Stock Indices:

| Dow Jones | 40,669 |

| S&P 500 | 5,569 |

| Nasdaq | 17,446 |

Bond Sector Yields:

| 2 Yr Treasury | 3.60% |

| 10 Yr Treasury | 4.17% |

| 10 Yr Municipal | 3.36% |

| High Yield | 7.69% |

YTD Market Returns:

| Dow Jones | -4.41% |

| S&P 500 | -5.31% |

| Nasdaq | -9.65% |

| MSCI-EAFE | 12.00% |

| MSCI-Europe | 15.70% |

| MSCI-Pacific | 5.80% |

| MSCI-Emg Mkt | 4.40% |

| US Agg Bond | 3.18% |

| US Corp Bond | 2.27% |

| US Gov’t Bond | 3.13% |

Commodity Prices:

| Gold | 3,298 |

| Silver | 32.78 |

| Oil (WTI) | 58.22 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 142.35 |

| Canadian /Dollar | 0.72 |

Macro Overview

Recent speculative trading among smaller retail investors raised concerns about how social media is influencing individual stock price movements. Popular social news aggregation and discussion websites are influencing frantic trading behavior, often by inexperienced traders, which is occasionally driving prices far above valuations that would be traditionally implied by traditional equity valuation methods. Some market participants and politicians are calling for heightened regulation and scrutiny surrounding these websites and how they operate.

Vaccine production and distribution is being closely monitored by market analysts and economists due to the tremendous impact it has on consumer behavior and sentiment. Consumer expenditures have been curtailed by stay-at-home mandates and risk of infections in public locations including retail stores and restaurants.

The Internal Revenue Service (IRS) will not accept 2020 tax returns until February 12 due to staffing shortages and COVID-related rules that were enacted in December 2020. Acceptance of prior year returns traditionally would have started two weeks sooner. Taxpayers owed a refund may see a delay in receiving funds, although the April 15 tax filing deadline will remain the same.

