Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Macro Overview

Financial markets are becoming more sensitive to the Delta variant mutation of Covid-19, as some countries in Europe reconsider easing restrictions on businesses and travel. Regardless, global equities finished the 2nd quarter on a positive note and rates stabilized following an upward trending environment earlier in the year.

A lack of spending and stay home orders during the pandemic has left millions of consumers with abundant cash hoards, which has been a factor in the recent economic activity occurring nationwide. Some economists and analysts question as to how long it will be until the plentiful cash positions are depleted.

Comments by St. Louis Federal Reserve Bank member James Bullard suggested that there is a “housing froth that seems to be developing” and indicated a pullback on mortgage bond purchases by the Federal Reserve could happen in 2022.

Half of existing home buyers in April that took a mortgage out put 20% down, while a quarter of buyers paid cash according to the National Association of Realtors. Cash offers as well as large down payments are pushing some less capable buyers out of the market, consequently forcing many to rent until conditions change.

There is growing concern that the more infectious Delta variant of Covid-19 may evolve into a dominant strain in the U.S. The highly transmissible variant made up 30% of positive samples sequenced in the U.S. for the two-week period ending June 19th according to the U.S. Centers for Disease Control and Prevention. The Delta mutation first emerged in India and has since been spreading worldwide, forcing some countries to reevaluate loosened restrictions on businesses, travel and public events.

An eviction moratorium for tenants set to expire on June 30th was extended to July 31st after a Supreme Court decision. The moratorium was initiated in August by the prior administration to help tenants that were experiencing financial hardships due to Covid-19. Some landlords across the country have consequently seen months of non-payment by some tenants with the inability to evict them. The U.S. Department of Agriculture also extended through July 31st a moratorium on foreclosures from properties financed by USDA Single Family Housing Direct and guaranteed federal loans.

