Michael McCormick

5 West Mendenhall, Ste 202 | Bozeman, MT 59715

406.920.1682 mike@mccormickfinancialadvisors.com

Sustainable Income Planning | Investments | Retirement

Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Dear Friends,

Whew, 2022 is behind us! Looking back upon last year it seems that everyone suffered financially to some degree. Bonds and stocks were both down about -18%. An aggressive small cap tech portfolio got taken to the woodshed with losses over -40%. Utilities and commodities/energy were the only places to hide (other than cash). And once again, no one got it right. In hindsight, inflation was the culprit, finally showing up from all these years of free money. But we made it through. In fact, the unlikely “soft landing” scenario may be happening and I’m actually feeling optimistic about your investments.

Caveman with a cell phone running from a Sabretooth Tiger by Dall-e Artificial Intelligence

But any good news about unemployment and moderating inflation is already being drowned out by new threats. One such new terror I’ve been exploring is artificially intelligent programs that can write papers for students, provide relationship tips, and also give basic financial advice. It’s not something most of us can understand how it works, but it does! Does this stress you out? I asked ChatGPT How to reduce stress about money? This is what I received:

- Make a budget: Having a clear understanding of your income and expenses can help you feel more in control of your finances.

- Set financial goals: Setting specific, measurable, and achievable financial goals can give you a sense of purpose and direction.

- Create an emergency fund: Having a savings cushion can provide a sense of security and reduce stress caused by unexpected expenses.

- Seek professional advice: Consult with a financial advisor or therapist to help you understand and manage your stress about money.

- Practice mindfulness: Mindfulness can help you focus on the present moment and reduce stress caused by worries about the future or regrets about the past.

- Prioritize self-care: Make sure to take care of yourself physically, emotionally, and mentally. This can help reduce overall stress levels, including stress about money.

- Learn to manage stress: Stress management techniques, such as exercise, meditation, and deep breathing, can help you feel more relaxed and better able to manage stress about money.

It’s also important to remember that money is a means to an end, not an end in itself. Being content with what you have, and focusing on the things that really matter in life, such as relationships and personal fulfillment, can help reduce stress about money. (OpenAI.com)

Take care in 2023. I hope it’s the best ever! Why shouldn’t it be? -Mike

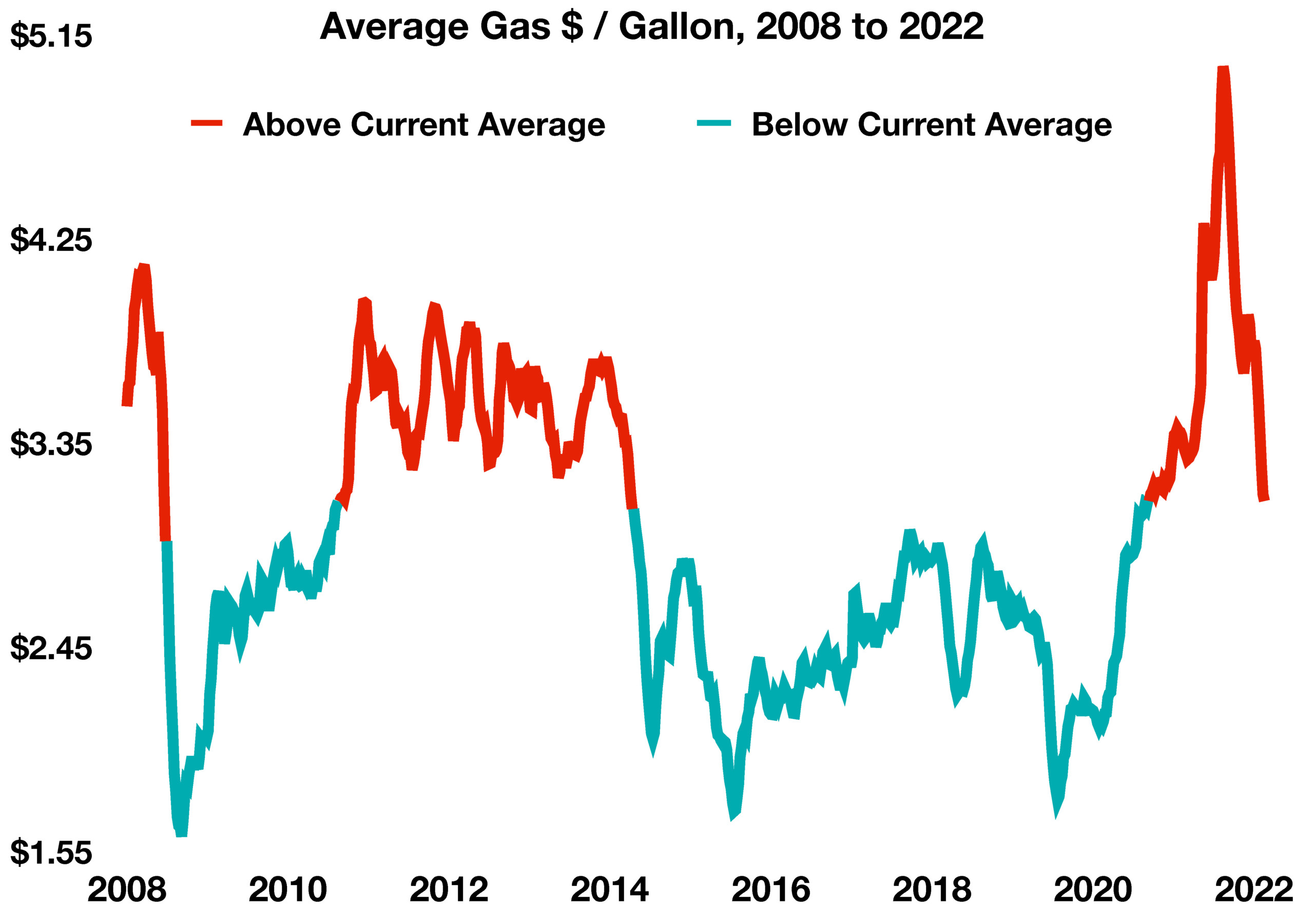

Average gasoline prices have officially reached an 18-month low after extraordinary prices in 2022. The average price per gallon of regular gasoline across the U.S. stood at $3.09 at the end of 2022, which was last seen over 18 months ago in June of 2021. In 2022, several international factors including supply limitations due to the war in Ukraine led to abnormally high fuel costs for consumers. The average price per gallon across the nation eclipsed $4 for 22 weeks in a row and surpassed $5 in June of 2022. Gasoline became a financial burden for many consumers throughout 2022, compounding already higher prices for other essential items. (Sources: U.S. Energy Information Administration, Federal Reserve Bank of St. Louis)

Average gasoline prices have officially reached an 18-month low after extraordinary prices in 2022. The average price per gallon of regular gasoline across the U.S. stood at $3.09 at the end of 2022, which was last seen over 18 months ago in June of 2021. In 2022, several international factors including supply limitations due to the war in Ukraine led to abnormally high fuel costs for consumers. The average price per gallon across the nation eclipsed $4 for 22 weeks in a row and surpassed $5 in June of 2022. Gasoline became a financial burden for many consumers throughout 2022, compounding already higher prices for other essential items. (Sources: U.S. Energy Information Administration, Federal Reserve Bank of St. Louis)