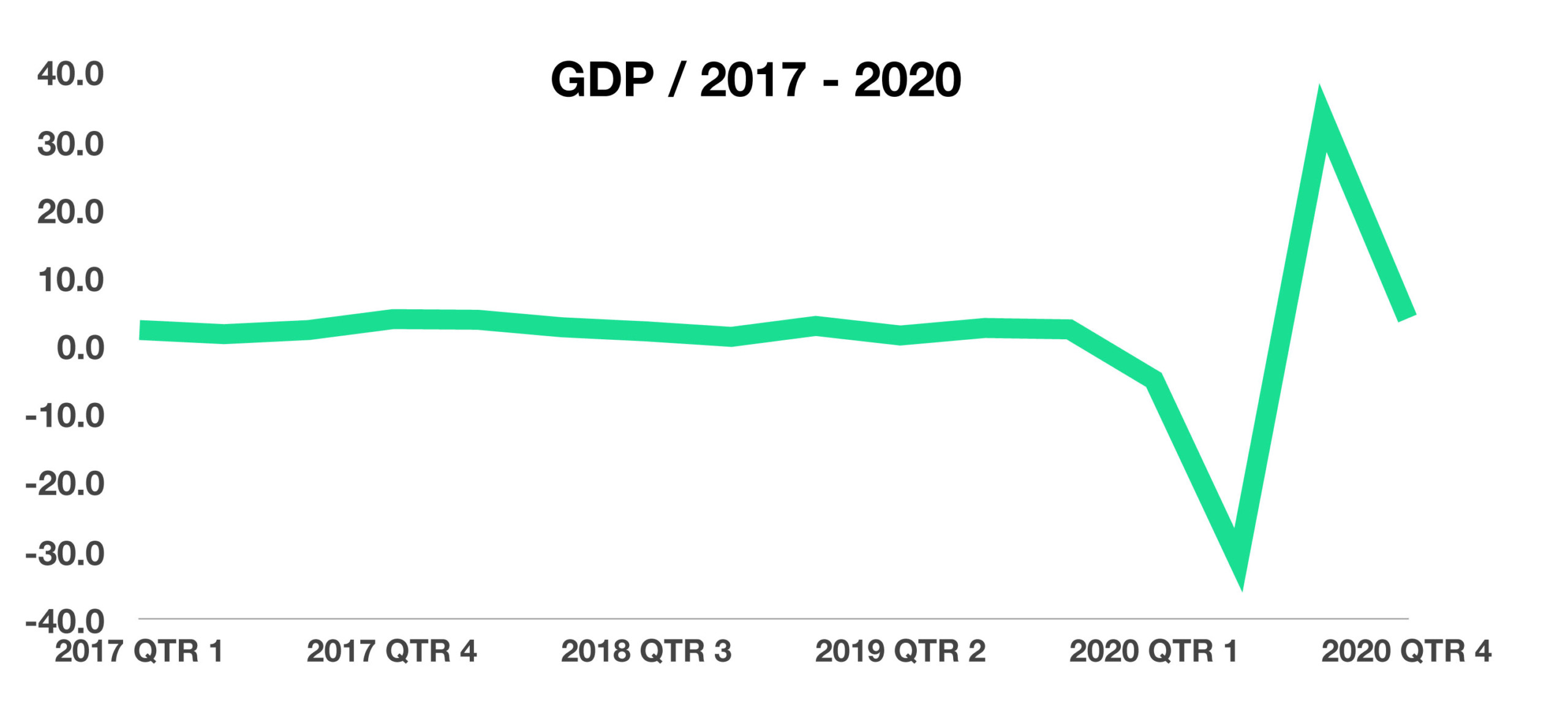

Economic growth for the U.S., as measured by Gross Domestic Product (GDP), rose at a rate of 4% in 2020, following a contraction of over 31% in the second quarter alone. The dramatic collapse and ensuing rebound for economic growth was historic in proportion.

Since COVID vaccine distributions began on December 14, 2020, more than 29.5 million doses have already been administered in the United States as of January 30, 2021. Total doses distributed but not yet administered stand at nearly 50 million as of the end of January. The federal government has primarily delegated prioritization and distribution of the doses to individual states. Some health care experts and economists are concerned that slow distribution of vaccinations worldwide will postpone sustainable economic resurgence.

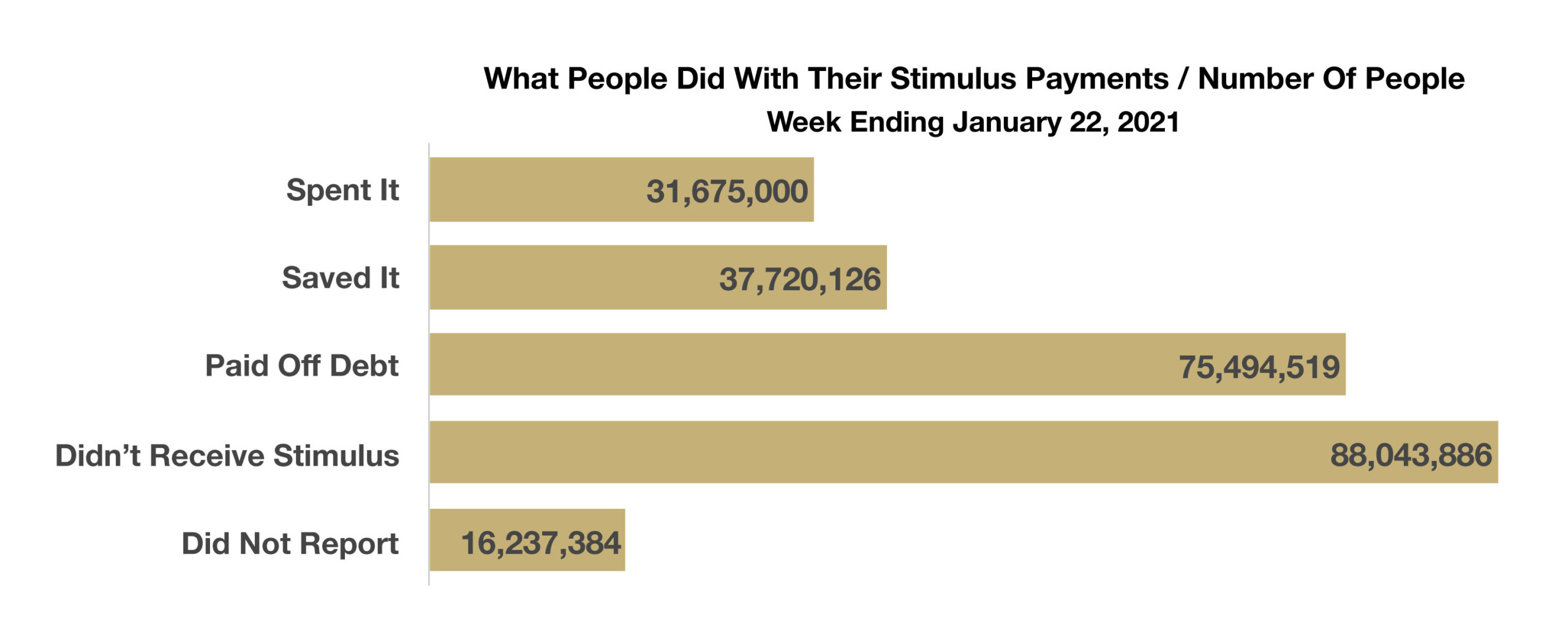

Data gathered by the U.S. Census Bureau as of January 22, 2021, reveal that millions of Americans are not spending their stimulus checks, but are rather saving the funds or paying off debt. With over 37.5 million people opting to save their stimulus payments, a growing number of policymakers believe that millions who are receiving stimulus checks may not actually need them.

Sources: Census Bureau, Rockefeller Foundation, CDC, Federal Reserve, IRS