Tax On Social Security In Retirement – Retirement Tax Planning

A prudent and effective tax strategy during your employment years will mostly likely need to be modified in retirement. Once earned income ceases and income from retirement plans, investments, and Social Security commences, tax liabilities change.

The impact of the changes is primarily driven by the assets that we have little tax control over once we reach 70.5, which include IRAs, 401ks, and pensions. Reaching age 70.5 triggers RMDs (Required Minimum Distributions). Distributions from tax deferred retirement accounts such as an IRA or a 401k are generally taxed at the ordinary tax rate. Distributions from a Roth IRA or Roth 401k are income tax free as long as the account has been opened for at least five years and the account holder is 59.5.

Investment income such as stock dividends and bond interest are taxed differently, especially when they are held outside of a retirement account. Realizing gains on stocks that have been held for one year or more can be taxed at a more favorable rate than the ordinary rate. Interest on bonds and gains realized on short-term positions less than one year, are taxed at the ordinary rate.

Retirement also introduces us to Social Security which, contrary to popular belief, can be taxed. Eligibility for Social Security benefit payments begins at age 62, but can be postponed until age 70. A key determinant as to when to start receiving Social Security may be contingent on the amount of retirement assets in retirement accounts subject to RMDs. This is where tax strategies can vary dramatically.

Retirees with excessive assets in retirement accounts subject to RMDs and with non-retirement investment income may want to confer with a tax professional to help determine when to take Social Security. Conversely, retirees with minimal assets in retirement accounts and investments may have less concern about paying taxes on their Social Security benefits.

The IRS determines if and how taxes are owed on Social Security by the “provisional income” measure. Provisional income includes gross income, tax-free interest, and 50% of Social Security benefits. If the provisional income is above a certain amount, then a portion of the Social Security income becomes taxable.

One way to potentially lower taxes in retirement is to start taking distributions from tax-deferred accounts before it’s required. Again, once you reach age 59.5, you can withdraw funds from those accounts without paying the 10% early withdrawal penalty. The withdrawals are still taxed as ordinary income, but over time they reduce the size of tax deferred accounts, and thus the size of your RMDs. Another reason to access those funds before 70.5 is that it could help you delay taking your social Security benefit, which increases in size the later you take it, up to age 70.

Another strategy for reducing the potential tax consequences of RMDs is converting a traditional IRA or 401(k) plan into a Roth IRA before the age of 70.5. A Roth conversion may make sense when you’re certain you’ll be in a higher bracket when you eventually withdraw the money, which is often the case once RMDs and Social Security are factored in.

(Sources: Social Security Admin., IRS, Tax Policy Center)

