Markets shrugged off dismal economic data as local governments in geographic regions eased their COVID-related restrictions on local businesses. Following a recent surge in reported positive cases of the novel coronavirus, healthcare professionals expressed concern regarding a “second wave” of infections. The second quarter, which ended June 30th, saw a price rebound in all eleven sectors of the S&P 500 Index. This was a striking reversal following the first quarter of the year, in which equity prices plummeted.

The increase in reported new coronavirus cases in various states and cities has heightened anxiety among economic analysts. Fear of a second wave of infections has led to re-closures by some cities and businesses, inflicting further harm on already-struggling businesses. States and cities are employing a wide variety of different transmission prevention and re-opening strategies as they seek to balance health considerations with economic livelihood concerns. The World Health Organization (WHO) suggested that certain countries and regions reinstate mandatory stay-at-home rules in order to stem an acceleration of new infections. The WHO also noted that the United States and the world will eventually need to learn to live with virus outbreaks and the turmoil that accompanies them.

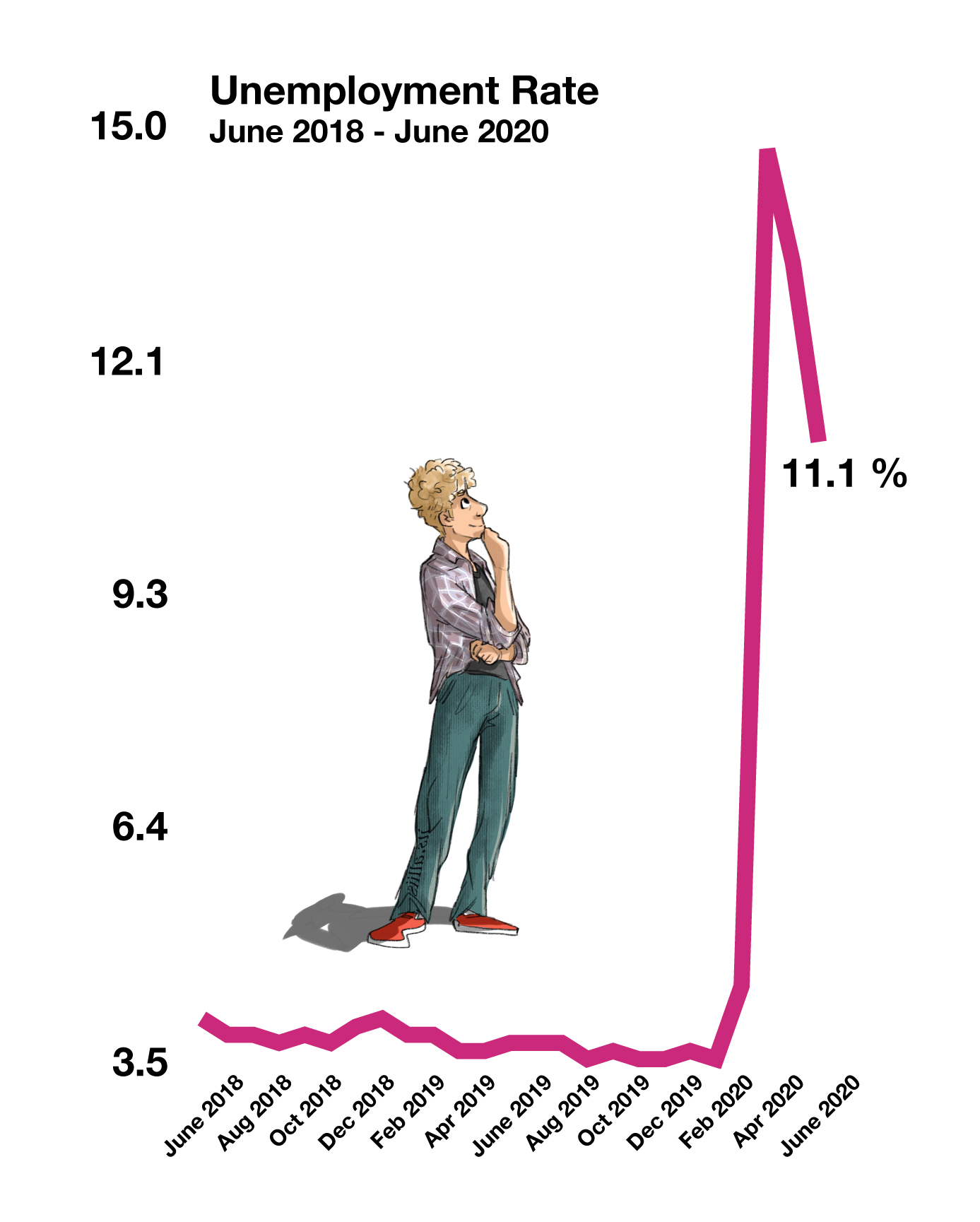

The Federal Reserve is placing safeguards in place to mitigate the debilitating impact that a second wave of infections could have on economic activity. The safeguards include two new lending programs to provide financial liquidity for cities and businesses across the country. The Municipal Liquidity Facility provides essential funds to cities and municipalities suffering from the financial fallout of the outbreak, and the Main Street Lending Program provides loans to small and mid-sized businesses. The Department of Labor acknowledged that it misclassified 4.9 million non-working people as newly employed for the month of May. The May employment data was initially questioned by economists and market analysts, yet propelled equity markets higher when released. Mischaracterizing data damages the credibility of data provided by the Labor Department and other government entities. June employment data revealed a decrease in the unemployment rate, driven by a resurgence in business activity for the restaurant, hospitality, and leisure sectors.

The European Union (EU) remained closed to U.S. travelers over the past month, despite opening borders to residents from some other countries in late June. In response to the steady increase of reported COVID-19 cases within U.S. borders, the EU extended the original July 1st end date for the travel ban, invoking epidemiological factors as the justification. The Congressional Budget Office (CBO) estimates that the virus outbreak will cost the U.S. economy $7.9 trillion over the next ten years. Cost estimates will be influenced by how the virus may evolve and when a vaccine will be introduced. (Sources: Federal Reserve, CBO, Dept. of the Treasury, CDC, Dept. of Labor, WHO)

