Earl R. King Sr., CFP®

Managing Member

9701 Apollo Drive, Suite 410

Largo, MD 20774

Tel: 301-304-6070/Cell: 240-472-6570

eking@erogerfinancial.com / www.erogerfinancial.com

Stock Indices:

| Dow Jones | 40,669 |

| S&P 500 | 5,569 |

| Nasdaq | 17,446 |

Bond Sector Yields:

| 2 Yr Treasury | 3.60% |

| 10 Yr Treasury | 4.17% |

| 10 Yr Municipal | 3.36% |

| High Yield | 7.69% |

YTD Market Returns:

| Dow Jones | -4.41% |

| S&P 500 | -5.31% |

| Nasdaq | -9.65% |

| MSCI-EAFE | 12.00% |

| MSCI-Europe | 15.70% |

| MSCI-Pacific | 5.80% |

| MSCI-Emg Mkt | 4.40% |

| US Agg Bond | 3.18% |

| US Corp Bond | 2.27% |

| US Gov’t Bond | 3.13% |

Commodity Prices:

| Gold | 3,298 |

| Silver | 32.78 |

| Oil (WTI) | 58.22 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 142.35 |

| Canadian /Dollar | 0.72 |

Macro Overview

A resurgence of sporadic economic activity emerged in May as stay at home bans were eased and some businesses slowly reopened. Virus resurgence fears are still a concern as uncertainty surrounding the availability of a vaccine lingers.

