Derek J. Sinani

Founder/Managing Partner

derek@ironwoodwealth.com

7047 E. Greenway Parkway, Ste. 250

Scottsdale, AZ 85254

480.473.3455

Stock Indices:

| Dow Jones | 44,094 |

| S&P 500 | 6,204 |

| Nasdaq | 20,369 |

Bond Sector Yields:

| 2 Yr Treasury | 3.72% |

| 10 Yr Treasury | 4.24% |

| 10 Yr Municipal | 3.21% |

| High Yield | 6.80% |

YTD Market Returns:

| Dow Jones | 3.64% |

| S&P 500 | 5.50% |

| Nasdaq | 5.48% |

| MSCI-EAFE | 17.37% |

| MSCI-Europe | 20.67% |

| MSCI-Pacific | 11.15% |

| MSCI-Emg Mkt | 13.70% |

| US Agg Bond | 4.02% |

| US Corp Bond | 4.17% |

| US Gov’t Bond | 3.95% |

Commodity Prices:

| Gold | 3,319 |

| Silver | 36.32 |

| Oil (WTI) | 64.98 |

Currencies:

| Dollar / Euro | 1.17 |

| Dollar / Pound | 1.37 |

| Yen / Dollar | 144.61 |

| Canadian /Dollar | 0.73 |

Macro Overview: There’s a growing consensus among various economists and market analysts that inflation could force consumers to cut back on spending to the extent that a recession materializes. Consumer expenditures have an enormous impact on economic activity, representing 70% of Gross Domestic Product (GDP). Even the Federal Reserve seems to think that rising rates can pose a risk to the U.S. economy – but inflation has backed the Fed up against the ropes.

The Federal Reserve Bank of New York released a report in early May identifying concerns members of the Fed have. Among the concerns are that elevated and persistent inflation, coupled with a sharp rise in rates could slow economic activity causing an increase in delinquencies, bankruptcies, and other forms of financial distress. The report also identified uncertainty surrounding heightened commodity prices and geopolitical risks attributed to the ongoing Russian conflict. With that said, recession in my view is nearly unavoidable at this stage. My baseline belief is that the U.S. economy will likely be in a broad recession by mid-2023.

