Joseph Schw arz, CFA 612.355.4365

arz, CFA 612.355.4365

Stephen Dygos, CFP® 612.355.4364

Benjamin Wheeler, CFP® 612.355.4363

Paul Wilson 612.355.4366

www.sdwia.com

Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Macro Overview – January 2020

Financial markets experienced a bountiful decade for stocks and bonds, as a low rate environment fostered by the Federal Reserve and technological advances driven by innovation, catapulted values higher. The 2010 decade was the first decade to avoid a domestic economic recession, with accelerated growth in various sectors including technology, healthcare, and industrials.

A calm in the markets was displaced as tensions in the Middle East spurred concern early in the new year. Global equity, bond and commodity markets reacted to developments in the region that unleashed a wrath of unease.

International markets advanced in 2019, propelled by low interest rates and a gradual global expansion. Robust gains in global equity markets came about against a backdrop of negative rates in parts of the world, traditionally representative of dismal economic dynamics. Historically low rates during the past decade also incentivized governments and companies worldwide to borrow, boosting growth in expansion and capital investments globally.

A proposed phase-one trade deal between the U.S. and China helped elevate market indices this past year, yet many believe that a more substantive agreement won’t materialize as soon as hoped.

The Federal Reserve plans to keep rates where they are, with no expected increases or decreases unless inflationary pressures become prevalent. Inflation has been surprisingly contained even with the unemployment rate at a 50-year low along with a gradual economic expansion. Accommodative monetary policies initiated by the Federal Reserve were instrumental in both equity and fixed income market expansion during the past decade.

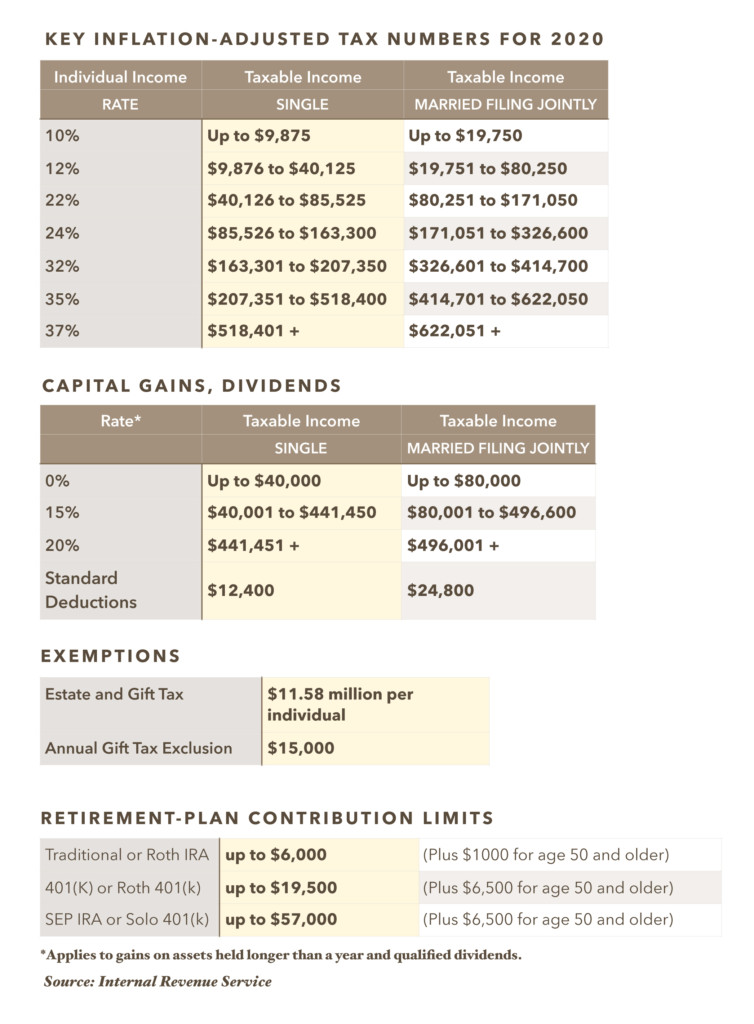

The IRS is providing annual inflation adjustments for over 60 tax provisions, including tax rate schedules, exemptions, and standard deductions. Notable increases affecting many tax payers include the standard deduction for married, filing jointly up to $24,800, and 401k contribution limits up to $19,500 for 2020. The tax code allowing for a $3,000 write off for capital losses, such as on stocks and mutual funds, is an unindexed provision that isn’t changing, which hasn’t had an increase since 1977.

The Federal Reserve continued to inject liquidity into the financial markets via buying bonds and actively participating in the repo market at the end of 2019. Many analysts believe that the Fed’s actions have dampened volatility ensued by the recent upheaval in the Middle East.

