Derek J. Sinani

Founder/Managing Partner

derek@ironwoodwealth.com

7047 E. Greenway Parkway, Ste. 250

Scottsdale, AZ 85254

480.473.3455

Stock Indices:

| Dow Jones | 40,669 |

| S&P 500 | 5,569 |

| Nasdaq | 17,446 |

Bond Sector Yields:

| 2 Yr Treasury | 3.60% |

| 10 Yr Treasury | 4.17% |

| 10 Yr Municipal | 3.36% |

| High Yield | 7.69% |

YTD Market Returns:

| Dow Jones | -4.41% |

| S&P 500 | -5.31% |

| Nasdaq | -9.65% |

| MSCI-EAFE | 12.00% |

| MSCI-Europe | 15.70% |

| MSCI-Pacific | 5.80% |

| MSCI-Emg Mkt | 4.40% |

| US Agg Bond | 3.18% |

| US Corp Bond | 2.27% |

| US Gov’t Bond | 3.13% |

Commodity Prices:

| Gold | 3,298 |

| Silver | 32.78 |

| Oil (WTI) | 58.22 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 142.35 |

| Canadian /Dollar | 0.72 |

Macro Overview

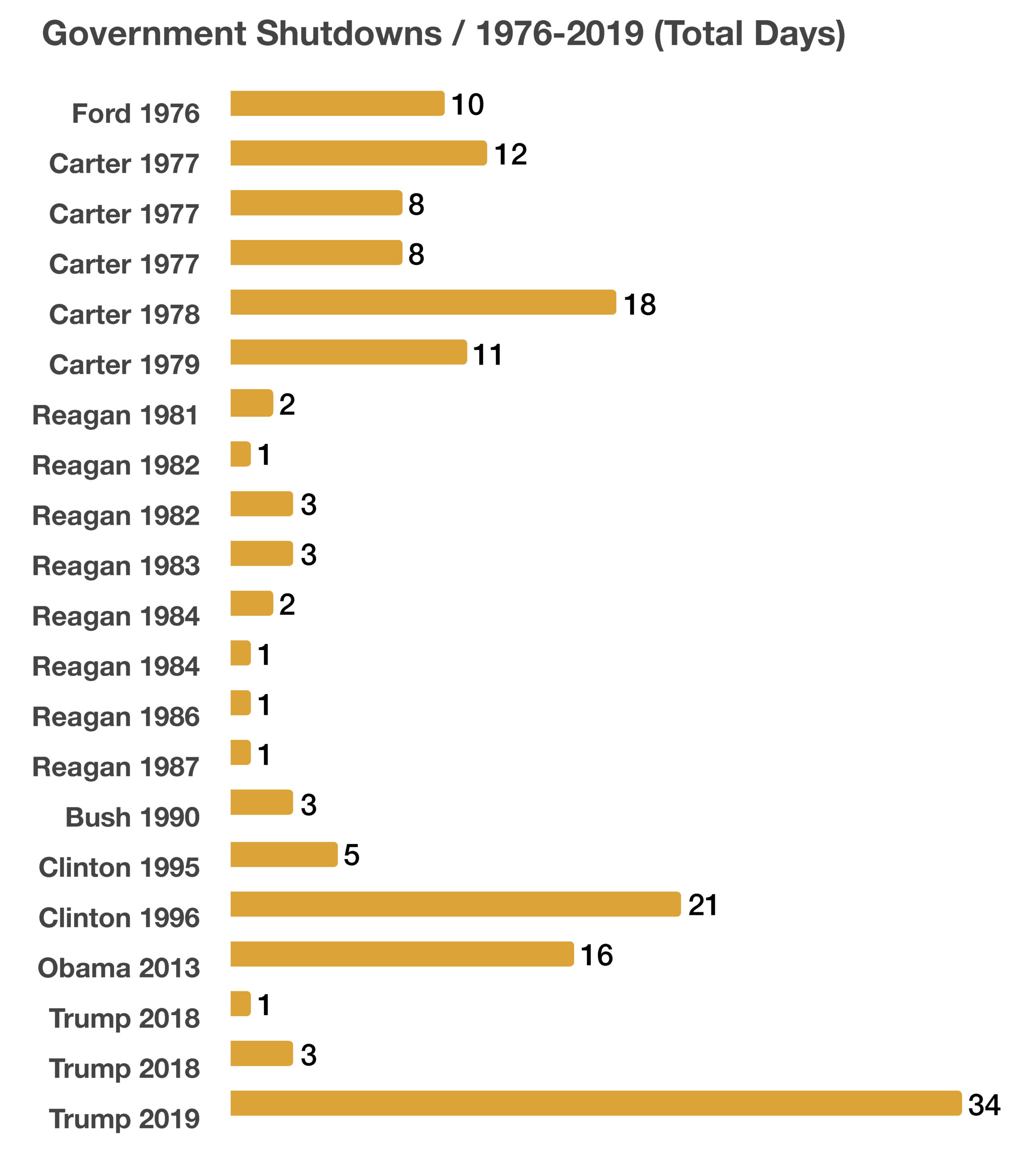

A federal government shutdown was averted on September 30th, when Congress voted to fund government operations until mid-November. Volatility in the financial markets increased during September, as uncertainty surrounding a resolution persisted. The possibility of a shutdown will evolve again in November, as Congress once again deliberates on the passage of the federal budget. Should a shutdown occur, the impact on the economy would initially be mild as previous shutdowns, and possibly expanding as millions of government workers go without salary. Private sector contractors would also be impacted with delayed payments, while consumer uncertainty hinders spending.

