Three Big Changes Our Government is now debating CARES Act 2, providing stimulus for the economic impact of COVID19. Regardless of cost and politics involved (not to mention how it is impacting our economy), there are provisions from Act 1 that benefit many of my Clients.

1) Required Minimum Distributions (RMD)s are being waived for 2020 distributions. As background, the SECURE ACT of 2019 (before COVID19) had changed the RMD start date from age 70 1/2 to 72. If you had started RMDs at 70 1/2 or 72, and took your annual distribution between 2/1 and 5/15/2020, you can return it to your account! Normally, qualified plan and IRA distributions require re-contributions within 60 days, but under CARES, you have the remainder of this year. Those who took their RMD in January can return it by August 31. These RMDs are not being delayed, but rather waived. In the event that you had taxes withheld from your distribution, you may re-contribute the full amount, with tax amounts coming from your personal funds Then you can reduce your future withholdings until you are repaid.

Many retirees who turn 70 1/2 in 2021 took an RMD in calendar year 2020 in order to avoid 2 payments in one year (2021). Now they can repay that distribution and wait to begin distributions at age 72.

2) Section 2202 under the CAREs Act enacted on March 27, 2020, provides for special distribution options and rollover rules for retirement plans and IRAs. Under the revised rules, IRA owners and retirement plan participants are allowed to withdraw up to $100,000, but must meet certain criteria to qualify. The IRS notes the following as criteria to meet: You are diagnosed with the coronavirus (COVID-19); Your spouse is diagnosed with the coronavirus (COVID-19); You experience adverse financial consequences as a result of being quarantined, furloughed, laid off, or having reduced work hours all due to COVID-19; Unable to work due to a lack of child care as result of COVID-19; Experience adverse financial consequences as a result of closing a business or loss of hours as a result of COVID-19. 3) Distributions from IRAs and qualified plans will have the 10% penalty waived but are still taxed at the individual owner’s corresponding tax rate. Qualified distributions up to the $100,000 maximum are for distributions made between January 1, 2020 and December 30, 2020. Taxes on distributions may be paid over a three year period starting with the year in which the initial distribution was made. Distributions may also be repaid back to an IRA or qualified plan over a three year period to avoid any tax consequences. (Source: https://www.irs.gov/newsroom/coronavirus-related-relief-for-retirement-plans-and-iras-questions-and-answers)

If you would like assistance with re-contributions or penalty-free withdrawals, just call us and we will be happy to assist.

What is your WHY?

What is your “WHY”? Today we’re dealing with a health crisis, political unrest and volatile markets. All this seems like something new, but we’ve been here before and will be again. Stuck at home and looking for entertainment, my husband and I have started binging tv shows from the 80s and 2000s. Boston Legal is one of our favorites! Almost daily, we are amazed that these shows are about the same political issues and ongoing debates over cultural norms that challenge us today.

We debate because we’re passionate. We’re passionate about our values.

A recent study from the Money Management Institute, Aon, shows there is a gap between what Clients want and what Financial Advisors THINK they want.

To paraphrase their findings…76% of Clients want to incorporate at least one of their core values into their investment portfolio but only 44% of Advisors realize it. Also, Clients are far more satisfied with the financial advisory relationship when they feel their values are being reflected.

This is my purpose…It is WHY I do – What I do – and how I do it. It doesn’t necessarily start out that way. When I first ask Clients how I can help them, most say they just want their money to grow – and I can do that! But over time it is natural that our Client-Advisor relationship, their financial plan or their investments DO reflect their values.

One example where their values can be reflected through our relationship would be a couple, where only one spouse had ever managed the finances and investments. He may not need my help to make their money grow, but more than one couple has approached me over the years so that we would have a strong relationship when it was needed, to be there for the other spouse in the event the first could no longer manage the finances. That’s not really about money. It’s about the Clients’ values and it’s about relationship.

Many of my Clients’ value family first. They work with me because I free their time for those they love. They are comfortable having me work FOR them, and not just WITH them. They have granted me discretion to make and act on decisions within agreed-upon parameters – to give them more valuable time to take care of loved ones, to travel, and play. They count on me to provide organization and management so they can accomplish life’s goals with less worry.

