Macro Overview

The Fed raised rates for the third time this year, signaling it was on track for further hikes

over the next few months. Rates moved higher across the fixed income spectrum, with the

10-year Treasury bond piercing the 3% mark, a level last reached in May of this year. The

Federal Reserve also revised its estimates for GDP growth from 2.8% to 3.1% for 2018, with

an eventual slowing to1.8% by 2021.

Newly imposed tariffs by the Department of Commerce on Chinese imports became

effective in late September. The $200 billion worth of tariffs will begin at a 10% rate and

increase to 25% by year end should the two countries not come to an agreement.

The Department of Commerce is incentivizing U.S. companies to shift production of goods in

China to the U.S. by allowing companies to redirect production prior to year end before

tariffs are scheduled to reach 25% on Chinese made products.

Equity markets brushed aside ongoing concerns over escalating international trade tensions

and instead focused on economic expansion in the United States. Analysts are seeing the

benefits of the recent tax cuts and deregulation translate into expanding earnings for U.S.

companies. Economists are also citing the tax cuts as a monumental factor in economic

expansion.

Preliminary damage estimates following the destruction caused by hurricane Florence are

expected to reach between $38 billion and $50 billion.The cost of Florence is not expected to

be anywhere near the cost of hurricanes Harvey, Maria, or Irma, yet will impose additional

strain on an all ready straddled insurance industry. Damage estimates are compiled by

Moody’s which tracks the claims paying ability of insurance companies, especially during

periods of significant payment of claims. The Federal Emergency Management Agency

(FEMA) has thus far received over 8,000 claims for flood damage which allows for a $5,000

payment without an adjuster visit.

Oil prices headed higher in September topping levels not reached since 2014. Global energy

markets reacted to limited production from OPEC, Saudi Arabia, Russia and the United

States. The price for a barrel of Brent oil, which is priced internationally, reached $80 while

the price of domestic oil priced as WTI surpassed $72. Adding to the supply strain were

recently imposed sanctions on Iranian oil exports along with production constraints in the

U.S.

Consumer sentiment reached its second highest level since 2004, as tracked by the

University of Michigan’s Consumer Sentiment Index. Sentiment among consumers improved

across all income categories with the expectation of higher wages and continued job growth.

Modest levels of inflation also propelled confidence among consumers.

The White House Council of Economic Advisers reported that 623 companies this past month

announced bonuses, pay increases, and better benefits as a result of the recent tax cuts. The

council also estimates that over 6 million American workers have so far directly benefited

from the tax law changes.

(Sources: Fed, Dept. of Commerce, Moody’s, EIA, White House Council of Economic Advisers)

THE OECD ESTIMATES U.S. ECONOMIC GROWTH AT 2.9% FOR 2018, UP FROM 2.2% IN 2017

Economic Data Influences Stocks – U.S. Equity Update

Major equity indices all posted gains for the third quarter, with the S&P 500 advancing 7.2%, the Dow Jones

Index gaining 9%, and the Nasdaq rising 7.1%. It was the single best quarter for stocks since 2013, buoyed

by recent corporate tax cuts, improving earnings, and stable economic growth.

A notable shift occurred in the third quarter as equities surpassed real estate as the largest portion of

household wealth. Real estate has out-valued equities as a percentage of household wealth for nearly 20

years.

Investments by companies in the S&P 500 Index increased to $341 billion in the first half of 2018, exceeding

the same period last year by 19 percent. The increase in investments is on pace to be the most significant

in nearly 25 years.

Several analysts are forecasting that the positive effects of the recent tax cuts will begin to fade as higher

interest rates begin to inflate capital borrowing costs.

Growth estimates from the Organization for Economic Cooperation and Development (OECD) place U.S.

economic growth at 2.9% for 2018, up from 2.2% in 2017, making it the fastest pace of growth since 2005.

(Sources: S&P, Bloomberg, OECD, Dow Jones, NASDAQ)

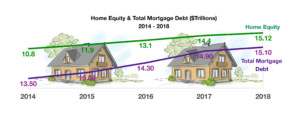

Household Equity Rising as Mortgage Debt Falling – Housing Market Overview

Following the debacle of the housing crisis from ten years ago, homeowners have become less ambitious

and more conservative. Equity levels in homes across the country have respectfully increased past

mortgage debt levels over the past few months. The latest data from the Fed shows that household equity

is approaching $16 trillion, exceeding the level of mortgage debt standing at $15.1 trillion.

Contributing to the rise in home equity includes rising real estate values, a sustained low rate environment,

limited housing supply, and an improving economic environment.

