Fairscale Capital, LLC

402 Amherst St. Suite 203

Nashua, NH 03063

603.318.7337

Stock Indices:

| Dow Jones | 40,669 |

| S&P 500 | 5,569 |

| Nasdaq | 17,446 |

Bond Sector Yields:

| 2 Yr Treasury | 3.60% |

| 10 Yr Treasury | 4.17% |

| 10 Yr Municipal | 3.36% |

| High Yield | 7.69% |

YTD Market Returns:

| Dow Jones | -4.41% |

| S&P 500 | -5.31% |

| Nasdaq | -9.65% |

| MSCI-EAFE | 12.00% |

| MSCI-Europe | 15.70% |

| MSCI-Pacific | 5.80% |

| MSCI-Emg Mkt | 4.40% |

| US Agg Bond | 3.18% |

| US Corp Bond | 2.27% |

| US Gov’t Bond | 3.13% |

Commodity Prices:

| Gold | 3,298 |

| Silver | 32.78 |

| Oil (WTI) | 58.22 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 142.35 |

| Canadian /Dollar | 0.72 |

Macro Overview

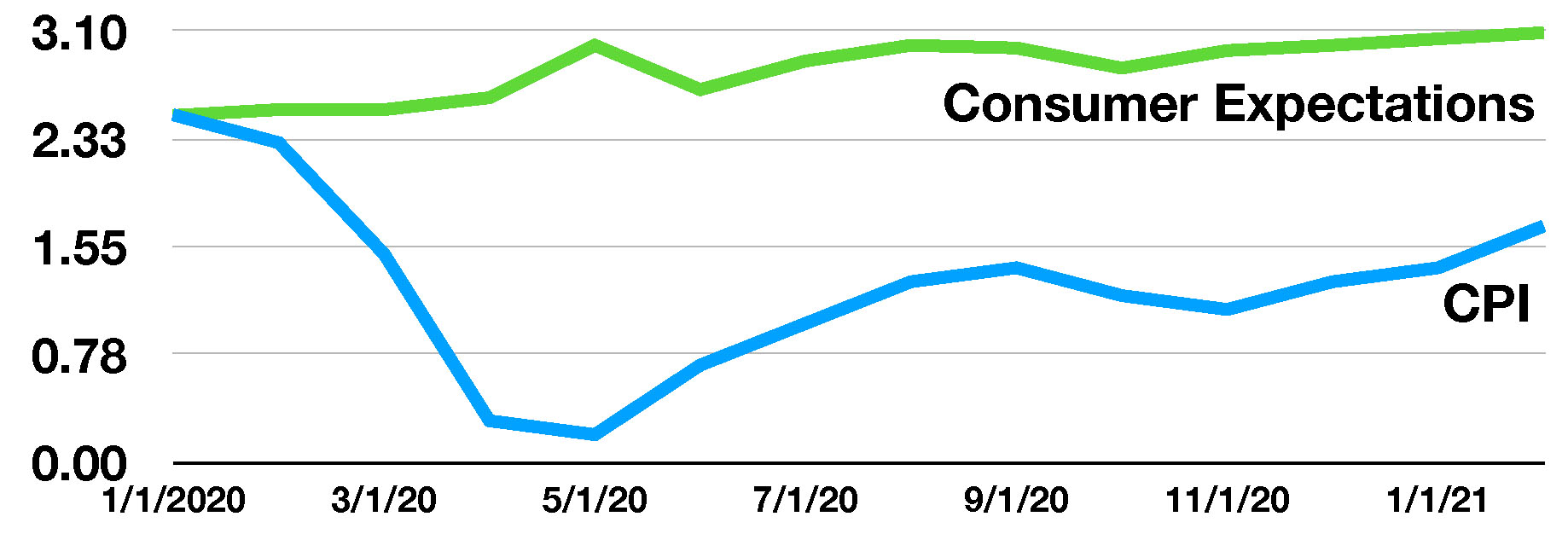

The prospect of resurgent inflation has developed into a growing concern for markets globally. Some believe that current inflationary pressures may be transitory and not lasting, while others contend that higher prices may become more permanent.