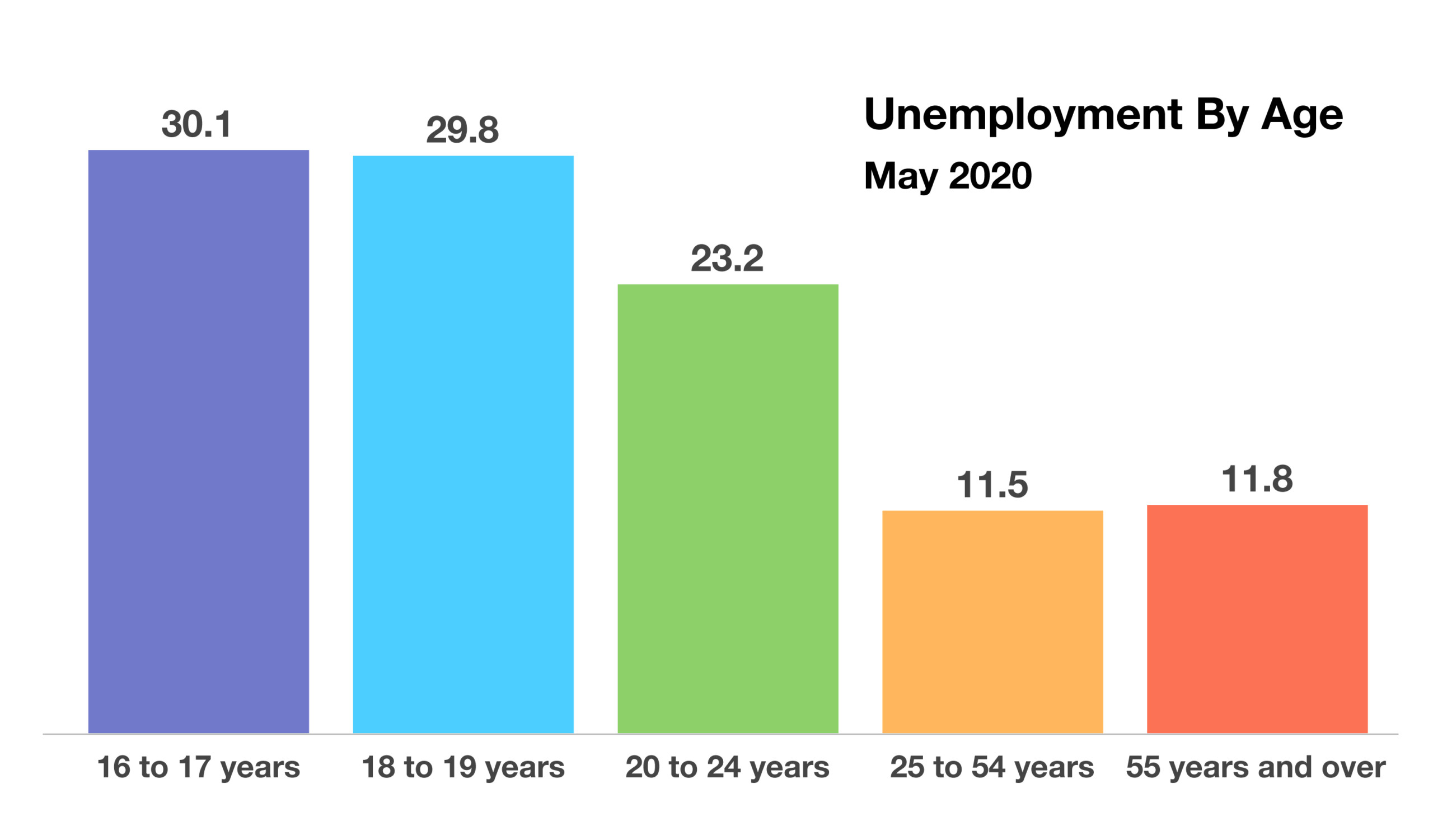

25% of workers ages 16 to 24 lost their jobs from February to May

Equities rebounded in the second quarter, with all eleven sectors of the S&P 500 Index positive for the quarter. Sectors with the most advancements included consumer discretionary, energy, materials, and technology. Economists and analysts believe that the upswing in these sectors is representative of an anticipated economic recovery, but that risk remains due to the potential for a second outbreak wave.

The technology-heavy Nasdaq Index outperformed the S&P 500 Index and the Dow Jones Industrial Index both year-to-date and over the second quarter. Some stock analysts have proposed that the disparity in performance is reminiscent of the dot-com expansion 20 years ago. (Sources: S&P, Nasdaq, Dow Jones, Bloomberg)

Rates Stabilize In June – Fixed Income Overview

Federal Reserve continued purchasing debt securities in the second quarter under the Secondary Market Corporate Credit Facility program, which the Fed established to maintain liquidity in the bond markets. Individual corporate bonds and exchange-traded funds (ETFs) have been included in the Fed’s buying program, which was launched in mid-June. Bonds purchased include debt with both investment grade and non-investment grade ratings.