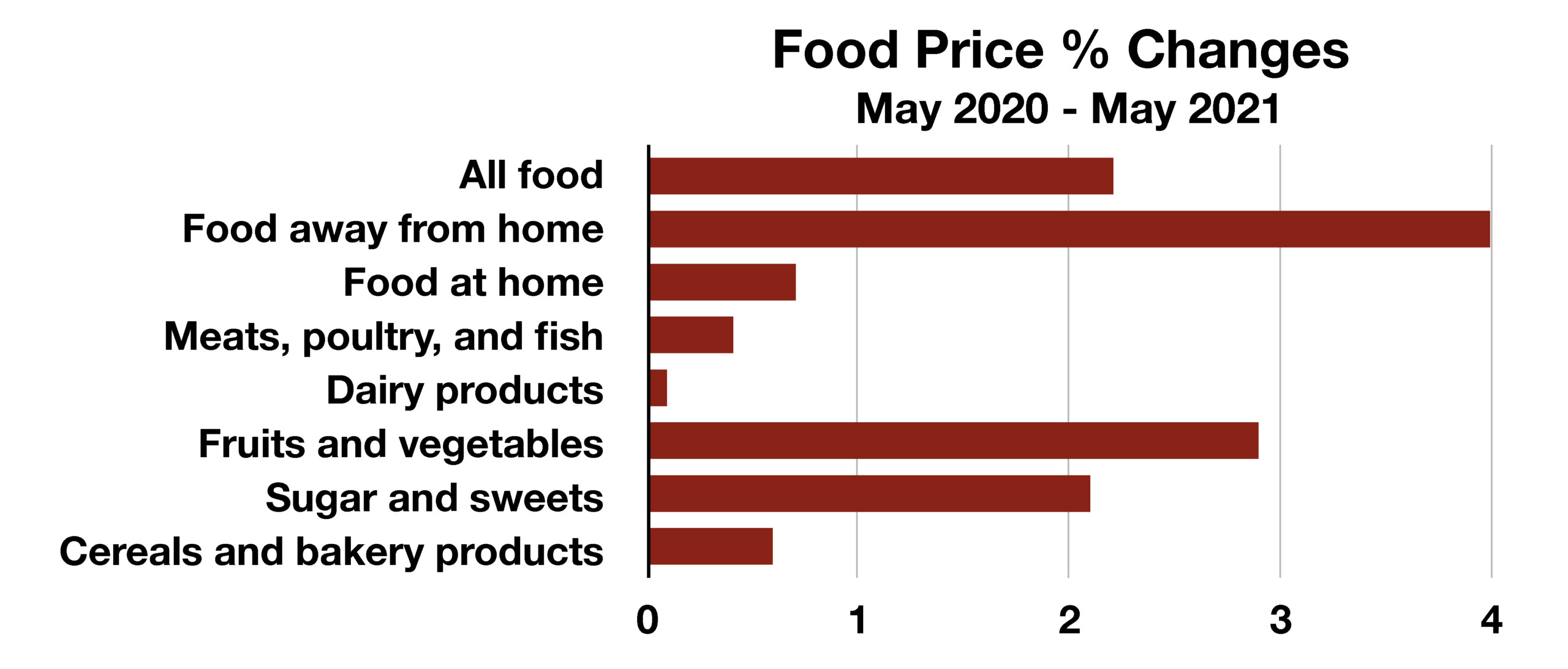

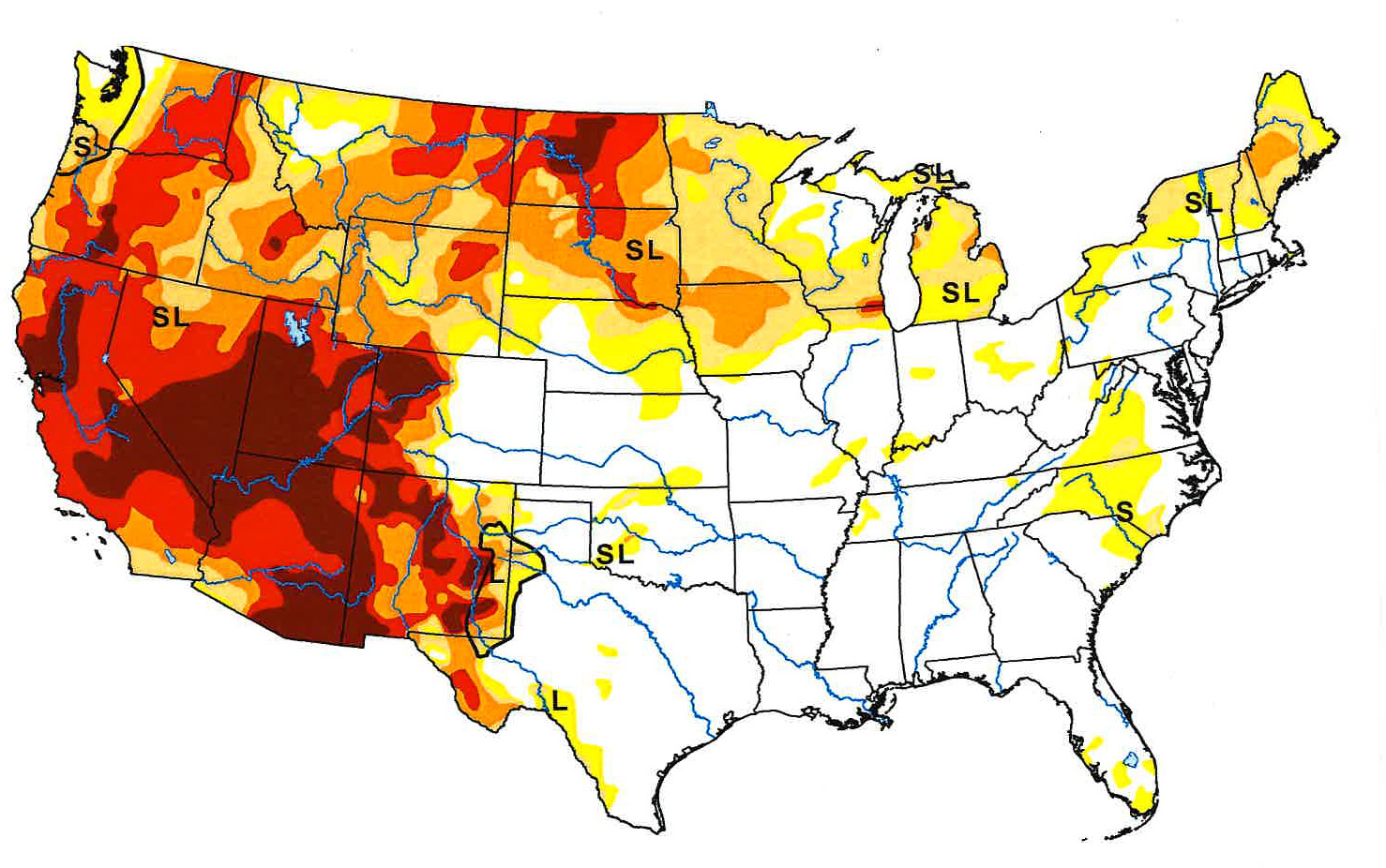

The U.S. Drought Monitor shows that nearly ten percent of the United States is experiencing exceptional drought characteristics as of June 30th. Severe drought conditions are primarily inflicting the western states even as excessive rains pound other parts of the country. Food crops such as wheat, corn and grains are expected to be affected, pushing prices higher in an already inflationary environment. (Sources: Labor Dept., U.S. Drought Monitor, NAR, USDA, Fed, CDC)