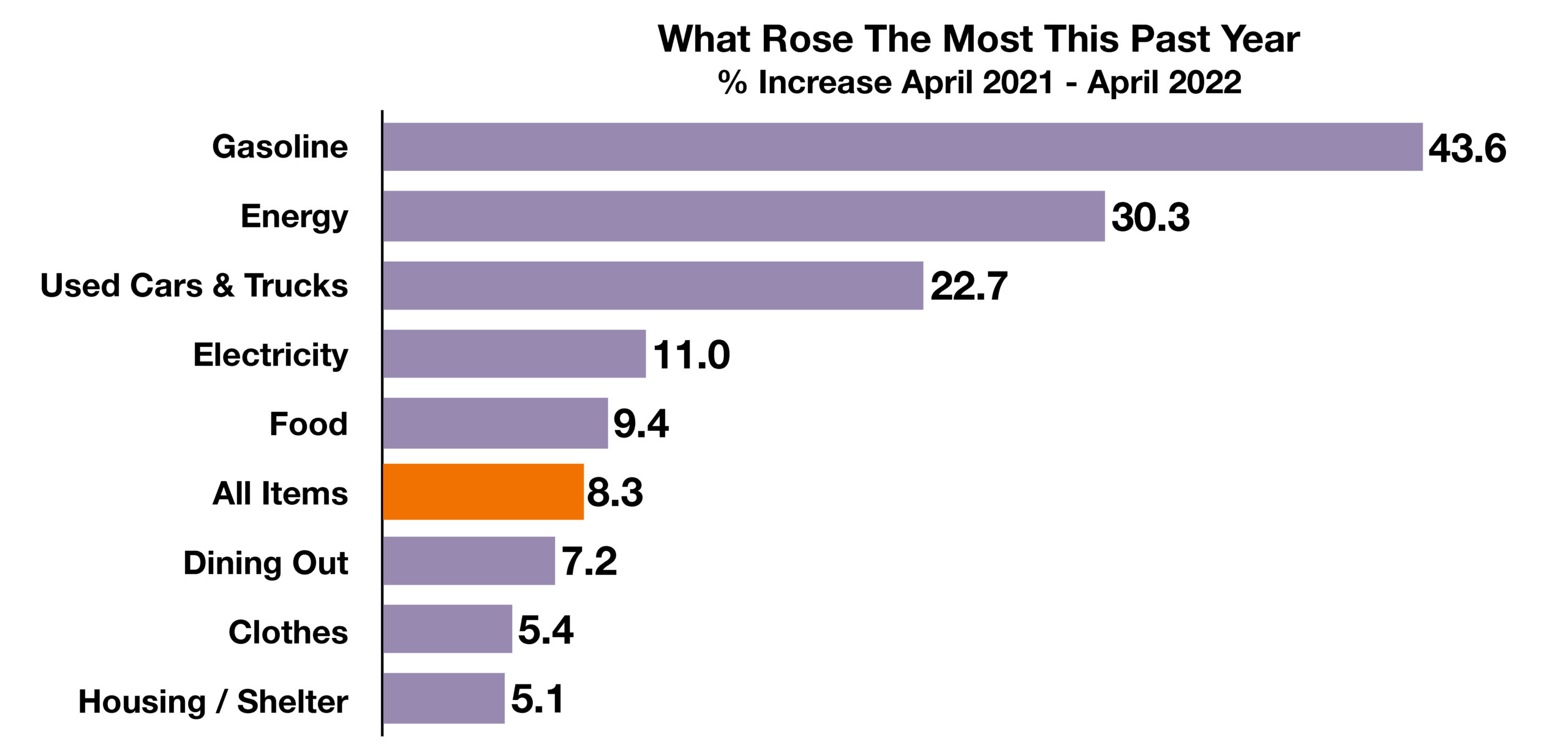

Inflation had seemed to have eased a bit in April, but underlying price pressures continue to identify gasoline and energy costs as the most acute for consumers. March data showed a decrease from 8.5% to 8.3% annualized inflation rate for all items. However, Today, June 10th, the May consumer price index showed a monthly rise of 1%, well above the 0.7% rise forecast by economists. The year-over-year rate rose 8.6%, topping the 40-year high of 8.5% seen in March.