Corporate and government bonds posted positive returns in the second quarter, as yields leveled off following the dramatic drop in yields during the first quarter of the year. The benchmark 10-year Treasury bond yield closed at 0.66% at the end of June, helping to stabilize consumer lending and mortgage rates. (Sources: Dept. of the Treasury, Federal Reserve, Bloomberg)

Unemployment Hits Young Workers Hardest – Labor Market Overview

Unemployment hit young workers the hardest, with roughly 25% of workers ages 16 to 24 losing their jobs from February to May. Sectors that traditionally employ mostly younger workers, such as leisure, hospitality, and restaurants, have suffered dramatic declines in business activity since the outbreak. Economic conditions caused by the pandemic and the corresponding governmental measures have introduced a challenging environment for high school and college students, as well as college graduates, to find short-term and summer job positions.

Younger workers 16-19 years of age are experiencing unemployment rates as high as 30%, more than double the rate at this time last year. Teenagers are seeing nearly triple the amount of unemployed compared to all other age groups nationally, and the overall unemployment rate is at 11.1% as of the most recent data reported by the Department of Labor. (Source: Dept. of Labor)

Unlike PPP loans, Main Street loans are not grants and can’t be forgiven

Fed Main Street Loan Program – Stimulus Program Overview

In addition to the stimulus loan programs brought about by the CARES Act, the Federal Reserve introduced its own stimulus program called the Main Street Loan Program.