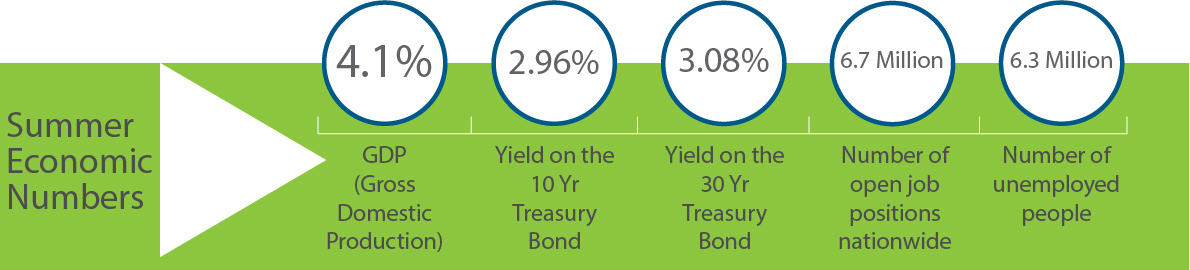

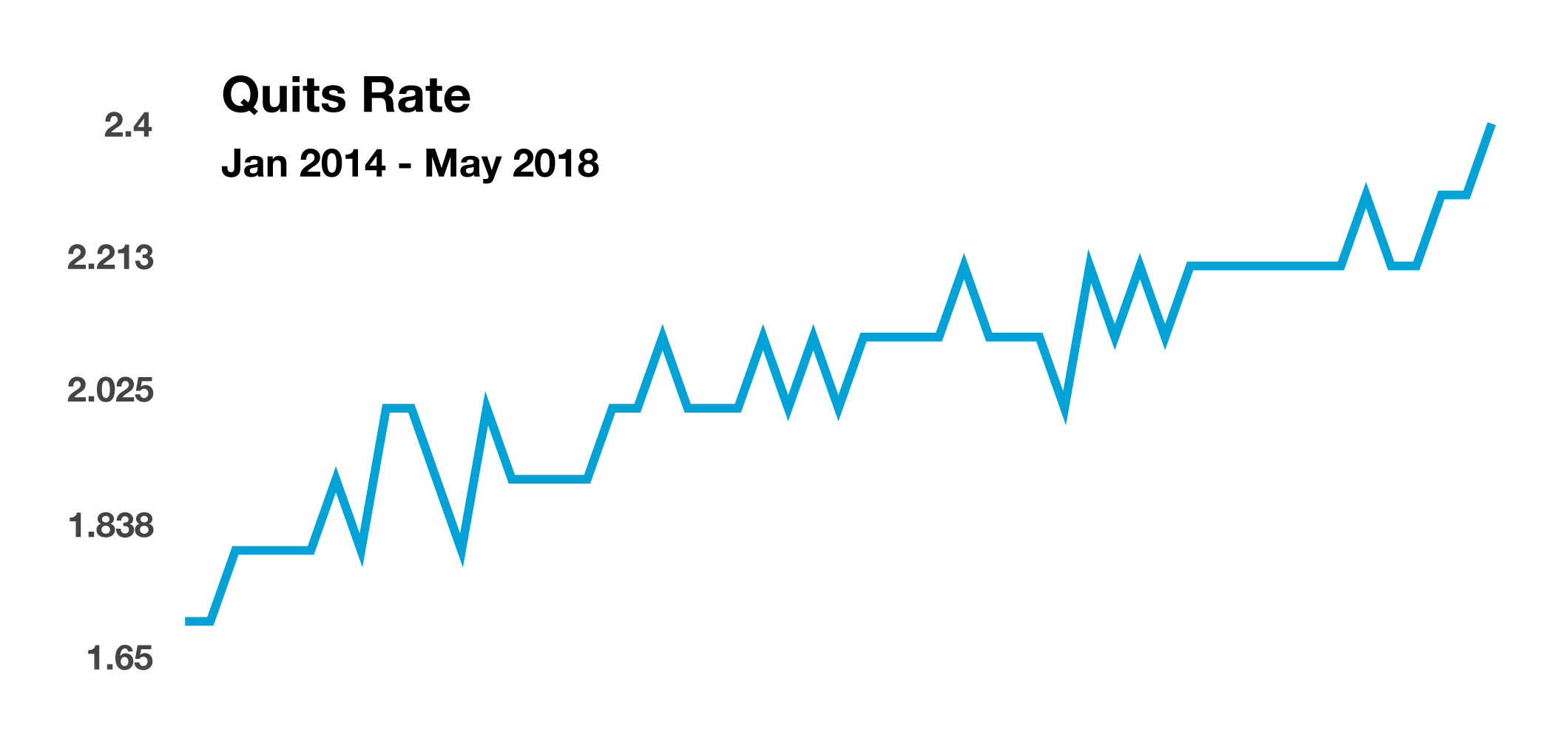

lysts follow the quits rate closely because it reveals how confident workers are. These same workers are also the consumers that the Fed monitors to determine if their confidence is allowing them to spend more, thus lifting economic growth. The most current quits rate rose to 2.4 in May, the highest monthly reading in over 10 years. Following the financial crisis in 2008, the quits rate dropped as workers were less confident in leaving a job they had rather than look for another job opportunity. (Sources: U.S. Labor Department)

lysts follow the quits rate closely because it reveals how confident workers are. These same workers are also the consumers that the Fed monitors to determine if their confidence is allowing them to spend more, thus lifting economic growth. The most current quits rate rose to 2.4 in May, the highest monthly reading in over 10 years. Following the financial crisis in 2008, the quits rate dropped as workers were less confident in leaving a job they had rather than look for another job opportunity. (Sources: U.S. Labor Department) at is not prevalent with existing home sales.