The amount of mortgage debt held by homeowners has not yet returned to the levels seen since before

the housing crisis. Homeowners have become more conservative and less ambitious as they were during

the crisis. Americans are also staying in their homes longer which helps build equity faster as opposed to

moving and taking out a new loan laden with fees and interest payments. The Fed report notes that

homeowners are taking much less equity out of their homes relative to the crisis period. The Fed data has

also identified that more cash buys are prevailing throughout the market, helping to somewhat reduce the

reliance on mortgage loans. (Sources: FRED; Federal Reserve Bank of St. Louis)

90% OF IBUPROFEN CONSUMED IN THE U.S. IS IMPORTED FROM CHINA

Products Exempted From New Tariffs…..For Now – Trade Policy

Of the 5,745 products that have been tagged with tariffs as they arrive in the U.S. from China, a handful have been omitted from tariffs. Among the exempted products are ibuprofen, barite, fluorine salts, and smartwatches. As newly imposed tariffs became effective in late September, numerous industries and companies have realized how vulnerable the U.S. is to various products and materials exclusively supplied by China. Fluorine salt, an essential chemical used to manufacture electrolytes for electric car batteries, is exempt from tariffs for the time being. Certain auto manufacturers and battery manufacturers located in the U.S. lobbied heavily to keep the chemical off the tariff list. The mineral barite is used widely in the U.S. energy industry for the purpose of facilitating the use of drilling fluids in oil and gas exploration. Department of Commerce data reveals that 90% of ibuprofen consumed in the U.S. is imported from China. Even though actual pills and tablets are produced in the United States, the key ingredient is imported directly from China. Various medical groups lobbied to have ibuprofen exempt from tariffs since it is widely used as a safe and easily available medication. Because of its broad medical application, the World Health Organization has placed ibuprofen on its list of Essential Medicines. A range of businesses from enormous energy companies to smaller suppliers of specialty parts have lobbied for tariff exemptions ever since the tariff wars began. Many have agreed that China has become an indispensable supplier of many raw and essential products used in the U.S. China has become a global producer of relatively obscure industrial commodities used in a host of numerous products, which the U.S. has become increasingly reliant on.

Recently imposed tariffs currently affect about $250 billion of Chinese imports, with an additional $267 billion proposed by year end. China has thus far retaliated with $110 billion in tariffs on U.S. products, yet exempted certain products such as oil. The ratio of trade between the U.S. and China stands at 4-to-1, meaning that for every 4 Chinese products the U.S. buys, China buys 1. (Sources: Commerce Department, World Health Organization)

Rates On The Rise – Fixed Income Update

The Fed announced its third rate hike for the year, indicating another rate increase anticipated in

December and three more to follow in 2019. The Fed’s key policy rate, the Federal Funds Rate, now stands at a range of 2% – 2.25%, the highest in ten years. Borrowing rates are gradually increasing in various consumer sectors including autos, appliances, and home mortgages. Many analysts believe that the current Fed Chairman, Jerome Powell, may have the ability to orchestrate a soft landing, meaning raising interest rates gradually without triggering a recession or economic slowdown. Of the various fixed income sectors, U.S. corporate high-yield bonds had the least amount of price declines in September, outperforming both government and investment grade debt. Some analysts view this as a validation of improving financial conditions for U.S. companies and their ability to repay debt. (Sources: Treasury Dept., Federal Reserve, Bloomberg)

623 U.S. COMPANIES ANNOUNCED BONUSES, PAY INCREASES, AND BETTER BENEFITS

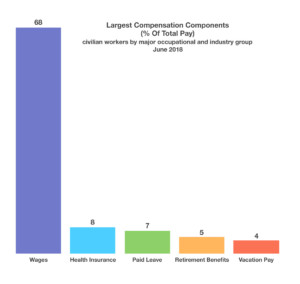

Larger Increase in Benefits Than Income – Labor Market Review

As companies struggle to keep existing qualified workers as well as attract and hire new workers, the task

of keeping labor costs minimized becomes an increasing challenge. Rather than paying higher wages, some

employers are compensating their employees with enriched benefits.

The Department of Labor monitors not only

how much companies pay their employees, but

the breakdown of how companies are

compensating their employees. The most

recent data released shows that companies are

spending more on health insurance, retirement

savings, bonuses, vacation time, and other

group benefits rather than increasing wages.

The recent gain in benefits grew by nearly 12%

for bonuses and benefits.

With unemployment near 18-year lows, the

3.9% unemployment rate has led to numerous

job openings that exceed the number of jobless

seeking work. This tightening has led to

employers using bonuses and benefits to

maintain and recruit skilled employees.