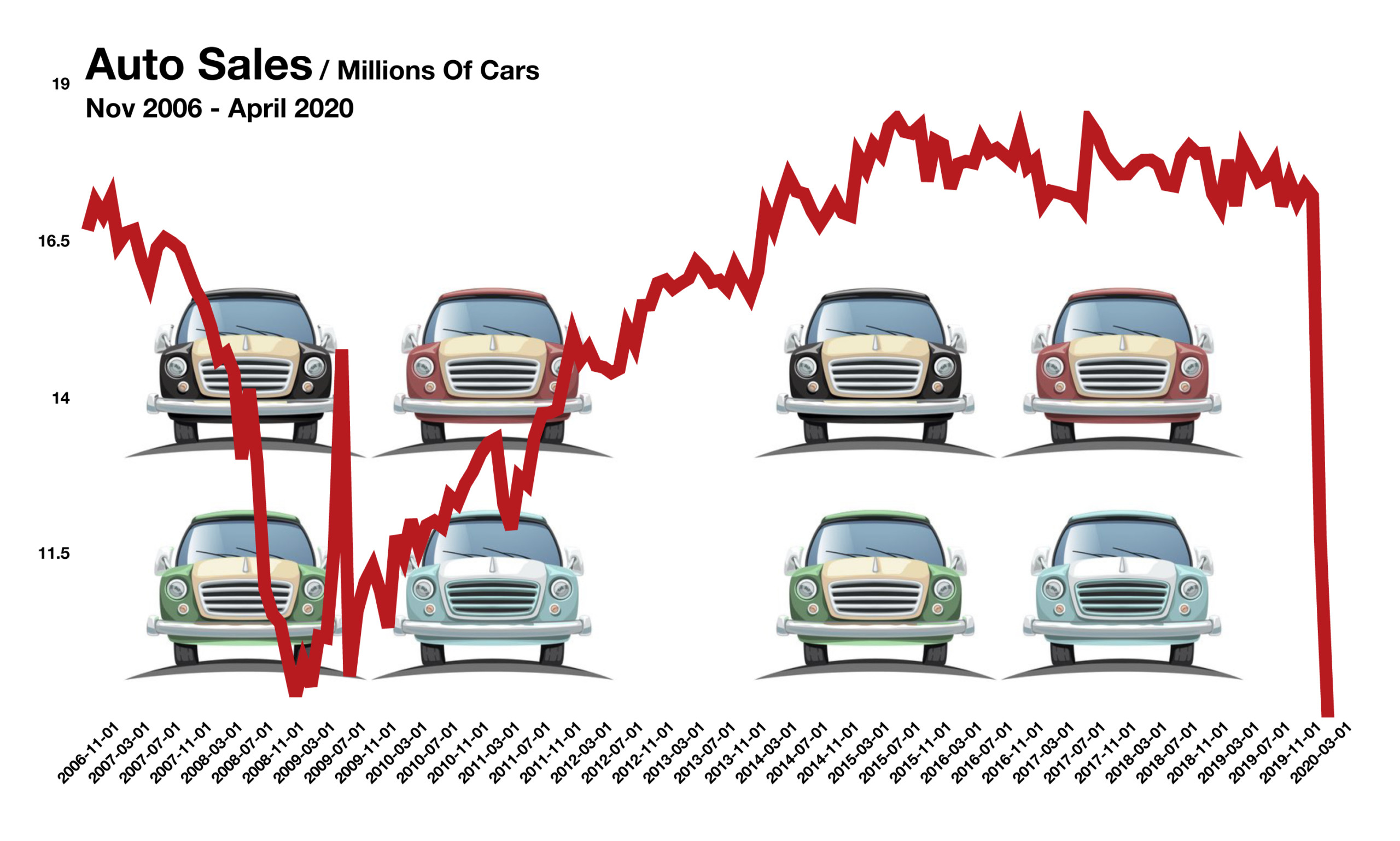

Following April’s rebound for U.S. equities, May continued to post recaptured gains for all major stock indices. Slow re-openings by states and cities have allowed a gradual reactivation of economic activity benefiting nearly all sectors of the equity markets.

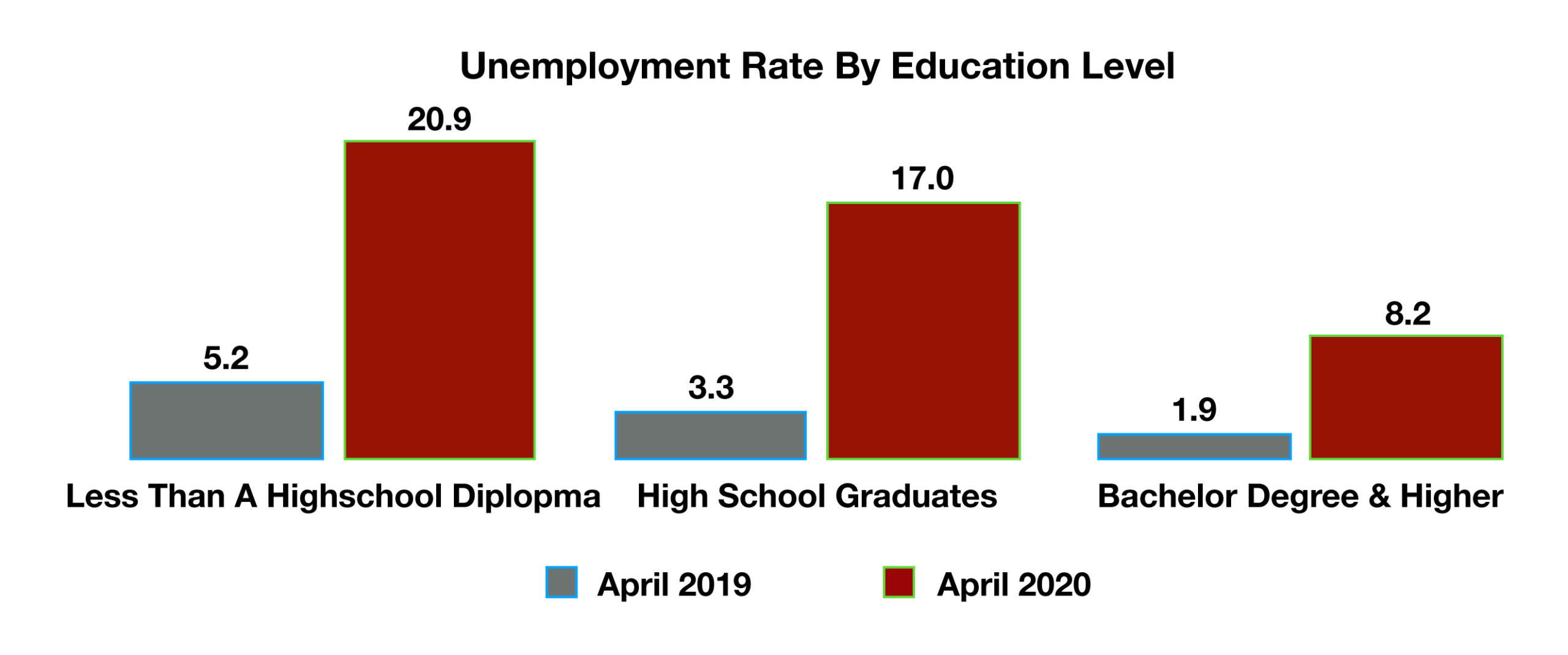

Unemployment hit 14.7%, the highest since the great depression era, when unemployment was 25%. All income and education levels were profoundly affected, with over 40 million applying for unemployment claims since the middle of March. The extent of the lock down for businesses nationwide is being blamed for a vast amount of small business bankruptcies that may prohibit the re-hiring of millions of workers in numerous industries.