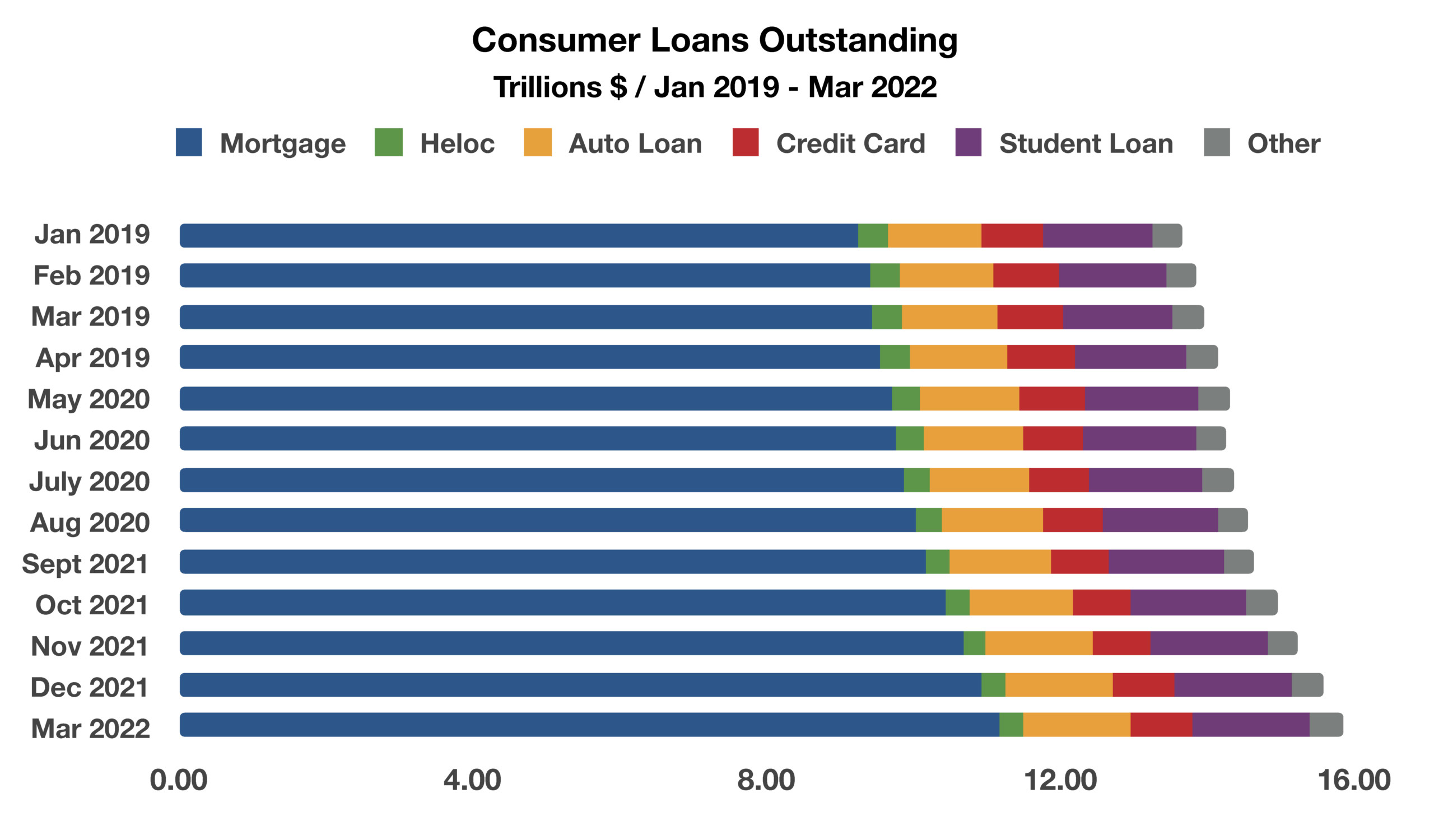

Federal Reserve data is indicating a rise in revolving credit card usage and a decrease in the savings rate. Consumer credit outstanding has risen the most since November 2001, when the economy was in recession. The Federal Reserve calculates that the average household is spending an additional $300 per month due to inflation. What does this mean? A segment of consumers are being forced to use credit cards to meet daily living costs as their savings are being depleted.