And it’s becoming more possible all the time, to choose investments that reflect a person’s values and even further a cause. Before Covid, I attended the 2020 Catholic Foundation Investment Forum of North Georgia…and I’m not Catholic. It’s my job – my purpose – to help Clients define and reach THEIR goals. Some of my Clients are Catholic and would like to invest in companies that further Catholic causes. Others are more concerned about personal liberty or environmental issues.

We can invest to achieve growth, income, and philanthropy in ways that are relevant to your goals and consistent with your values.

The Covid Economy

Macro Overview

Concern has elevated regarding the possibility of a second wave of COVID-19 infections following a surge in cases across the country. Markets, however, continued to shrug off dismal economic data amid pandemic worries, as a sporadic easing of restrictions targeting businesses came about. The second quarter, which ended June 30th, saw a rebound in all eleven sectors of the S&P 500 Index, a reversal following the first quarter of the year.

The increase in new coronavirus cases in various states and cities has escalated anxiety among investors and market analysts. Fear of a second wave of infections has led to re-closures by some cities and businesses, inflicting further harm on already struggling businesses. The variance of methods being utilized by states and cities continues to be vastly inconsistent.

The World Health Organization (WHO) suggested that certain countries and regions reinstate lockdowns in order to stem an acceleration of the pandemic. The WHO also believes that the United States and the world will eventually need to learn to live with virus outbreaks and the turmoil that accompanies them.

The Federal Reserve is placing safeguards in place, should a second wave of infections emerge which could further debilitate economic activity. The safeguards include two newly created lending programs to facilitate liquidity for cities and businesses across the country. The Municipal Liquidity Facility provides essential funds to cities and municipalities suffering from the financial fallout of the outbreak, and the Main Street Lending Program provides loans to small and mid-sized businesses.

