Joseph Schw arz, CFA 612.355.4365

arz, CFA 612.355.4365

Stephen Dygos, CFP® 612.355.4364

Benjamin Wheeler, CFP® 612.355.4363

Paul Wilson 612.355.4366

www.sdwia.com

Stock Indices:

| Dow Jones | 40,669 |

| S&P 500 | 5,569 |

| Nasdaq | 17,446 |

Bond Sector Yields:

| 2 Yr Treasury | 3.60% |

| 10 Yr Treasury | 4.17% |

| 10 Yr Municipal | 3.36% |

| High Yield | 7.69% |

YTD Market Returns:

| Dow Jones | -4.41% |

| S&P 500 | -5.31% |

| Nasdaq | -9.65% |

| MSCI-EAFE | 12.00% |

| MSCI-Europe | 15.70% |

| MSCI-Pacific | 5.80% |

| MSCI-Emg Mkt | 4.40% |

| US Agg Bond | 3.18% |

| US Corp Bond | 2.27% |

| US Gov’t Bond | 3.13% |

Commodity Prices:

| Gold | 3,298 |

| Silver | 32.78 |

| Oil (WTI) | 58.22 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 142.35 |

| Canadian /Dollar | 0.72 |

Macro Overview

Markets have been undermined for weeks by the uncertainty of a phase-one trade deal outlined by U.S. and Chinese trade delegates. Optimism for a probable U.S.-China trade deal stemmed from the progression toward a phase-one deal that might include a rollback of certain tariffs by both the U.S. and China.

Global equity markets continued to elevate in November against a backdrop of political events and optimism surrounding ongoing trade negotiations. With the year end approaching, focus has shifted to the 2020 election, a phase-one trade deal, the Fed maintaining rates, and receding recession concerns.

A broad barometer of the current status of the country’s economic well being is the money supply, which essentially measures the level of cash in savings accounts, checking accounts, CDs, and money market funds. Money supply has grown over 10% during the past quarter, translating into plenty of excess liquidity for financial markets and providing a buffer against any unexpected volatility.

Fixed income analysts expect that the Fed is attempting to normalize interest rates by holding off on any further rate changes until economic data offers a clearer view of where the economy is headed. Analysts believe that subdued inflation exceptions by the Fed may leave rates steady heading into 2020.

There are less global bonds yielding negative rates, down to $11.9 trillion from a peak of $17 trillion in the summer. Lessening negative yields is indicative of a possibly stronger global economy, sparking a drive to equities to capture growth prospects. Some believe that the president’s objective of a weaker U.S. dollar would be beneficial for both international equities and exports of U.S. products around the world.

Consumers continue to spend at retail stores and on food heading into the holiday season, buoying economic activity throughout the country. Consumer expenditures represent over two-thirds of GDP, an integral part of the nation’s economy. A continued low-rate environment, along with a strong job market, has allowed consumers to spend generously on retail and food.

(Sources: Commerce Dept., Bloomberg, Federal Reserve, BLS)

Looks Like QE But It’s Not Says The Fed – Fixed Income Overview

The Federal Reserve is slowly re-expanding its balance sheet by currently buying $60 billion of Treasury bills each month. Reminiscent of the Fed’s Quantitative Easing (QE) program, meant to stimulate economic activity, the Fed denies that it is QE, but rather just a buffer for any possible bond market volatility.

Interest rates are believed to have stabilized for the time being, as the Fed has essentially placed a hold on raising and lowering rates until further notice. The yield on the 10 year treasury bond ended November at 1.78%, essentially where it’s been for the past two months.

The presidential race is promoting bond buyers to consider municipal bonds in order to hedge against any possible increase in tax rates. The tax free interest generated by municipal bonds has historically been a benefit for certain investors in the higher tax brackets.

Sources: Federal Reserve

Global Markets Elevate – Equity Review

Domestic equities finished November with gains not seen since the summer.

Optimism surrounding U.S.-China trade discussions helped fuel equities higher, with technology, health care, and financials as the leading sectors in November.

The absence of volatility, along with the Fed maintaining a steady rate environment, was also a catalyst for equities to climb in November. Stock market volatility, as measured by the VIX Index, dropped to its lowest levels since April.

U.S. equity markets have outperformed international equities over the past two years so far. Historically, a lower U.S. dollar has benefited international stocks, as well as help increase exports of U.S. products worldwide.

(Sources: U.S. Commerce Department, Bloomberg)

Medigap Plan F Phasing Out – Medicare Benefits Update

Of the ten Medicare supplemental plans, known also as Medigap, the single most popular plan, Plan F, will be eliminated at the end of the year to new subscribers.

Retirees who turn 65 after 2019 will no longer have Plan F as an option. Plan F is the most expensive supplemental option since there are no deductibles, no co-pays and no additional bills after a doctor’s visit.

Plan G has become the next best comprehensive plan after Plan F is phased out to newcomers. Plan G is almost identical to Plan F with the exception of having to pay the Medicare deductible before insurance pays any benefits.

A Medigap policy supplements expenses not covered by Medicare including co-payments, co-insurance, and deductibles. Medigap policies are sold by private insurance companies and vary in pricing and coverage from state to state.

The following are important aspects regarding Medigap policies:

In order to have Medigap coverage, one must have Medicare Part A & Part B.

A Medigap policy only covers one person, not a married couple. So, each person needs their own separate policy.

Any standardized Medigap policy is guaranteed renewable even with a pre-existing condition.

Medigap does not cover prescription drugs. Medicare Part D does offer coverage for prescription drugs.

Medigap policies generally don’t cover long-term care, vision, dental care, hearing aids, eyeglasses, or private nursing.

Sources: medicare.gov

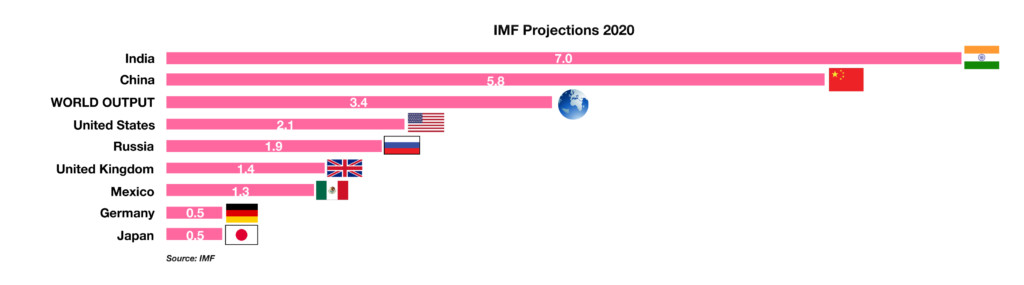

Global Growth Expected To Slow – World Economy

Every year the International Monetary Fund (IMF) releases a report on its outlook for worldwide economic growth. The IMF is an international organization consisting of 189 countries working to foster global financial cooperation. In its most recent report released in October, the IMF noted that the global economy is in a synchronized slowdown with a projected growth rate of 3.4% worldwide in 2020. The subdued projections are a consequence of rising trade barriers, uncertainty surrounding trade and geopolitics, low productivity rates, and strain in the emerging market economies.

The IMF is estimating a 3% growth rate for the global economy in 2019, a drop from 3.6% in 2018. Among those countries expected to see a decline in growth are China, Japan and the United States. China’s forecast is primarily due to trade tensions and a drop in exports. India continues to grow at a favorable rate among both the emerging and developed economies. Its projection of a 7% growth rate for 2020 is greater than all other major emerging and developed economies.

Source: International Monetary Fund