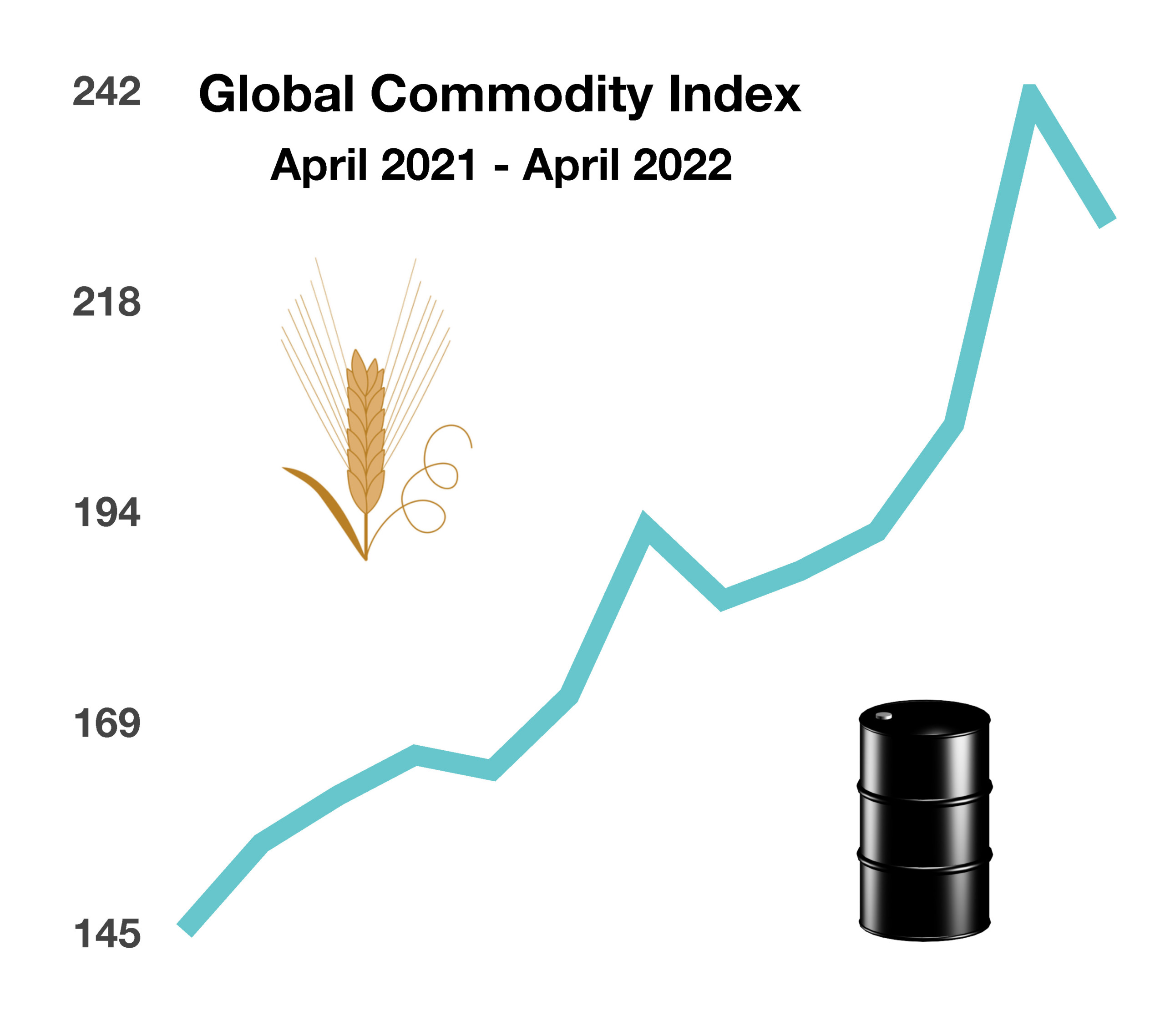

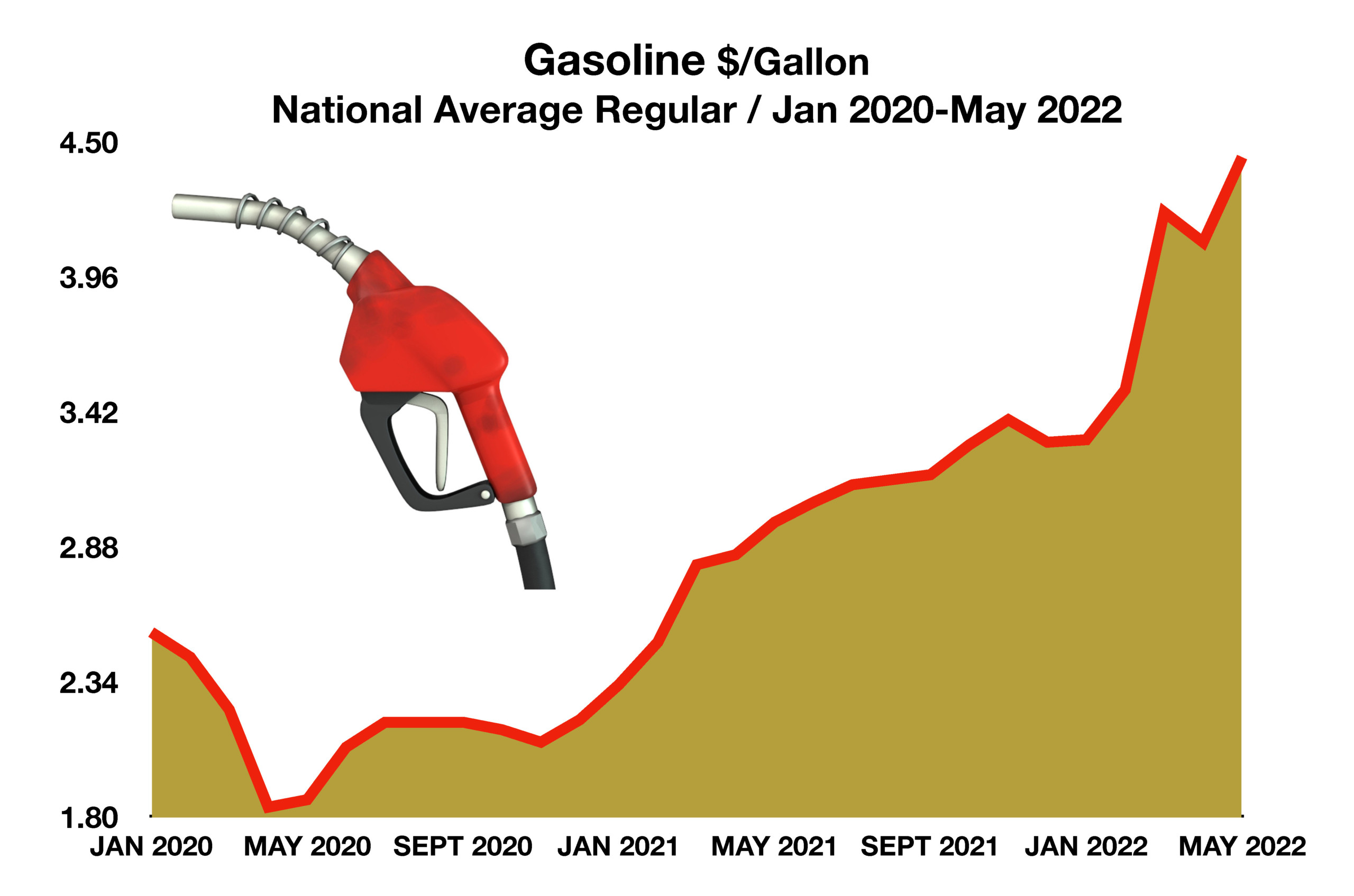

Soaring transportation costs are translating into higher prices for companies and consumers nationwide. A gallon of diesel has risen to over $5.50 this past month from $3.17 this same time last year. Diesel is the primary fuel used for transporting goods via trucks, trains, and shipping. The Federal Reserve plans to raise short term rates again in June and July – essentially, being forced to raise rates to combat inflation, all the while, the economy is slowing – not an ideal situation. Separately, according to the Federal Reserve, it now takes the average home buyer 10 years worth of wages to buy an average-priced single-family home, double the historical norm of 5 years worth of wages. A precursor to declining real estate prices?

The Federal Reserve plans to raise short term rates again in June and July – essentially, being forced to raise rates to combat inflation, all the while, the economy is slowing – not an ideal situation. Separately, according to the Federal Reserve, it now takes the average home buyer 10 years worth of wages to buy an average-priced single-family home, double the historical norm of 5 years worth of wages. A precursor to declining real estate prices?