The program is designed to help credit flow to small and medium-sized businesses that were in sound financial condition before the onset of COVID-19, and are recovering from, or adapting to, the impacts of the pandemic. The program offers 5-year loans with floating rates and deferred principal and interest payments to assist businesses facing temporary cash flow interruptions. Loans range in size from $250,000 to $300 million, offering a wide range supporting a broad set of business entities. Different from Paycheck Protection Program (PPP) loans, Main Street Program loans are not grants and cannot be forgiven.

The Fed is participating in the lending process by taking a 95% interest in the loans issued, while lenders retain 5% of the loans. The unusual tactic of taking an interest in the loans allows the Fed to assume risk in the loans issued. Businesses can learn about eligibility requirements for a Main Street Program loan by accessing the Fed’s link at https://www.federalreserve.gov/monetarypolicy/mainstreetlending.htm. (Source: Federal Reserve Bank of Boston)

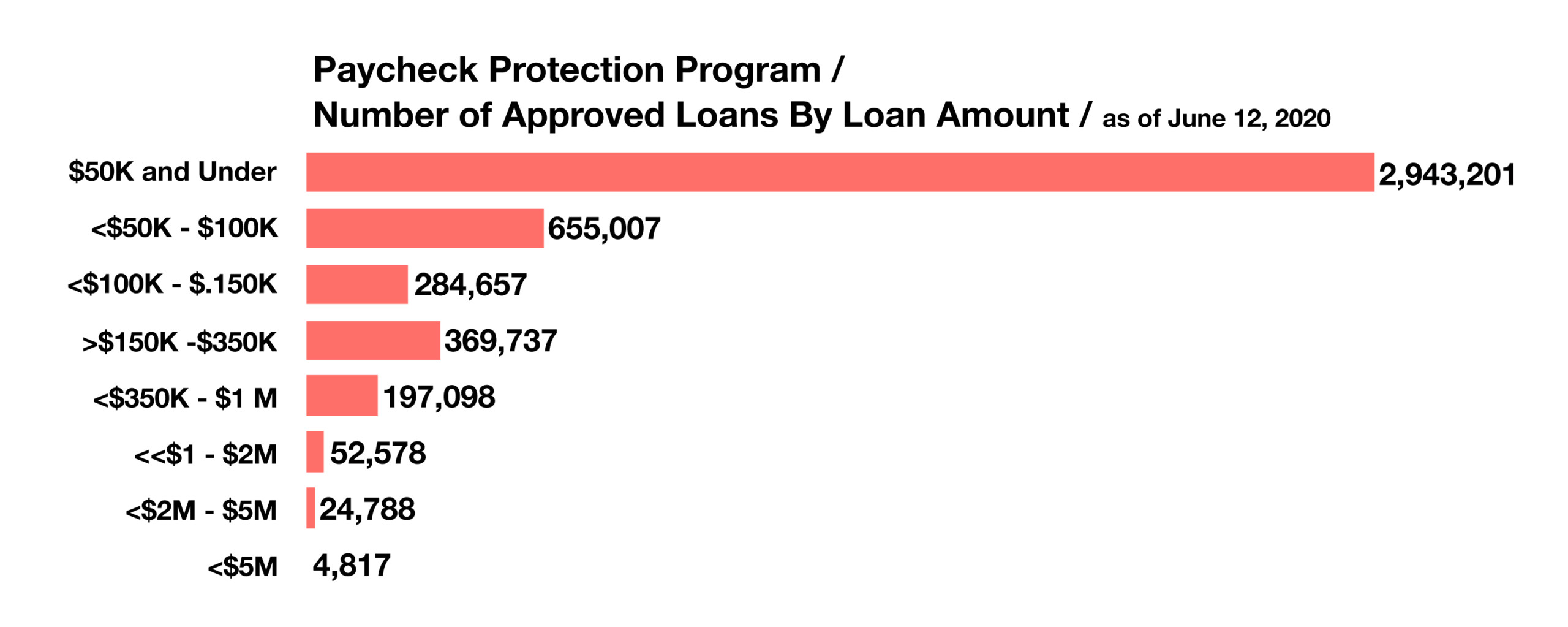

Small Business Loan Program Still Has Funds – Stimulus Program Review

Three months following the administration’s launch of pandemic relief programs, the remaining balance of undirected funds in conjunction with the Paycheck Protection Program (PPP) has been subject to scrutiny. The program was established to assist small businesses with critical funds to remain solvent during the pandemic.

