Please welcome the newest members of the LifeMark team

Joshua Weaver – Beaumont, TX

Dabney McMurray – Hattiesburg, MS

Upcoming sales teleconferences

February 13 @ 2PM EST

GWG Life Settlements / Alternatives

March 14 @ 2PM EST

Prudential Annuities

Connections – LifeMark & Upstate Andy Kalinowski: The question “Why LifeMark” also applies to Upstate Special Risk Services.If you are reading this article, you have answered the “Why LifeMark” question, since you are likely already registered with LifeMark. However, because LifeMark does not require its representatives to place their non-securities business with a particular outlet, it is quite possible that you came to LifeMark having other existing relationships for that business. So the question “Why Upstate” is a good one and should be addressed.From an historical perspective, Upstate could be called the mother of LifeMark. Many years ago, Upstate, in its long-range planning, determined that the financial/insurance world was changing. We believed that if we were to retain our independence, it would be necessary to also be in the securities business. That observation lead to the birth of LifeMark. The world is changing again – this time more dramatically and rapidly. All firms in the financial services industry, as well as their advisor associates, will need to change to be relevant and survive. The LifeMark/Upstate team provides you with access to nearly every kind of product, service, system, advice and guidance you may require in serving your clients and to grow your practice. These resources are available to you in one place, delivered by folks who understand your practice and see you as a member of our extended family.

We will use the net proceeds we raise in this offering to primarily invest in income-producing and growth self storage properties in the United States and Canada that are expected to support sustainable stockholder distributions over the long term while also achieving appreciation in the value of our properties and, hence, appreciation in stockholder value. At the end of our acquisition phase, we anticipate that our portfolio will consist of approximately 75% income-producing properties and 25% growth properties, though the specific allocations may vary at any point in time.

Broadridge is the premier provider of advisor marketing solutions designed to help you find new prospects, retain and grow business with existing clients, and increase referrals while optimizing your practice.

Gateway: Build and Grow Website / Sponsored Name Placement / Social Sharing / Advisor Resource Center / Continuing Education

Journey: Grow and Communicate

Website \ Sponsored Name Placement \ Social Sharing \ eNewsletters \ eCards \ Advisor Resource Center \ Seminars \ Continuing Education

Destination: Preserve and Manage

Website / Social Sharing / eNewsletters / eCards / Advisor Resource Center / Continuing Education

Rising interest rates weighed on equity momentum as the expectation of increased borrowing costs and inflation accelerated market volatility. Markets retreated from gains established earlier in the year as higher global yields precipitated a pullback in domestic and international equities.

A synchronized global recovery has become the catalyst for increases in commodity prices, inflation and economic growth. Recent oil demand increases by emerging countries have stoked inflation pressures internationally, while news of higher wages in the U.S. fueled further acceleration of inflation fears, driving down bond prices and elevating bond yields. The rise in rates is affecting a broad spectrum of loans from auto and personal to mortgages. The ascent of interest rates in January is expected to continue throughout the year as the Fed slowly starts to unwind its expansive stimulus efforts.

