Stock Indices:

| Dow Jones | 40,669 |

| S&P 500 | 5,569 |

| Nasdaq | 17,446 |

Bond Sector Yields:

| 2 Yr Treasury | 3.60% |

| 10 Yr Treasury | 4.17% |

| 10 Yr Municipal | 3.36% |

| High Yield | 7.69% |

YTD Market Returns:

| Dow Jones | -4.41% |

| S&P 500 | -5.31% |

| Nasdaq | -9.65% |

| MSCI-EAFE | 12.00% |

| MSCI-Europe | 15.70% |

| MSCI-Pacific | 5.80% |

| MSCI-Emg Mkt | 4.40% |

| US Agg Bond | 3.18% |

| US Corp Bond | 2.27% |

| US Gov’t Bond | 3.13% |

Commodity Prices:

| Gold | 3,298 |

| Silver | 32.78 |

| Oil (WTI) | 58.22 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 142.35 |

| Canadian /Dollar | 0.72 |

Where do I begin?! In the pages following, you will read about the series of events that have led us to this point: What economists, market analysts, Fed Presidents past and present, and the administration (including all branches of this government) think about what happens next. What should we expect from the Coronavirus? How will that affect the economy? Uncertainty and our emotions are the driving force on the market and the economy. Rational optimism could be a great tool for, not just living through this crisis, but doing it well.

KCG manages assets and offers advice, not based upon geopolitical events, but with a long-term perspective.

It has been the case in all of our financial crises, that no one (and no government) wants to feel the painful consequences of the actions that led us here. Our first instinct is to do whatever is necessary to eliminate the pain. In this case, the Fed reduces its key lending rate to 0% – 0.25% and re-instates new versions of Quantitative Easing; The Administration gives us The Cares Act. And it works….for now. While these actions provide the economy with some immediate stimulus, mostly a result of society’s emotional responses, even the Fed and the Administration are busy putting the next relief package together because everyone realizes these are not permanent solutions.

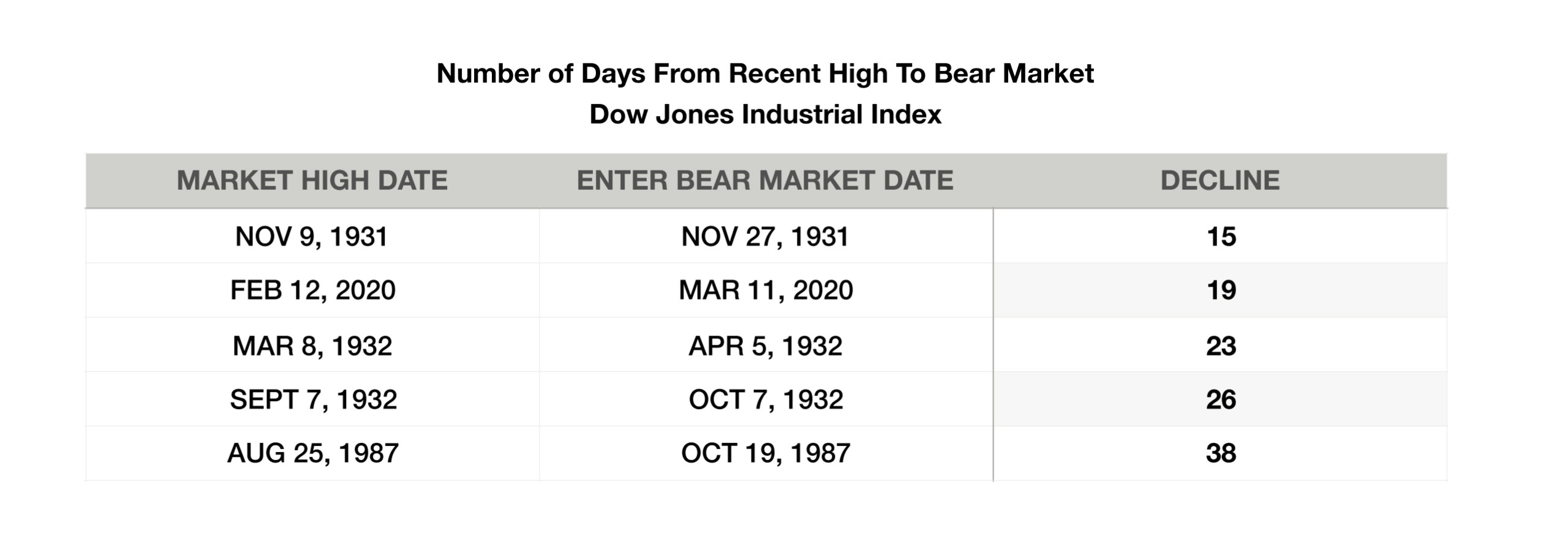

It certainly seems that this is the beginning of the bear market. Bull and bear markets are normal. What was not normal was the unprecedented 11 year bull run. Covid-19 was just the impetus for this bear. Richard Bernstein recently said in an interview, “Bear markets have 3 phases. 1) Investors view it as temporary; 2) It’s worse that expected; 3) Investors feel as if it will never end.” This is just the beginning. This could be the bottom of the “Coronavirus-19 event” market, assuming the health news over the past couple of days continues to improve. There seems to be a light at the end of the tunnel. However, the impact on the economy is yet unknown, and could be far worse than we expect. Not only will we have the consequences of shutting down a third of our economy, and a supply chain that will have to be re-designed, the long-term result of government intervention is yet to come. There is no way of knowing how long we will be able to kick this can down the road but there is getting to be a mountain of cans and sooner or later we won’t be able to kick them all.

Now for the rational optimism…Let’s shift the question from “How long is this going to continue?”, to “What opportunities are there?”

With the re-pricing of securities, KCG has been able to develop three very attractive new model/target portfolios: a traditional Individual Stock Portfolio and ETF Sector Model based upon new fundamentals, and an ESG ETF Model. (For non-millenials, ESG means Environmentally-, Socially-, and Governance- friendly investing.)

For income-oriented portfolios and bond-holders, new opportunities have presented themselves to buy a quarter-liquidity bond fund, FS Credit Income Fund (FCRIX) at the bottom of the market. KCG Clients know that bonds are to be held to maturity, sometimes as long as ten years, in order to generate the assured yield. A somewhat illiquid fund can be viewed in the same way. The upside of that illiquidity is that while great bond funds like PIMCO and Eaton Vance are having to sell good bonds to generate funds for investors to withdraw, interval funds like FS, are able to buy those bonds. They are not having to raise money and rather, can purchase great assets at great prices.