Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Macro Overview

The rally in stocks that began following the election in 2016 propelled through 2017 as optimism and expectations that growth oriented policies and tax cuts would materialize. Political turmoil was not a deterrent for the markets, as major U.S. equity indices finished the year at near record levels.

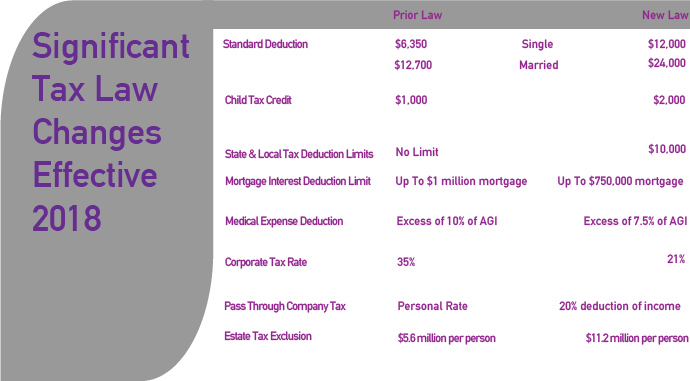

The Tax Cut & Jobs Act was signed into law by the President on December 22nd, setting the stage for new tax codes and rules effective January 1, 2018. Following the passage of the new tax law legislation, small businesses and larger corporations prepare for optimal methods of spending capital and expanding in 2018.

Congress passed a short-term funding plan to avert a government shutdown between December 22nd to January 19th. Since federal funding gaps are common, Congress institutes a continuing resolution or CR to provide interim funds in order to maintain government operations.

Strengthening economic conditions throughout the international markets helped buoy global stocks and mildly boost inflationary pressures, which can be beneficial for certain equities. Economic stimulus efforts by central banks were reigned in during 2017, as developed and emerging market economies exceeded growth expectations.

The Federal Reserve raised rates as expected with the objective of curtailing inflationary pressures. The December rate hike was the third of the year, pushing shorter-term rates higher, which are more sensitive to Fed rate increases. Overall, rates remained fairly stable in 2017, as inflation and economic growth were tepid. The 10-year Treasury yield ended 2017 at 2.40%, down from 2.45% at the beginning of the year.

Commodity prices, including precious metals and energy products, are expected to rise in 2018 as the prospect of inflationary pressures increases. A rise in global oil demand along with curtailment of production pushed prices higher in 2017 to levels not reached in over two years.

Confusion surrounding prepayment of property taxes was a nationwide problem the last week of the year as homeowners rushed to prepay 2018 property tax bills without being certain if a deduction could be taken in 2017. In a statement, the IRS did specify that taxpayers could deduct prepaid 2018 state and local property taxes on 2017 returns only if the taxes were assessed before 2018.

Sources: Congress.gov, Federal Reserve, IRS, U.S. Treasury

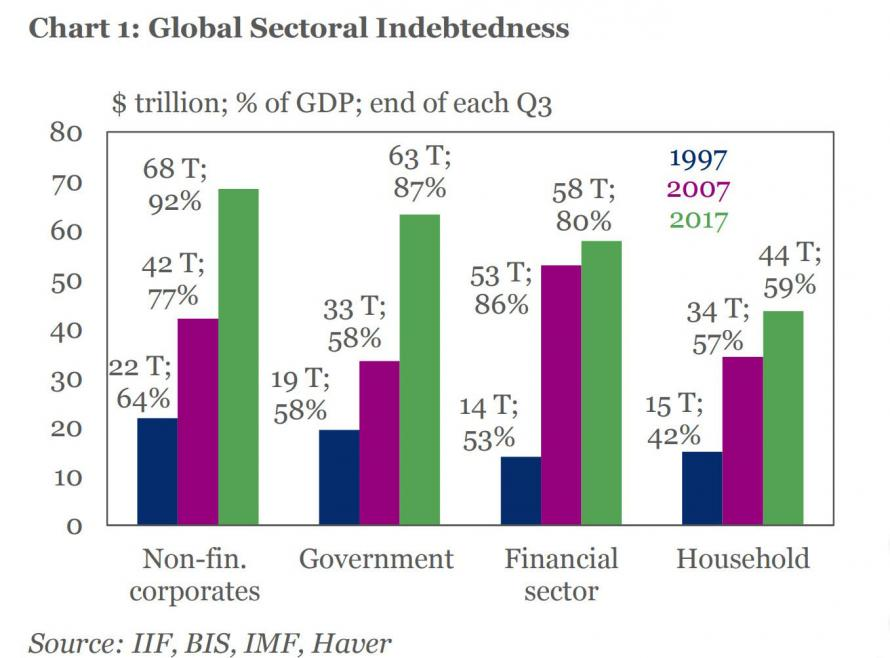

Global debt has now reached $233 trillion, up $16 trillion in six months!! A mere 1% rise in interest rates equates to approximately $1.2 trillion in losses for bond investors. As interest rates continue to rise, liquidity in the credit markets could begin to dry up meaning many borrowers will be paying much higher rates to refinance their debt or even worse the lower credit quality borrowers (high-yield (junk) ) may be unable to obtain financing at any rate resulting in massive defaults. As we have discussed in previously newsletters this could be the trigger that not only slows down the stock market but we believe will ultimate cause a credit crisis that will dwarf the 2008 crisis. Why? Because global debt is nearly $80 trillion higher now than in 2007-2008 and much of this debt is very low quality. (Continued on next page)

Global debt has now reached $233 trillion, up $16 trillion in six months!! A mere 1% rise in interest rates equates to approximately $1.2 trillion in losses for bond investors. As interest rates continue to rise, liquidity in the credit markets could begin to dry up meaning many borrowers will be paying much higher rates to refinance their debt or even worse the lower credit quality borrowers (high-yield (junk) ) may be unable to obtain financing at any rate resulting in massive defaults. As we have discussed in previously newsletters this could be the trigger that not only slows down the stock market but we believe will ultimate cause a credit crisis that will dwarf the 2008 crisis. Why? Because global debt is nearly $80 trillion higher now than in 2007-2008 and much of this debt is very low quality. (Continued on next page)