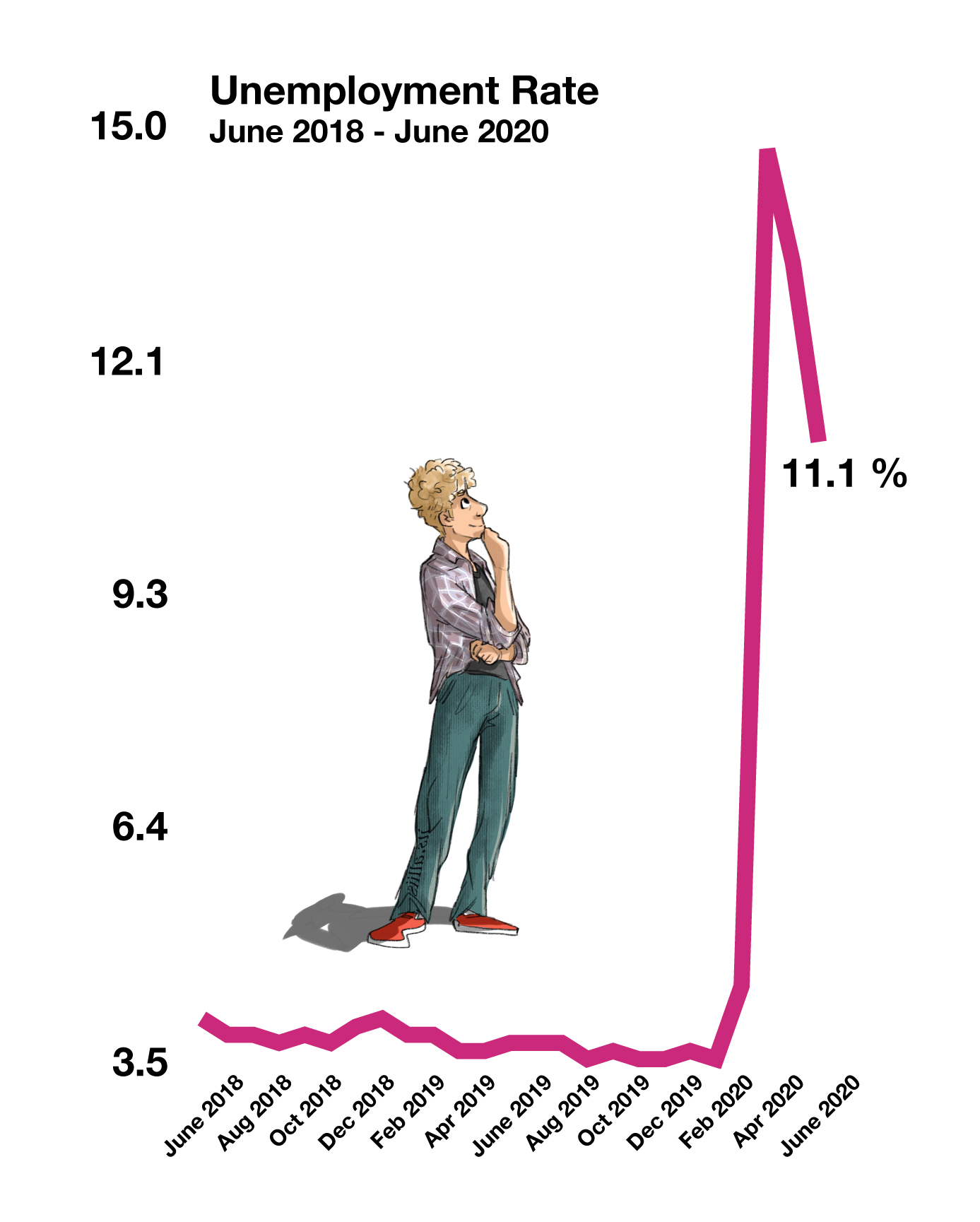

The Department of Labor acknowledged that it misclassified 4.9 million non working people as newly employed for the month of May. The May employment data was initially questioned by economists and market analysts, yet propelled equity markets when released. Such data mishaps can place Labor Department data as well as data from other government entities into question. June employment data revealed a decrease in the unemployment rate, propelled by a resurgence in restaurant, hospitality, and leisure jobs.

The European Union (EU) remained closed to U.S. travelers this past month despite borders opening up to residents from other countries as of late June. In response to the steady increase of reported COVID-19 cases within U.S. borders, the EU extended the original July 1st travel ban suspension noting epidemiological factors as the justification.

The Congressional Budget Office (CBO) estimates that the virus outbreak will cost the U.S. economy $7.9 trillion over the next ten years. The uncertainty of how the virus may evolve and when a vaccine is introduced will alter cost estimates. (Sources: Fed, CBO, U.S. Treasury, CDC, Labor Department, WHO)

Equities rebounded in the second quarter, with all eleven sectors of the S&P 500 Index positive for the quarter. Sectors with the most advancements included consumer discretionary, energy, materials and technology. Economists and analysts believe that the upswing in these sectors is representative of an economic recovery, yet hinged on the risk of a second outbreak wave.

The technology heavy Nasdaq Index has outperformed the S&P 500 and the Dow Jones Industrial Index both year to date and for the second quarter. Some stock analysts believe that the disparity in performance is reminiscent of the dot-com expansion 20 years ago. (Sources: S&P, Nasdaq, Dow Jones, Bloomberg)

Rates Stabilize In June – Fixed Income Overview

Federal Reserve buying of debt securities continued in the second quarter under the Secondary Market Corporate Credit Facility program, which was established to maintain liquidity in the bond markets. Individual corporate bonds and ETFs have been part of the Fed’s buying program, which was launched in mid-June. Bonds purchased so far include debt issues from both investment grade and non-investment grade rated companies.

Corporate and government bonds continued to post positive returns in the second quarter, as yields stabilized following the dramatic drop in yields during the first quarter of the year. The benchmark 10-year Treasury bond yield closed at 0.66% at the end of June, helping to boost consumer lending and mortgage rates. (Sources: Treasury Dept., Federal Reserve, Bloomberg)