This past month, the White House Council of Economic Advisers reported that 623 U.S. companies

announced bonuses, pay increases, and better benefits as a result of the tax law changes. (Source: Labor

Department; September 18, 2018 Release,USDL-18-1499, White House Council of Economic Advisers)

When Taxes Replaced Tariffs – Historical Note

As a young country, the first of tariffs enacted to protect American business interests was the Tariff Act of

1789. The act was written to raise funds for the newly established government, reduce debt from the

Revolutionary War, and protect U.S. companies from unfair foreign competition. At the time, Congress

passed tariff amounts from 5% to as high 50%. For the next 150 years, tariffs generated the vast majority of

revenue for the federal government, until Congress ratified the 16th amendment in 1913 allowing the

imposition of federal income taxes. Tariffs began to lose their importance thereafter once federal tax

revenue began coming in.

Presidents varied on their views regarding tariffs over the decades, yet Abraham Lincoln said in 1847 that

“Give us a protective tariff and we will have the greatest nation on earth”. Tariffs eventually paid for some

of the costs of the Civil War for the north.

By the end of the second World War, the U.S. economy had become enormous with American companies

dominating the international markets. For the next 60 years, U.S. policy sought to reduce trade barriers

and tariffs in order to expand and maintain commerce throughout the world. (Sources: Library of Congress;

https://archive.org)

THE DEFICIT OF THE FIRST 10 MONTHS OF THE FISCAL YEAR 2018 REACHED 682 BILLION DOLLARS

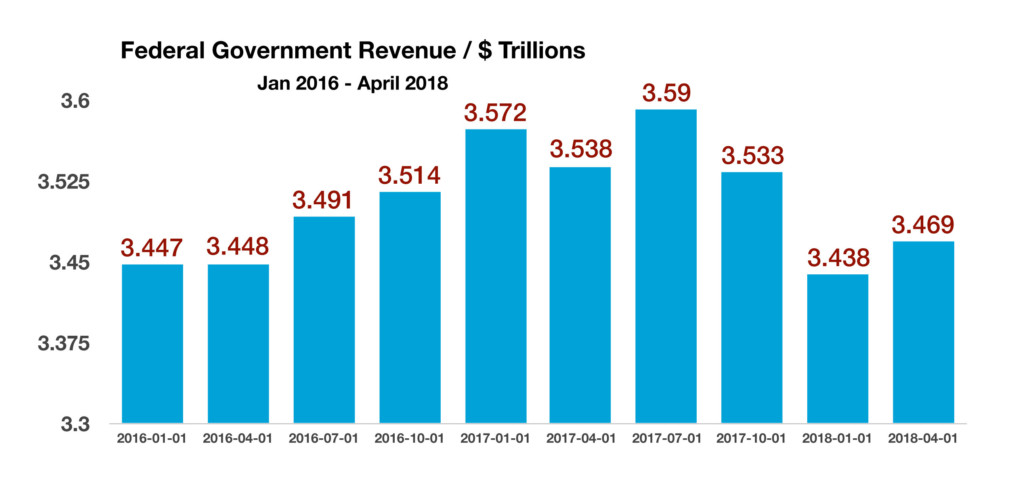

Federal Government Revenue Heading Higher – Fiscal Policy Overview

The Congressional Budget Office (CBO) released its summary of the most recent

federal budget as of July. The deficit of the first 10 months of the fiscal year 2018

reached 682 billion dollars, up $116 billion from a year earlier. Federal spending

increased by $143 billion, attributable to increases in Medicare, Medicaid, and Social

Security expenditures.

What was noted as well in the report was that revenues were also higher, increasing

by $26 billion. Even though corporate income taxes were lower following the recent

tax cuts, individual income taxes rose by $104 billion. The rise in individual taxes

was a result of larger withholdings on paychecks, which increased by $32 billion.

That increase in withholdings reflects recent increases in wages and salaries,

meaning that the economy is possibly experiencing more people working and at

higher pay rates.

Source: CBO

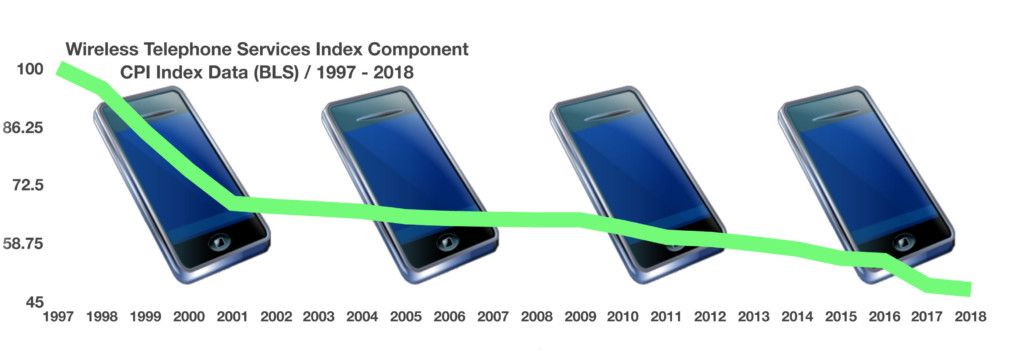

95% OF AMERICANS OWN A CELLULAR PHONE AND PAY A MONTHLY SERVICE FEE

Wireless Rates Are Due To Climb – Consumer Expenditures

Cell phone bills are rising across the country as providers eliminate promotions and

consolidate operations. The announcement of recent mega mergers in the industry has

reduced the number of providers and lessened competition, leading to increased rates for

customers.