Rising fiscal deficits along with increasing levels of federal debt are prompting the administration to explore the most significant tax hikes since 1993. Tax increases are being considered for corporations, businesses structured as pass-through entities, estate taxes, and capital gains.

Optimism surrounding a third round of stimulus payments along with rising vaccination rates fueled equity markets in March as an economic revitalization began to take hold. Major equity indices ended the quarter positively as companies saw a resurgence in activity and sales.

The pandemic has brought about modifications and changes to business models throughout numerous industries, many of which are passing along higher costs to consumers. Many of the higher cost trends are not being recognized by some government inflation gauges and not accounted for in forecasts. The suggestion that inflationary pressures are only temporary are being contested as a growing number of businesses are expected to make pricing changes permanent.

The IRS announced that it is extending the tax filing deadline to May 17th, allowing tax payers more time to assess the effects of COVID related changes for individual and small business filers. With the IRS extending the deadline, nearly all states will follow suit and extend the tax deadline to May 17th as well, but most are maintaining the due date of April 15th for estimated tax payments.

In addition to stimulus payments, the $1.9 trillion bill passed in March, known as the American Rescue Plan Act of 2021, will provide an exemption on taxes paid on unemployment benefits up to $10,200. The IRS communicated that automatic refunds would be issued to those who have already filed their 2020 taxes and have paid taxes on unemployment last year.

A $2.25 trillion infrastructure plan introduced by the administration is expected to focus on transportation, cleaner water, high-speed broadband and manufacturing. An increase in corporate taxes is the primary source of funding the proposed plan.

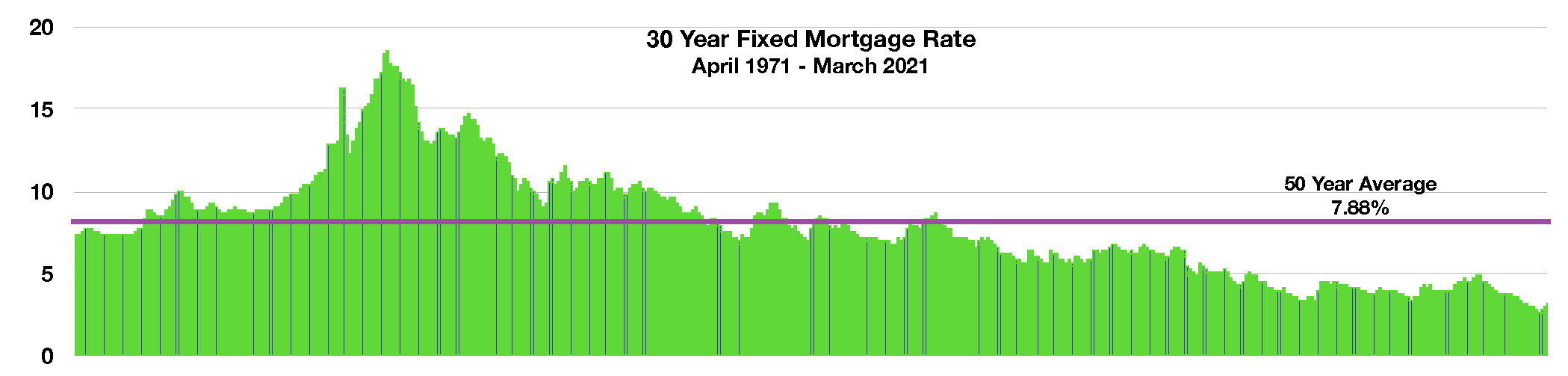

The rapid rise in mortgage rates since the beginning of the year has led to a slowdown on refinances nationwide. The 30-year fixed rate mortgage reached the highest level in over nine months at 3.17% as of March 25th, yet still at historical lows relative to the 50-year average for a 30-year fixed mortgage rate of 7.88%.

Identified mutations of the COVID-19 virus have raised concerns about the spread of a variant known to be more transmissible than the initial virus, prompting the CDC to caution the public about relaxing preventive measures.

Sources: IRS, Federal Reserve, CDC, Congress.gov