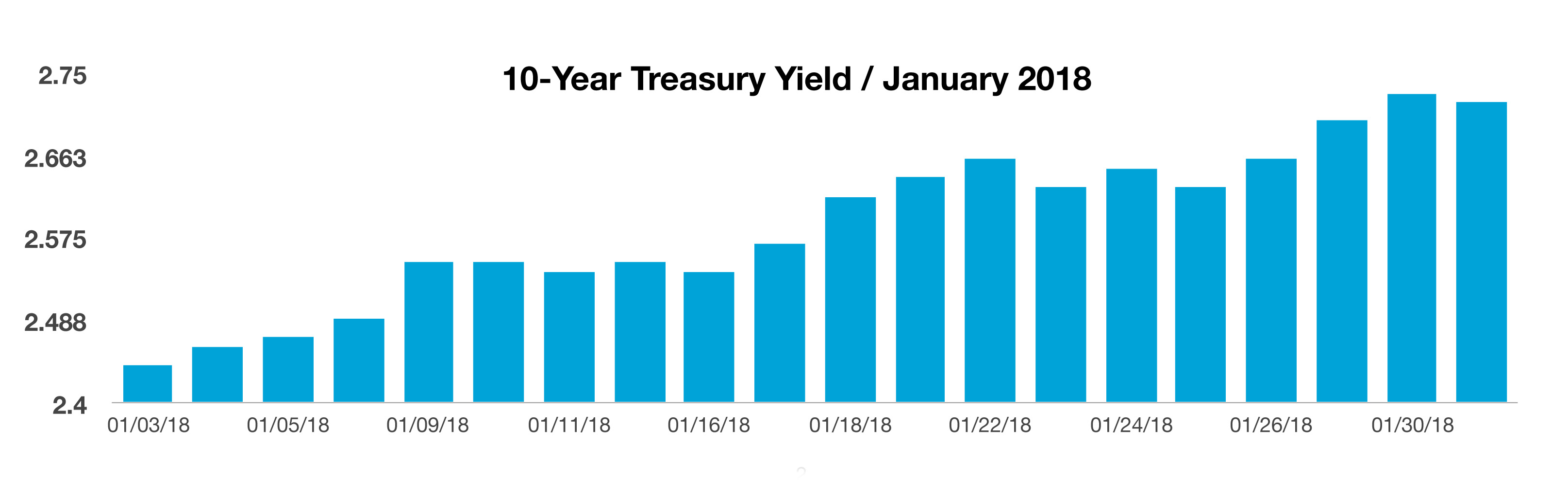

The 10-year Treasury bond yield recorded its steepest monthly increase since November 2016 with short-term and long-term Treasury yields remaining in the tightest range in a half-century. Low rates have allowed companies to borrow cheaply and have forced investors to seek out riskier assets to meet return objectives.

The recent tax changes now allow U.S. corporations to repatriate cash funds overseas and pay a 15.5% tax rather than 35%. An estimated $300 billion is expected to slowly start returning to the United States over the next few months, leading to stock buybacks, hiring, capital investment, and dividend payout increases.

World financial, political and intellectual leaders gathered in Davos, Switzerland, for the annual World Economic Forum. President Trump was the first U.S. president to attend since Bill Clinton in 2000. U.S. representatives discussed plans of establishing revised business and trade arrangements with several nations in attendance.

The Federal Reserve Bank of Atlanta revised its economic growth forecast to 5.4% for the first quarter of 2018, an optimistic revision following improving economic data. The forecast is generated by a model, known as the GDPNow model, which takes various factors into account. The model is also forecasting an increase in consumer spending from 3.1% to 4.0% and an increase in real private fixed investment growth from 5.2% to 9.2%, both significant components for sustainable economic growth.

Sources: Atlanta Fed Bank, Treasury Dept.,www.weforum.org/

Volatility Returns To The Market – Equity Overview

Optimism and positive sentiment surrounding earnings and growth estimates fueled equities in January, lifting equity indices to new highs. The S&P 500 achieved its 10th consecutive monthly gain in January, the longest 11-month winning streak for the index since January 1959.

Stocks receded towards the end of January as rising interest rates and the onset of inflationary tensions elevated market volatility. Bonds pressured U.S. stocks as the two-year Treasury yield reached 2.12 percent, compared with the 1.76 percent dividend yield on the S&P 500. The 2-year Treasury yield surpassed the S&P 500 Index dividend yield for the first time in nearly ten years.

Even at the levels that the major indices have risen to, stocks are still fairly valued historically per the S&P 500 Index earnings estimates at 18 times for 2018. January 2018 was the best January for the stock market since 1997. (Sources: S&P, US Treasury, Bloomberg)

Yields Head Higher – Fixed Income Update

Rising global bond yields precipitated a sell off in stocks as the cost to borrow for companies and governments rose. A host of factors are contributing to rates rising including: the ECB, Japan, and Federal Reserve all ending years of stimulus efforts; rising wages; and global economic growth. International bond yields rose in tandem with rising U.S. treasury yields, elevating the 10-year German bund out of negative yields.

As with companies, municipalities may be hit with higher interest rates resulting in saddling state and local government budgets producing increased borrowing costs. Further yet, rising rates may also prevent certain municipalities from taking steps to shore up their underfunded pension plans.

In its January meeting, the Fed did nothing to discourage expectations that it will continue to tighten monetary policy when it meets again in March. The Fed has officially begun to unwind its post financial crisis stimulus process, which entails raising short-term rates and reducing its $4.4 trillion balance sheet.

The Fed is now on track to raise short-term rates three times this year, since it has met its dual mandate of maximum employment with stable inflation. Any additional growth resulting from the recent tax cuts may entice the Fed to raise rates a fourth time this year should it be warranted.

The Treasury Department plans to increase the size of its bond and note auctions by $42 billion in order to meet funding requirements for the government. It also stated that it would only be able to fund government operations through the end of February unless congress raises the debt ceiling.

(Sources: Fed, US Treasury)

New IRS Tax Withholding Tables – Tax Planning

Because of the new tax law provisions this past month, 90% of wage earners will see an increase in their paychecks due to revised withholding rates, according to the administration. The effect of the revisions will be noticeable in early February, or as soon as employers adopt the new withholding tables, which are required to be in place no later than February 15th.