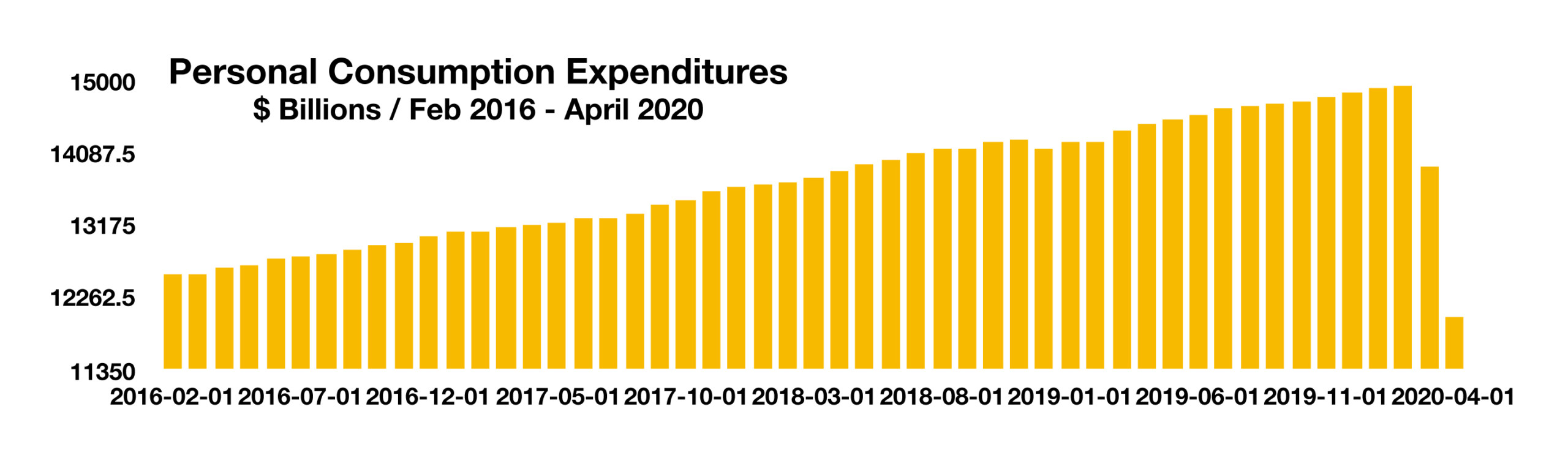

Retail sales in April saw their largest decline on record, the result of mandatory store closings and stay at home requirements. Industrial and manufacturing activity also fell in April, an indicator of a slower economic environment. Economic damage may not be fully recognized for months as lagging data tracked by various government agencies trickle into the headlines and financial markets. Consumer confidence, as measured by the University of Michigan CC Index, improved in May as consumers sought hope from the gradual easing of the virus quarantine. Inflation expectations also increased as scarce goods demanded higher prices across the country.

Economists and analysts are curious as to how the millions of unemployed workers will sustain themselves when their unemployment benefits expire. The $600 weekly unemployment benefit provided by the federal government expires on July 31st, unless extended by Congress. Individual state benefits vary on maximum weekly amounts, duration, and extension qualifications.

A study compiled by the Chicago Federal Reserve revealed that consumers spent nearly half of their federal stimulus checks within two weeks, then reverting to their prior spending habits. Economists expect that the economic effects of the one-time payments will be short lived.

Congress is expected to extend the period of time allotted for small businesses to use funds provided by the Paycheck Protection Program (PPP) from 8 weeks to 24 weeks. The additional time allows businesses to apply funds to approved expenses including payroll, rent, and utilities.

Federal unemployment benefits skyrocketed to $430 billion in April, the single largest monthly increase ever. Monthly unemployment benefits had been averaging $29.5 billion per month over the last five years, prior to the initial payout in benefits starting in March 2020 following the virus outbreak.