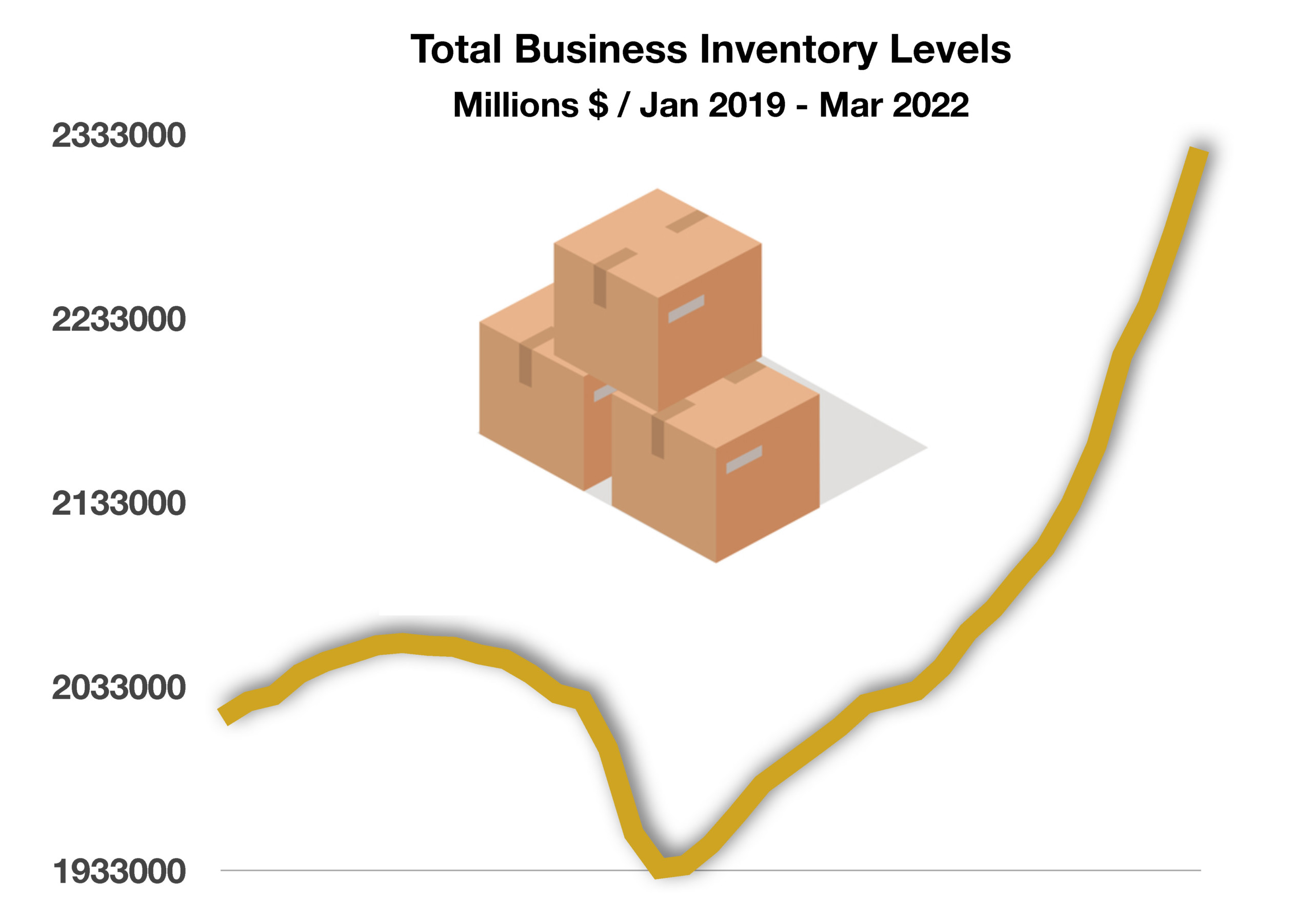

Now that constraints have lessened and various supply chains have resumed operations, companies have been accumulating raw materials and building a stockpile of finished products at an incredibility fast pace. Historically, increases in inventory levels have been an indication that demand for their goods might be weaning due to a pullback in business and consumer demand. As inventories swell, companies are eager to reduce stockpiles by discounting, which could mean lower prices for consumers.

Now that constraints have lessened and various supply chains have resumed operations, companies have been accumulating raw materials and building a stockpile of finished products at an incredibility fast pace. Historically, increases in inventory levels have been an indication that demand for their goods might be weaning due to a pullback in business and consumer demand. As inventories swell, companies are eager to reduce stockpiles by discounting, which could mean lower prices for consumers.