Withholding tables are used by payroll services and employers to determine how much tax to withhold on employee checks. The new tables reflect the increase in the standard deduction, repeal of personal exemptions and tax rate modifications.

According to the IRS, the new tables should produce more precise tax withholding, thus reducing overpayments that result in excessive tax refunds. The idea is to have just the right amount withheld, not too much and not too little. The IRS is also suggesting that form W-4 be revised to account for changes with itemized deductions, child tax credit, dependent credit, and repeal of dependent exemptions.

Mortgage Rates Starting To Rise – Mortgage Market Update

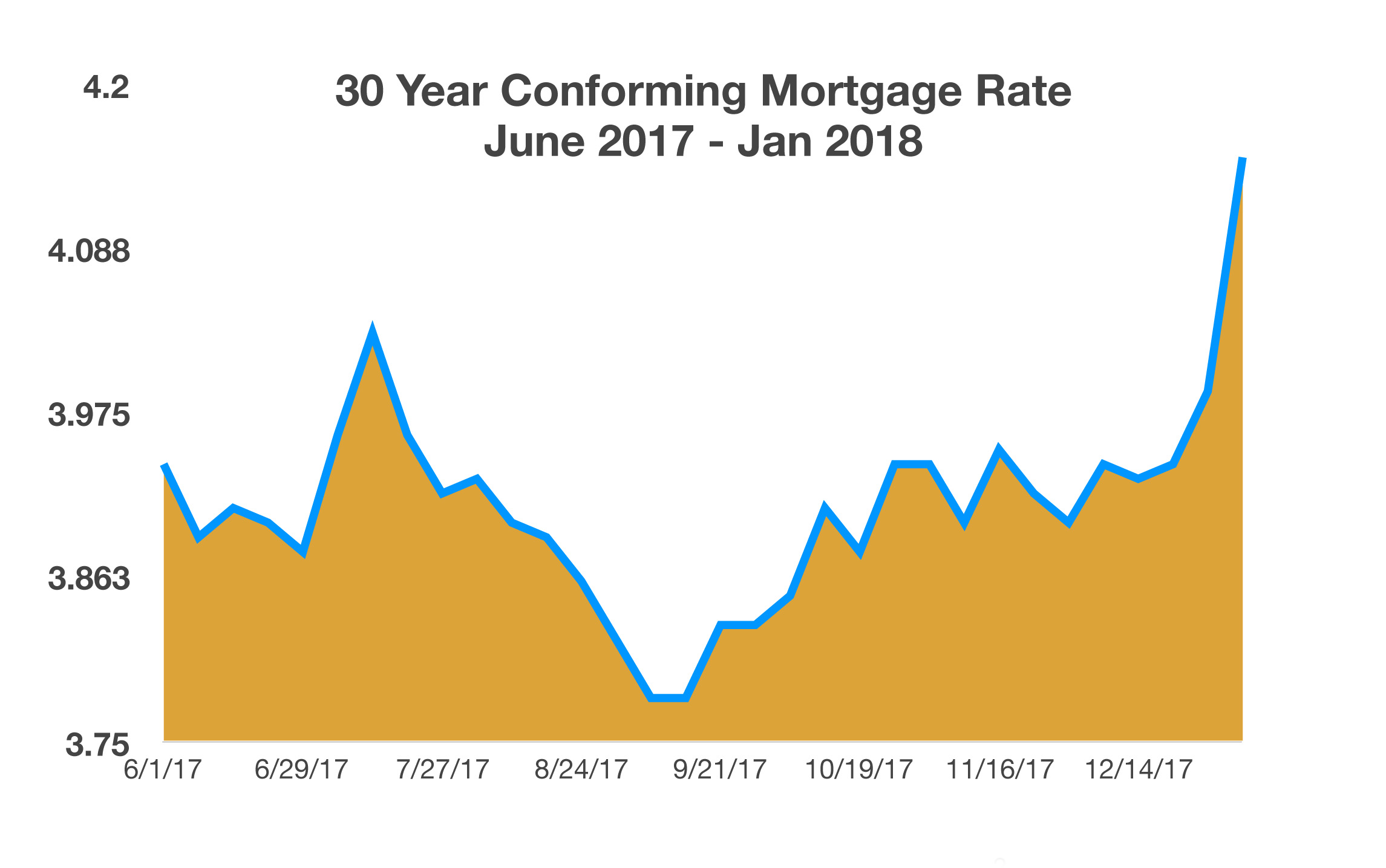

Optimism about economic growth has led to higher inflationary expectations, which eventually translate into higher interest rates. Over the past few months, the yield on the 10-year U.S. Treasury has increased from a historical low of 1.35% in 2016 to 2.72% at the end of January. As a gauge for mortgage rates nationally, the increase in the 10-year Treasury has also led to an overall increase in mortgage rates. According to data made available by Freddie Mac, the average rate on a 30-year fixed mortgage loan increased to 4.15% at the end of January. The concern economists have is that as mortgage rates continue to increase, home sales and affordability may begin to falter.