Congressional members are considering a proposal to forgive loans of $150,000 or less, which represent nearly 85% of all PPP loans, in order to minimize financial burden for small businesses.

Following the Small Business Administration’s approval of additional loans, the program’s outlays are now the largest financial expense related to governmental COVID-19 spending. Loans have been approved for nearly 81% of PPP loan applicants, many of whom have already received the funds.

The application deadline for the Paycheck Protection Program was extended June 30 to August 8. As of June 12, 2020, the SBA reported that over 4.5 million PPP loans had been approved, with an average loan amount of $113,000. (Sources: SBA, congress.gov, NFIB)

IRAs and 401(k)s are allowed to have withdrawals up to $100,000

Tapping 401k & Retirement Plan Assets During The Crisis – Retirement Planning

Provisions in the CARES Act allow for the withdrawal of retirement plan assets with waived penalties and minimized tax liabilities. During the current tax year, retirement account owners are permitted to withdraw funds from 401k plans, tax-deferred plans, and IRAs without incurring penalties. Loan limitations on employer-sponsored 401k plans will be relaxed, allowing employees to take larger loan amounts. Required Minimum Distributions (RMDs) are also being waived for 2020 distributions.

Section 2202 under the CARES Act enacted on March 27, 2020, provides for special distribution options and rollover rules for retirement plans and IRAs. Under the revised rules, IRA owners and retirement plan participants are allowed to withdraw up to $100,000, but must meet certain criteria to qualify. The IRS notes the following as criteria to meet:

“You are diagnosed with the coronavirus (COVID-19); Your spouse is diagnosed with the coronavirus (COVID-19); You experience adverse financial consequences as a result of being quarantined, furloughed, laid off, or having reduced work hours all due to COVID-19; Unable to work due to a lack of child care as result of COVID-19; Experience adverse financial consequences as a result of closing a business or loss of hours as a result of COVID-19.”

Distributions from IRAs and qualified plans will have the 10% penalty waived but are still taxed at the individual owner’s corresponding tax rate. Qualified distributions up to the $100,000 maximum may be taken between January 1, 2020 and December 30, 2020. Taxes on distributions may be paid over a three-year period starting with the year in which the initial distribution was made. Distributions may also be repaid back to an IRA or qualified plan over a three-year period to avoid any tax consequences. (Source: https://www.irs.gov/newsroom/coronavirus-related-relief-for-retirement-plans-and-iras-questions-and-answers)

In an effort to help keep homeowners and renters in their homes in the midst of financial burden due to the pandemic, the federal government has extended moratoriums on foreclosures and evictions to August 31, 2020 from the original expiration date of June 30. These moratoriums apply to single family mortgages insured by the Federal Housing Administration (FHA) and the U.S. Department of Housing & Urban Development (HUD). Under the moratorium, lenders of unpaid mortgages are required to halt foreclosure actions and suspend any foreclosure proceedings that were in process. The moratorium also forbids evictions of renters.

Homeowners are advised to continue making mortgage payments during the moratorium period. If this is not possible, then homeowners may seek forbearance on the payments via a provision in the CARES Act. Homeowners affected by the coronavirus pandemic with a federally-backed loan can delay or reduce mortgage payments for up to a year. Homeowners that don’t have a government-backed loan may obtain forbearance at the discretion of their mortgage lender. (Sources: Fannie Mae, Freddie Mac, HUD)

Economic conditions caused by the pandemic and the corresponding governmental measures have introduced a challenging environment for high school and college students, as well as college graduates, to find short-term and summer job positions.

Economic conditions caused by the pandemic and the corresponding governmental measures have introduced a challenging environment for high school and college students, as well as college graduates, to find short-term and summer job positions.