Sources: Federal Reserve, Dept. of Labor, Commerce Dept., Bloomberg

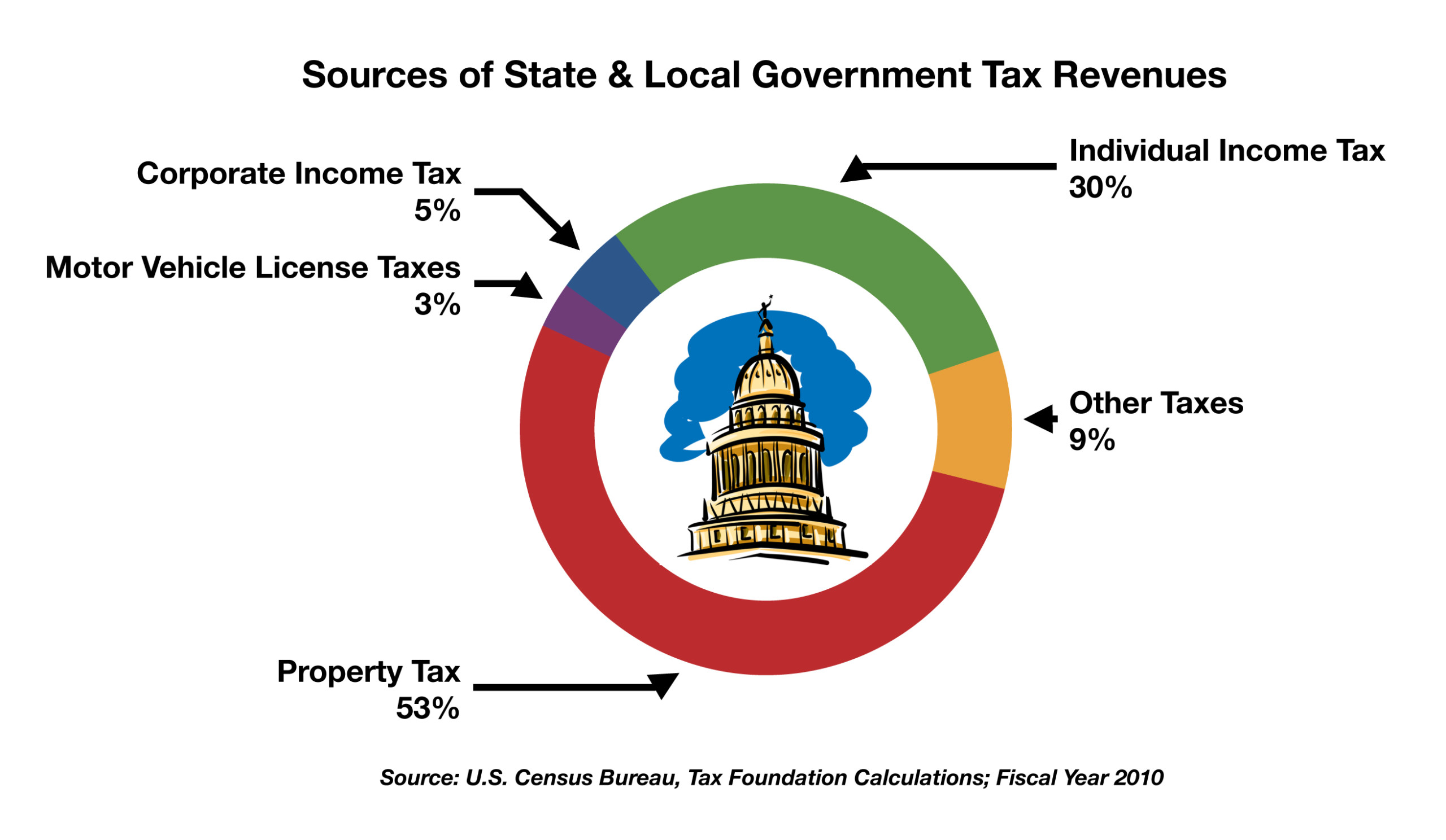

The dramatic loss of jobs has also led to mortgages and property taxes not being paid as homeowners struggle to meet ends. Data collected by the U.S. Census Bureau and the Tax Foundation identify that over 50 percent of state and local government revenues have come from property taxes over the past decade. Individual income taxes are significant, representing 30% of tax revenues while corporate income taxes make up roughly 5%. That’s why the dramatic increase in unemployment is so critical to state and local economies. (Sources: U.S. Census Bureau, The Tax Foundation)

The dramatic loss of jobs has also led to mortgages and property taxes not being paid as homeowners struggle to meet ends. Data collected by the U.S. Census Bureau and the Tax Foundation identify that over 50 percent of state and local government revenues have come from property taxes over the past decade. Individual income taxes are significant, representing 30% of tax revenues while corporate income taxes make up roughly 5%. That’s why the dramatic increase in unemployment is so critical to state and local economies. (Sources: U.S. Census Bureau, The Tax Foundation)

So for those who have not received a stimulus check or direct deposit yet, a debt card may be on its way. The debit cards are being issued by MetaBank, which is the Treasury Department’s financial agent, and mailed in plain white envelopes from Money Network Cardholder Services. The card is known as an Economic Impact Payment Card (EIP). The problem is that the envelope and the card may appear illicit and fraudulent to recipients, who are already wary about what they receive in the mail. The IRS notes that if you’ve received a card and are still not certain if it is a legitimate EIP card, you can visit EIPcard.com. (Source: IRS.gov/corornavirus/economic-impact-payment)

So for those who have not received a stimulus check or direct deposit yet, a debt card may be on its way. The debit cards are being issued by MetaBank, which is the Treasury Department’s financial agent, and mailed in plain white envelopes from Money Network Cardholder Services. The card is known as an Economic Impact Payment Card (EIP). The problem is that the envelope and the card may appear illicit and fraudulent to recipients, who are already wary about what they receive in the mail. The IRS notes that if you’ve received a card and are still not certain if it is a legitimate EIP card, you can visit EIPcard.com. (Source: IRS.gov/corornavirus/economic-impact-payment)