Thirty-year mortgage rates have surged to the highest levels in nearly a year, increasing borrowing costs at a time when the housing market is strengthening and prices have been rising. The 4.15% rate at the end of January was the highest rate since March 2017 and above 4 percent for the first time since May 2017. The average 15-year mortgage rate climbed to 3.62 percent from 3.39 percent.

Even with the recent rise in mortgage rates, rates are still low on a historical basis. As of this past month, the average mortgage rate since 1971 has been 8.16%. Over the past 46 years, mortgage rates have transitioned from the 5% range in the early 70s to over 14% in the late 70s and early 80s, with the 30-year conforming rate hitting a record high of 16.63% in 1981. (Sources: Freddie Mac, Bloomberg, U.S. Treasury)

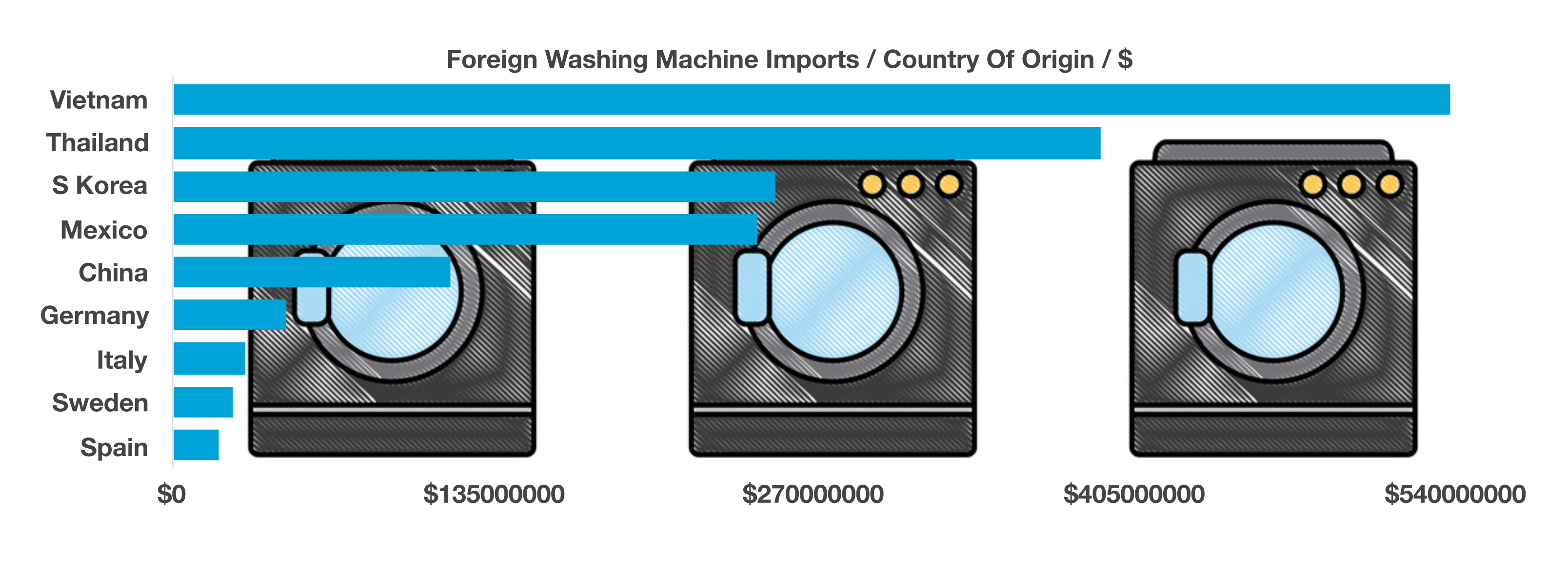

Washing Machines & Solar Panels Subject To New Import Tariffs – Trade Policy

Inexpensive imports inundating the U.S. consumer market have become a target for the Trump administration. The Commerce Department has been given the task of identifying imported products where U.S. producers and manufacturers may experience unfair trade characteristics. The low cost of labor overseas has made it nearly impossible for U.S. manufacturers to compete with, especially in labor intensive industries.