As tracked by the Labor Department’s Consumer Price Index (CPI), the cost of cell phone

service is a measurable component of the index. Over the years, cell phone costs have

become a vital and expensive service for consumers nationwide, almost as important as

groceries or rent. It is estimated that roughly 95% of Americans own a cellular phone and

pay a monthly service fee to one of several providers.

Following years of technological advancement and intense competition for market share,

cellular providers kept rates low. Adjusted for inflation, cell rates have consistently fallen in

price since 1997, meaning that as the price for other services rose, cellular rates fell.

The recent mergers and expansion of new cellular infrastructure has begun to raise rates.

Rather than absorbing merger costs and infrastructure build out, cellular service providers

are instead passing along the costs to consumers. The higher fees are considered

inflationary and thus add to the overall inflationary pressures that are gradually rising.

TURKISH CURRENCY, THE LIRA, HAS FALLEN OVER 40% YEAR TO DATE VERSUS THE U.S. DOLLAR

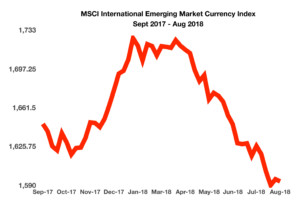

Emerging Market Currencies Experience Volatility – International Currency Review

Currency valuations across the emerging markets are being affected by recent

financial turmoil in Turkey and Argentina. The Turkish currency, the lira, has fallen

over 40% year to date versus the U.S. dollar. The Turkish lira has been the hardest

hit so far this year of all of the emerging market currencies. Emerging market

currencies, as tracked and measured by the MSCI International Emerging Market Index, has had a

continuous decline since the beginning of 2018.

Concerns about the exposure that European banks have to Turkish bonds became a forefront topic for

global bankers. Government spending by Turkey has been equal to that of the government in Greece that

led to the country’s debt crisis in 2012. Circumstances that occurred in Greece are appearing in Turkey as

mounting government debt has hindered the government’s finances and integrity.

The Argentine peso has lost over half its value versus the U.S. dollar so far this year.

A sell-off in the Argentine currency was exacerbated when the president of

Argentina asked the International Monetary Fund to speed up its release of $50

billion in bailout funds for the country.

Ironically, the economic growth and strength of the U.S. dollar has been a catalyst for emerging market

currency turmoil. The problem lies with dollar denominated debt owed by emerging market countries such

as Turkey, Greece, Argentina, and Venezuela. As the U.S. dollar appreciates versus the currencies of these

other countries, the cost to repay the debt increases.

Large international banks and institutional holders of emerging market debt buy

insurance to protect themselves from default, should countries become unable to

pay their debt. The insurance is known as credit default swaps or CDSs. The cost of

insuring debt against a default has risen for various countries over the past few

months, most notably Lebanon, Turkey, Pakistan, and Argentina.

Sources: Bloomberg, Reuters, FRED, IMF

SOME U.S. COMPANIES ARE SEEING AN INCREASE IN SALES AND GROSS MARGINS

Equities Maintain Their Resilience – U.S. Equity Markets

A persistent trade dispute between the United States and China has been lingering

over the financial markets for some time now. Helping to buoy domestic markets

are strong corporate earnings and improving economic data. Earnings from U.S.

companies this quarter are being considered the healthiest since the third quarter of

2009 during the financial crisis.

Some U.S. companies are seeing an increase in sales as well as an increase in gross

margins, considered optimistic by equity analysts. The continued strength of the U.S.

dollar, however, is starting to weigh on earnings for certain companies transacting

business overseas.

The administration has proposed altering quarterly reporting for publicly traded

U.S. companies to a semi-annual basis. Similar proposals have been made by

companies and regulators in the past in order to stem volatility and focus on

earnings. Recent news has focused on some companies going private and shedding

the regulatory hurdles and burden caused by quarterly reporting.

Sources: Bloomberg, Federal Reserve Bank of St. Louis

Products Exempted From New Tariffs…..For Now – Trade Policy

Products Exempted From New Tariffs…..For Now – Trade Policy