It is expected that federal tax revenues and the federal budget deficit should both benefit from the rise in the equity markets and the continued low rate environment. Sources: IRS, Labor Dept., Federal Reserve, CBO.gov., U.S. Treasury, Tax Policy Center

Global Equities Advanced In 2019 – Stock Market Overview

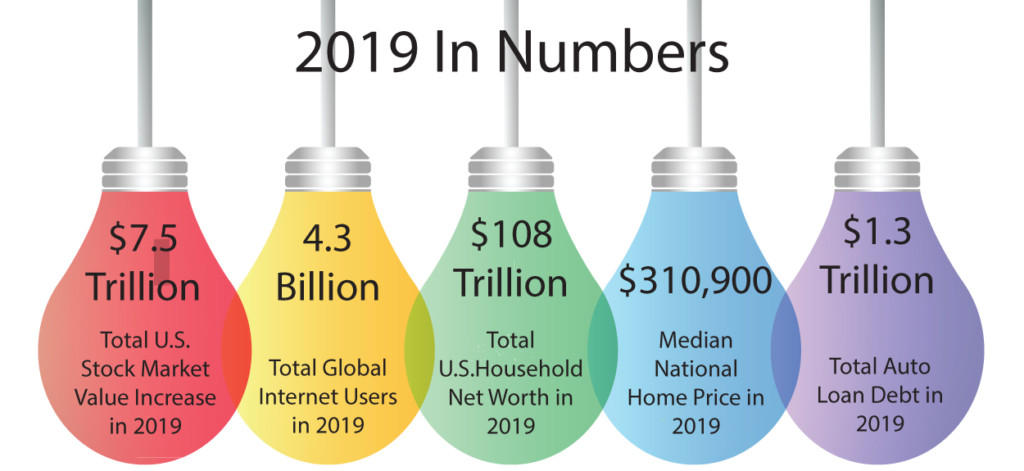

In sharp contrast to 2018, equity markets advanced in 2019 with gains not seen since 2013. Technology, financials, and communications were the leading S&P 500 sectors in 2019. Total stock market value increased $7.5 trillion for the year.

The equity market rebound from its topple in December 2018 was unexpected by many analysts, as 2019 began with expectations of a recession and further market downturn. International markets also advanced broadly in 2019, with gains in the developed and emerging markets.

Global bond markets have been favorable for stocks as historically low rates during the past decade incentivized governments and companies worldwide to borrow, boosting growth in expansion and capital investments globally.

The price/earnings ratio for the S&P 500 Index ended 2019 at 18.3, up from 15.6 at the end of 2018. Analysts view this ratio as an indicator as to how fairly valued the equity market is.

Sources: Bloomberg, S&P

Rates Expected To Stay Steady – Global Fixed Income Overview

Fixed income markets are expecting that the Federal Reserve will maintain interest rates steady through 2020, with no anticipated increases or decreases. Performance was positive across all bond sectors in 2019, with yields stabilizing towards the end of the year.

Ending the year at 1.92%, the yield on the 10-year Treasury bond is still the highest yield available among the developed government bond market. Government bond yields in developed economies such as Germany and Japan were still negative at the end of the year.

To shore up liquidity at the end of 2019 to avert a market disruption, as occurred in December 2018, the Fed injected billions of dollars into the repurchase-agreement market, also known as the repo market, and also bought roughly $400 billion of bonds since October 2019. The strategy has been very similar to the Fed’s quantitative easing program enacted during the financial crisis, also known as Q.E.

Sources: Federal Reserve, U.S. Treasury

The Secure Act – Key Provisions Affecting Retirement & College Savings Plans

Retirement plan legislation passed by Congress effective 2020 includes changes affecting millions of American retirees. The Setting Every Community Up For Retirement Enhancement Act, known as the Secure Act, was signed into law by the president on December 20th. Provisions of the law are intended to facilitate retirement savings for small company workers, offer additional distribution options for 401(k) participants, redraft inherited IRA rules, and increase the required minimum distribution age on IRAs.

Inherited IRAs / Stretch IRAs

Rules surrounding the distribution of funds from an Inherited IRA have changed by accelerating the distribution and taxation of Inherited IRA funds going to non-spouses. Those most affected by the new rules are retirees with generous IRA balances intending to leave funds to their children and grandchildren. Also referred to as Stretch IRAs, inherited IRAs have allowed IRA beneficiaries to stretch distributions and taxes over an extended period of time.

A current rule that will remain the same is allowing a spouse to rollover their deceased spouse’s IRA to a spousal IRA and take Required Minimum Distributions (RMDs) based on their life expectancy. Inherited IRA rules will be modified by the newly imposed rules affecting non- spousal beneficiaries such as children and grandchildren, the most common types of inherited IRA beneficiaries, who will need to take distributions on the entire balance within 10 years.

A challenge for inherited IRA beneficiaries is the tax implication of accelerated distributions over a much shorter time period. Some beneficiaries may also run the risk of falling into a higher tax bracket, especially if they are working.

Traditional IRAs

The 70 1/2 age limit for Traditional IRA contributions has been repealed, meaning that as long as you have earned income from working, you may contribute past age 70 1/2. The repeal is applicable to contributions made for tax year 2020 and thereafter, not for tax year 2019.

RMDs

The required minimum distribution (RMD) age for IRAs has been raised to 72 from 70 1/2. The new RMD age applies to those who turn 70 1/2 after December 31, 2019.

401(k) Plans

Small businesses are encouraged to set up plans for their employees by increasing the cap under which employees are automatically enrolled in a plan at 15% of wages. This provision is called a safe harbor.

Part-time employees who work either 1,000 hours annually or have three consecutive years with 500 hours of service are eligible for a 401(k) plan.

Annuities will now become an option for employees taking retirement distributions from their 401(k) plan, providing consistent income similar to how pension plans used to decades ago.

529 Plans

Qualified student loans may be repaid with 529 plan assets up to a maximum of $10,000 annually. Parents may also use 529 assets for the birth or adoption of a child, up to $5,000 per year.

Sources: https://waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/documents/SECURE%20Act%20section%20by%20section