Various U.S. manufacturers have been complaining about foreign manufacturers dumping their products in the U.S. in order to gain market share. Dumping is a practice when manufacturers export a product to another country at a price below their costs or below market prices. The U.S. Dept of Commerce monitors such activities and has filed various complaints with the World Trade Organization (WTO) over the practices. The WTO did recognize violations and identified several manufacturers using unfair trade practices.

This past month the Department of Commerce imposed higher tariffs on the imports of washing machines and solar panels manufactured overseas. The bulk of washing machines imported into the United States are from Asian countries including Vietnam, Thailand, and South Korea. The tariff on washing machines will start at 20 percent on the first 1.2 million units, then increase to 50% on every other unit after that. It is expected that the higher cost brought about by the tariffs will be passed along to American consumers by the foreign manufacturers. Solar panels imported into the U.S. will be imposed a 30 percent tariff the first year, dropping to a 15 percent tariff in the fourth. (Sources: Dept. of Commerce, WTO)

Consumer Spending Growing Faster Than GDP – Consumer Economics

The past four years have seen consumer spending exceeding GDP. Various factors drive consumer spending, including sentiment, optimism, wages, and demographics. GDP grew at a 2.6% annual rate in the fourth quarter, while consumer spending grew at a 3.8% annual rate. Historically, periods where consumer spending has grown faster than economic growth, as measured by GDP, inflation has evolved. Consumer expenditures include the purchase of furniture, appliances, food, autos, and recreational activities. Recent data from the Department of Labor show that consumers have more disposable income to spend. Economists believe that since consumer expenditures represent nearly 70% of GDP, it’s only a matter of time before GDP catches up. (Sources: Dept of Commerce, BEA)

Andy Kalinowski: The question “Why LifeMark” also applies to Upstate Special Risk Services.If you are reading this article, you have answered the “Why LifeMark” question, since you are likely already registered with LifeMark. However, because LifeMark does not require its representatives to place their non-securities business with a particular outlet, it is quite possible that you came to LifeMark having other existing relationships for that business. So the question “Why Upstate” is a good one and should be addressed.From an historical perspective, Upstate could be called the mother of LifeMark. Many years ago, Upstate, in its long-range planning, determined that the financial/insurance world was changing. We believed that if we were to retain our independence, it would be necessary to also be in the securities business. That observation lead to the birth of LifeMark. The world is changing again – this time more dramatically and rapidly. All firms in the financial services industry, as well as their advisor associates, will need to change to be relevant and survive. The LifeMark/Upstate team provides you with access to nearly every kind of product, service, system, advice and guidance you may require in serving your clients and to grow your practice. These resources are available to you in one place, delivered by folks who understand your practice and see you as a member of our extended family.

Andy Kalinowski: The question “Why LifeMark” also applies to Upstate Special Risk Services.If you are reading this article, you have answered the “Why LifeMark” question, since you are likely already registered with LifeMark. However, because LifeMark does not require its representatives to place their non-securities business with a particular outlet, it is quite possible that you came to LifeMark having other existing relationships for that business. So the question “Why Upstate” is a good one and should be addressed.From an historical perspective, Upstate could be called the mother of LifeMark. Many years ago, Upstate, in its long-range planning, determined that the financial/insurance world was changing. We believed that if we were to retain our independence, it would be necessary to also be in the securities business. That observation lead to the birth of LifeMark. The world is changing again – this time more dramatically and rapidly. All firms in the financial services industry, as well as their advisor associates, will need to change to be relevant and survive. The LifeMark/Upstate team provides you with access to nearly every kind of product, service, system, advice and guidance you may require in serving your clients and to grow your practice. These resources are available to you in one place, delivered by folks who understand your practice and see you as a member of our extended family.

One of the newest members

One of the newest members

ing grew at a 3.8% annual rate. Historically, periods where consumer spending has grown faster than economic growth, as measured by GDP, inflation has evolved. Consumer expenditures include the purchase of furniture, appliances, food, autos, and recreational activities. Recent data from the Department of Labor show that consumers have more disposable income to spend. Economists believe that since consumer expenditures represent nearly 70% of GDP, it’s only a matter of time before GDP catches up. (Sources: Dept of Commerce, BEA)

ing grew at a 3.8% annual rate. Historically, periods where consumer spending has grown faster than economic growth, as measured by GDP, inflation has evolved. Consumer expenditures include the purchase of furniture, appliances, food, autos, and recreational activities. Recent data from the Department of Labor show that consumers have more disposable income to spend. Economists believe that since consumer expenditures represent nearly 70% of GDP, it’s only a matter of time before GDP catches up. (Sources: Dept of Commerce, BEA)