The federal government shutdown dilemma has increased the possibility of a credit downgrade by Moody’s, the last agency with a AAA rating on government debt. Credit agencies S&P and Fitch have already lowered their ratings on U.S. government debt to AA+, down from the top tier rating of AAA. Another downgrade is expected to make it more costly for the government to borrow funds and maintain already excessive debt levels. The last downgrade was on August 1st when Fitch lowered its rating to AA+ from AAA.

A shutdown of the federal government is expected to affect only government operations and payments that are not funded by permanent appropriations. Those funded by permanent appropriations such as the Postal Service, entitlement programs such as Social Security and Medicare, will not be affected. Other essential and critical departments and agencies of the government would also continue operations, such as the Defense Department and the Treasury Department. Scheduled debt payments such as on Treasury bills, notes and bonds would also continue to be made.

Rising oil prices are hindering portions of the economy, inflicting rising costs on transportation, manufacturing, and food distribution. Equity analysts believe that some companies may see compressed earnings as lofty fuel costs continue to wear on operating expenses and potentially stoking the inflation embers. With that said, I’m expecting broadly positive Q3 and Q4 corporate earnings and continued disinflationary trends.

** Reminder, Medicare open enrollment is from October 15th to December 7th, allowing changes for existing Medicare recipients and enrollments for new members. Any changes and new enrollments are effective January 1, 2024.

