Michael McCormick

5 West Mendenhall, Ste 202 | Bozeman, MT 59715

406.920.1682 mike@mccormickfinancialadvisors.com

Sustainable Income Planning | Investments | Retirement

Stock Indices:

| Dow Jones | 44,094 |

| S&P 500 | 6,204 |

| Nasdaq | 20,369 |

Bond Sector Yields:

| 2 Yr Treasury | 3.72% |

| 10 Yr Treasury | 4.24% |

| 10 Yr Municipal | 3.21% |

| High Yield | 6.80% |

YTD Market Returns:

| Dow Jones | 3.64% |

| S&P 500 | 5.50% |

| Nasdaq | 5.48% |

| MSCI-EAFE | 17.37% |

| MSCI-Europe | 20.67% |

| MSCI-Pacific | 11.15% |

| MSCI-Emg Mkt | 13.70% |

| US Agg Bond | 4.02% |

| US Corp Bond | 4.17% |

| US Gov’t Bond | 3.95% |

Commodity Prices:

| Gold | 3,319 |

| Silver | 36.32 |

| Oil (WTI) | 64.98 |

Currencies:

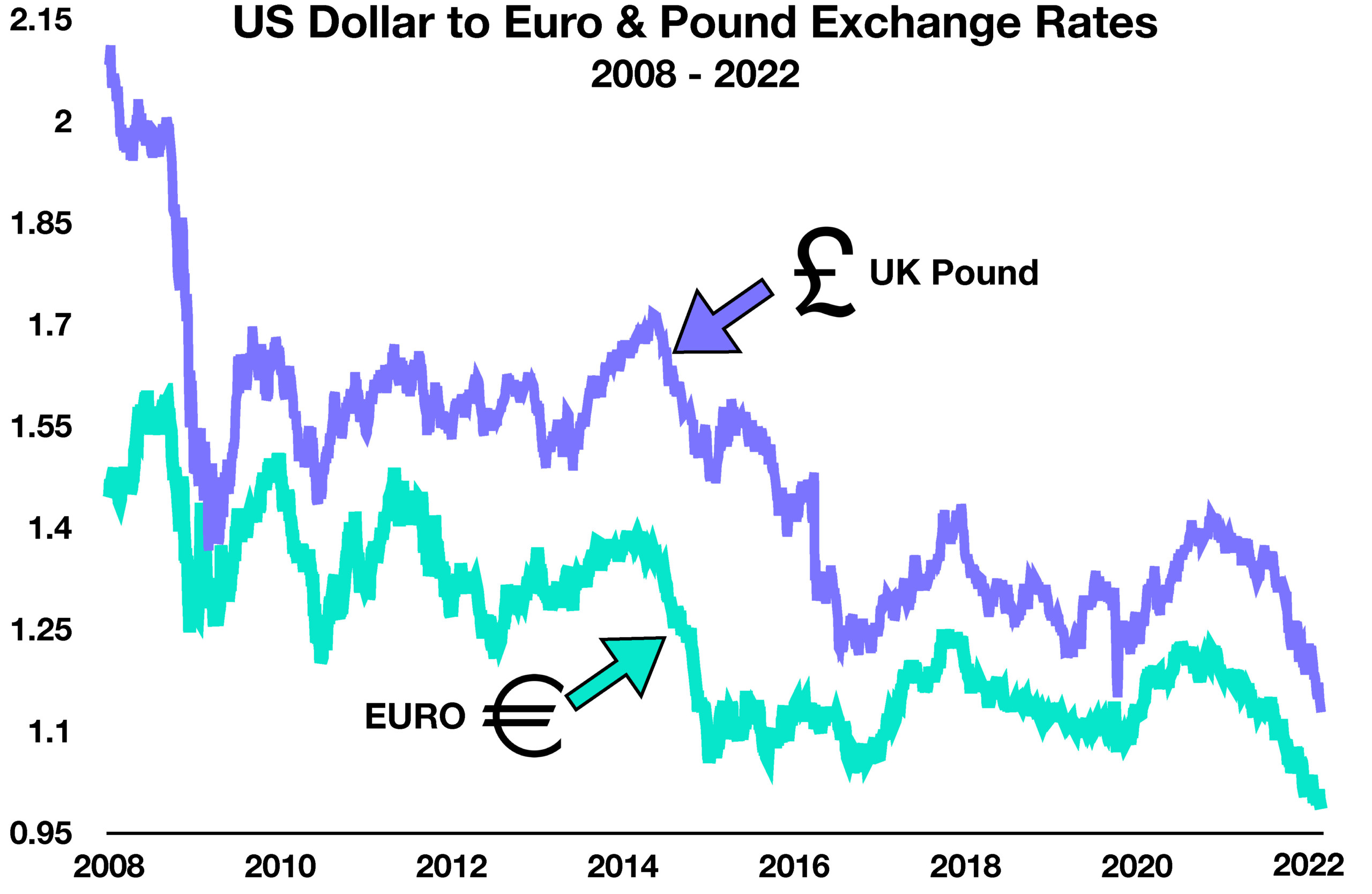

| Dollar / Euro | 1.17 |

| Dollar / Pound | 1.37 |

| Yen / Dollar | 144.61 |

| Canadian /Dollar | 0.73 |

Dear Friends, this may not be the bottom, but this is what it feels like.

It has been a dismal year for market investors. Year to date both stocks AND bonds are down about 24% (as of this writing)! The only safety that feels good is cash and that just lost 9% to inflation. The losses are painful and confusing. Additionally, we are fearful of more pain with every election, natural disaster, oversees conflict, and monthly statement. Warren Buffet says to be greedy during these times. But before that can happen, we first need to stop being fearful of tomorrows uncertainty.

