor, Fed, U.S. Treasury, Dept. of Commerce, International Energy Agency)