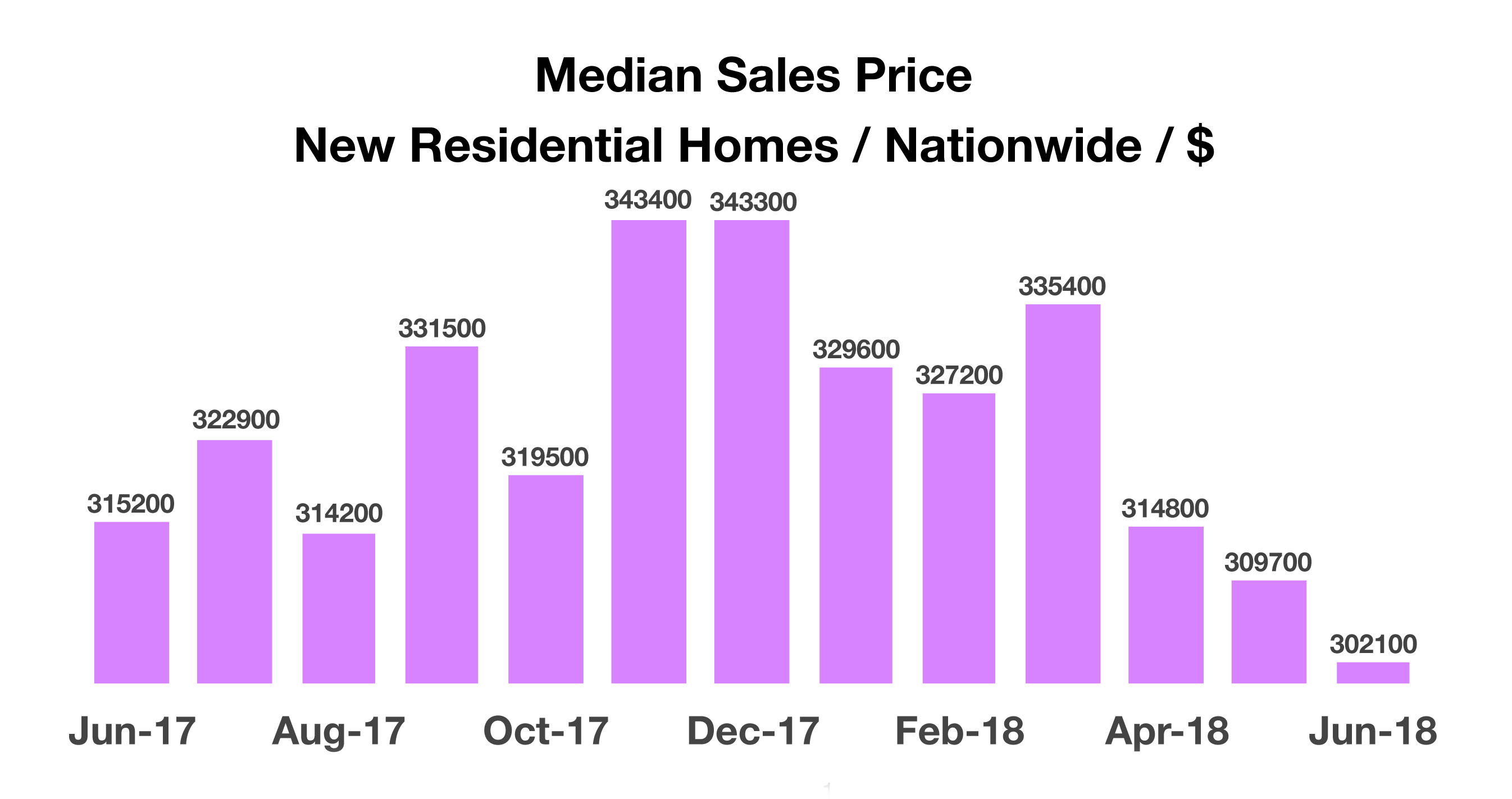

at is not prevalent with existing home sales.