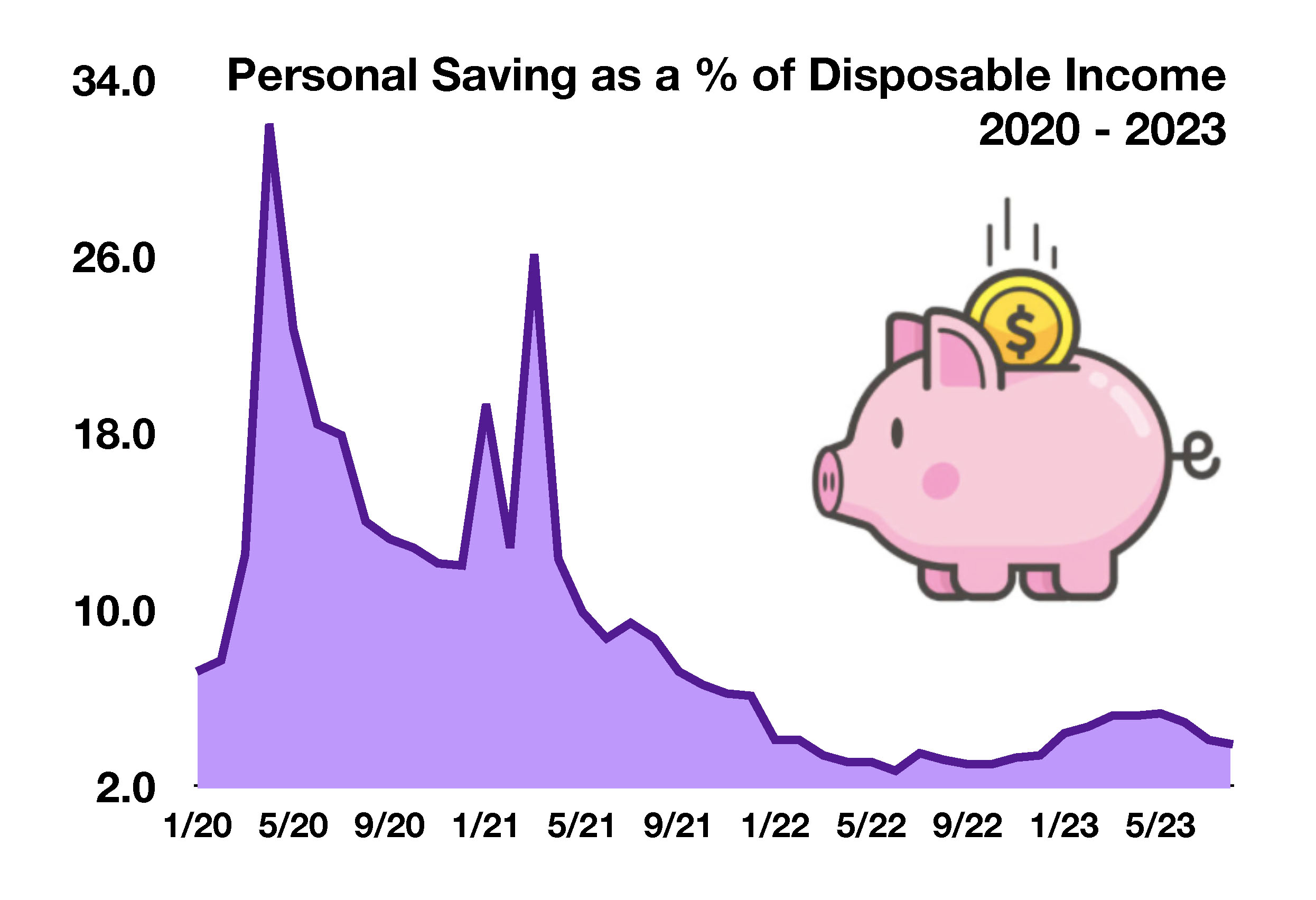

As retail stores and restaurants began to reopen in 2021, consumers were ready to spend funds that had been sitting idle for nearly a year. Consumer consumption fell dramatically in April 2020, as stay-at-home mandates and retail closures were in effect, only to elevate to new highs in April 2021 as consumers were able to spend freely again – oh and how they spent. The most recent data trends validate that consumers are spending less and perhaps with greater caution as a degree of economic uncertainty takes hold; or perhaps they are simply a little hungover from their post-pandemic spending binger. At the moment, I’m leaning towards the later and continue to forecast disinflation and a soft economic landing.

As retail stores and restaurants began to reopen in 2021, consumers were ready to spend funds that had been sitting idle for nearly a year. Consumer consumption fell dramatically in April 2020, as stay-at-home mandates and retail closures were in effect, only to elevate to new highs in April 2021 as consumers were able to spend freely again – oh and how they spent. The most recent data trends validate that consumers are spending less and perhaps with greater caution as a degree of economic uncertainty takes hold; or perhaps they are simply a little hungover from their post-pandemic spending binger. At the moment, I’m leaning towards the later and continue to forecast disinflation and a soft economic landing.

As the highways expanded to accommodate more traffic and heavier loads, roads and bridges have become integral components to the nation’s transportation system. Of the 117,483 bridges covering the nation’s highways, The Department of Transportation has identified over 5,230 as structurally deficient. The District of Columbia alone has over 16% of its highway bridges deemed structurally deficient. These statistics are completely unacceptable.

As the highways expanded to accommodate more traffic and heavier loads, roads and bridges have become integral components to the nation’s transportation system. Of the 117,483 bridges covering the nation’s highways, The Department of Transportation has identified over 5,230 as structurally deficient. The District of Columbia alone has over 16% of its highway bridges deemed structurally deficient. These statistics are completely unacceptable.