Oh Montana!

I’m always reminding myself that economics and finance are social sciences and not exact sciences. Markets are more like wild rivers than equations and the only rule is that there are no smooth rides or straight lines. As soon as someone has figured out which way we are going, the rules change. But eventually perseverance is rewarded, markets will return to fair value, and it will happen probably in unexpected ways. American Capitalism will reward risk, we just don’t know when.

Fear demands action, prudent investing requires discipline.

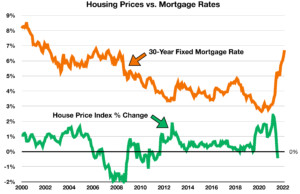

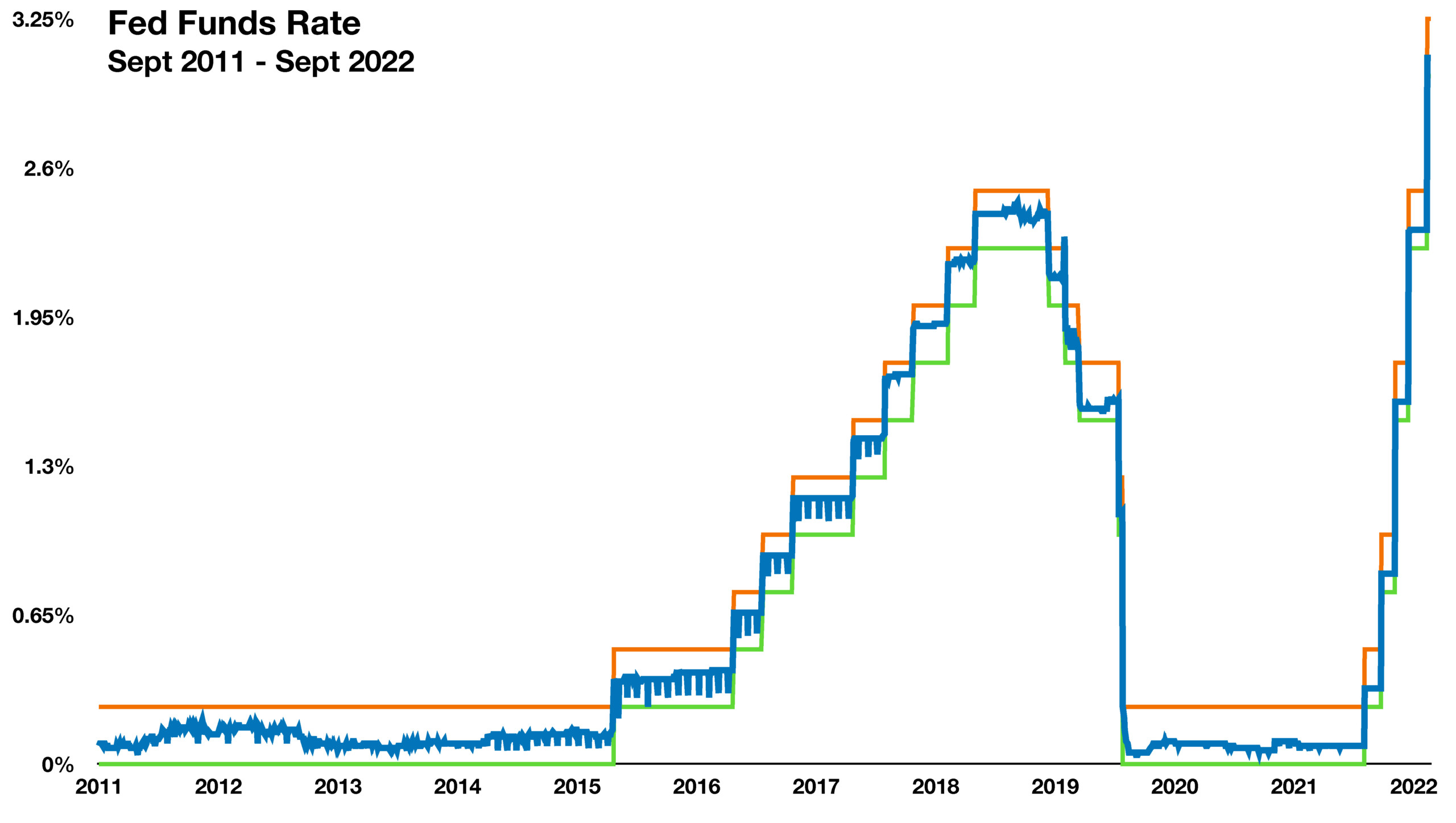

The one rate to rule them all – The Fed Funds Rate, which is controlled by the Federal Reserve Board, is the interest rate at which banks charge each other to borrow money. This year, the Fed has continued to aggressively increase the rate.

The effects of increasing the Fed Funds Rate are more expensive borrowing costs and reduced demand for borrowing money. By increasing the rate, the Fed hopes to pacify rising inflation, as the U.S. is currently experiencing the highest inflation rate observed since 1981.

In March of this year, the Fed began its increase of interest rates. Before then, the rate was effectively at close to 0% between April 2020 and February 2022. As of September 21st, the rate has a target range of 3% to 3.25%, which means the rate has risen 3% in just 7 months. This is the largest increase made by the Fed in a single year since 1982. Based on this, the Fed Funds Rate would reach 4% to 4.25% by the end of the year. (Sources: Federal Reserve Bank of St. Louis, Federal Reserve Bank of New York)