Michael McCormick

5 West Mendenhall, Ste 202 | Bozeman, MT 59715

406.920.1682 mike@mccormickfinancialadvisors.com

Sustainable Income Planning | Investments | Retirement

Stock Indices:

| Dow Jones | 39,118 |

| S&P 500 | 5,460 |

| Nasdaq | 17,732 |

Bond Sector Yields:

| 2 Yr Treasury | 4.71% |

| 10 Yr Treasury | 4.36% |

| 10 Yr Municipal | 2.86% |

| High Yield | 7.58% |

YTD Market Returns:

| Dow Jones | 3.79% |

| S&P 500 | 14.48% |

| Nasdaq | 18.13% |

| MSCI-EAFE | 3.51% |

| MSCI-Europe | 3.72% |

| MSCI-Pacific | 3.05% |

| MSCI-Emg Mkt | 6.11% |

| US Agg Bond | -0.71% |

| US Corp Bond | -0.49% |

| US Gov’t Bond | -0.68% |

Commodity Prices:

| Gold | 2,336 |

| Silver | 29.43 |

| Oil (WTI) | 81.46 |

Currencies:

| Dollar / Euro | 1.06 |

| Dollar / Pound | 1.26 |

| Yen / Dollar | 160.56 |

| Canadian /Dollar | 0.73 |

Summer Trail Running in the Tetons!

Dear Friends,

We just experienced a market selloff that was triggered by too much money in the system and runaway prices on most everything. The stock market bubble popped so hard that US Companies have seen ~$10 Trillion of value taken off their stock prices in just a few months. For most investors this means that their portfolio is now back to January 2021 valuations or even earlier.

This is how the market has been treating investors recently- harshly. Two years ago when the pandemic hit we lost ~40% in a week and two years before that in 2018 there was an 18% drop due to the taper tantrum. However, despite these selloffs, the S&P 500 has an annual 5-year return of +11% (as of this writing)! Enduring these scary times and the news that conflate it is the price investors pay for the growth the market provides.

I’m not discounting that we don’t have significant issues to solve before we get back to the races (we do and that’s what the rest of the newsletter is for). But while the challenges we face are new, this is normal stock market volatility. I believe we are below a fair value and for clients with surplus cash flows we are selectively putting money to work – prudently.

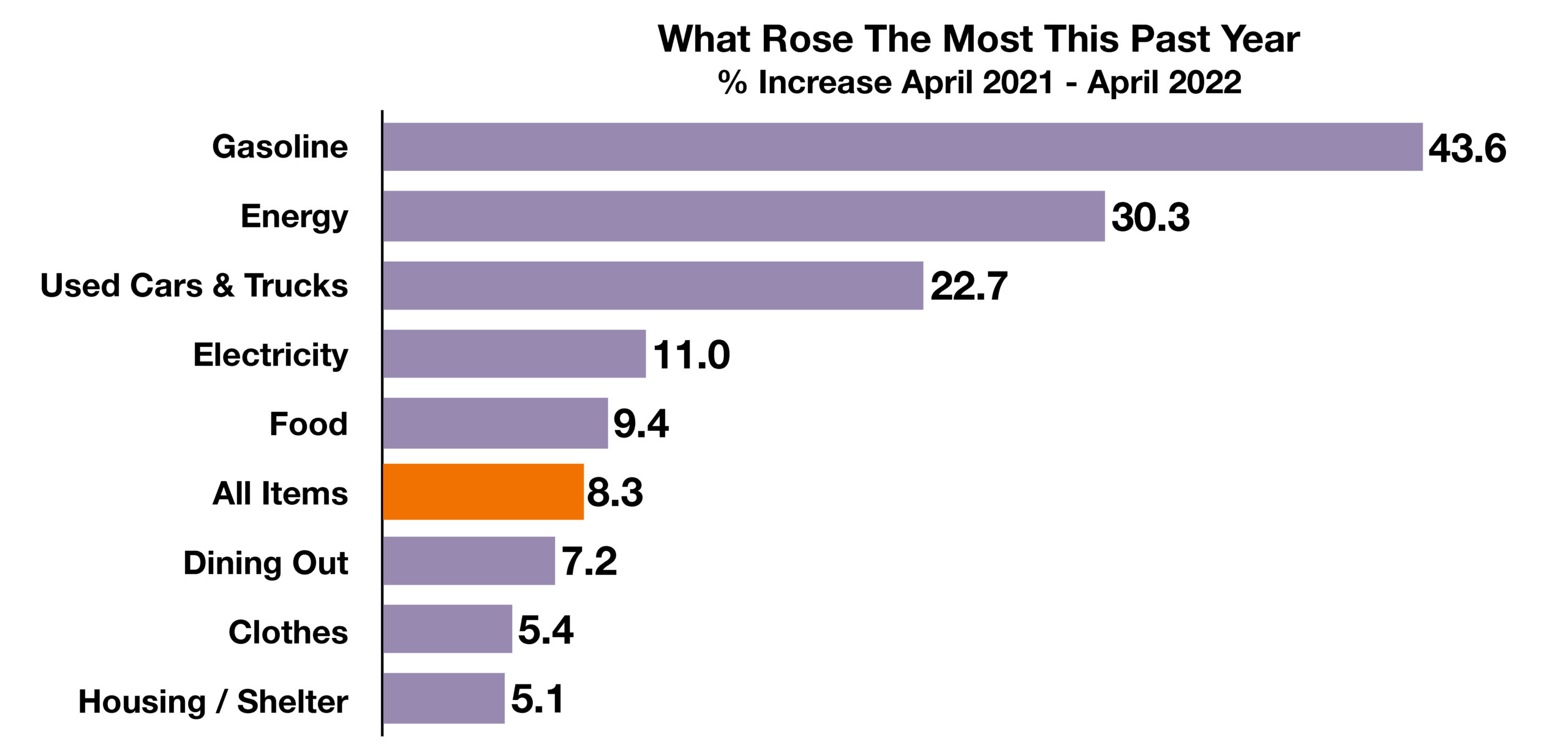

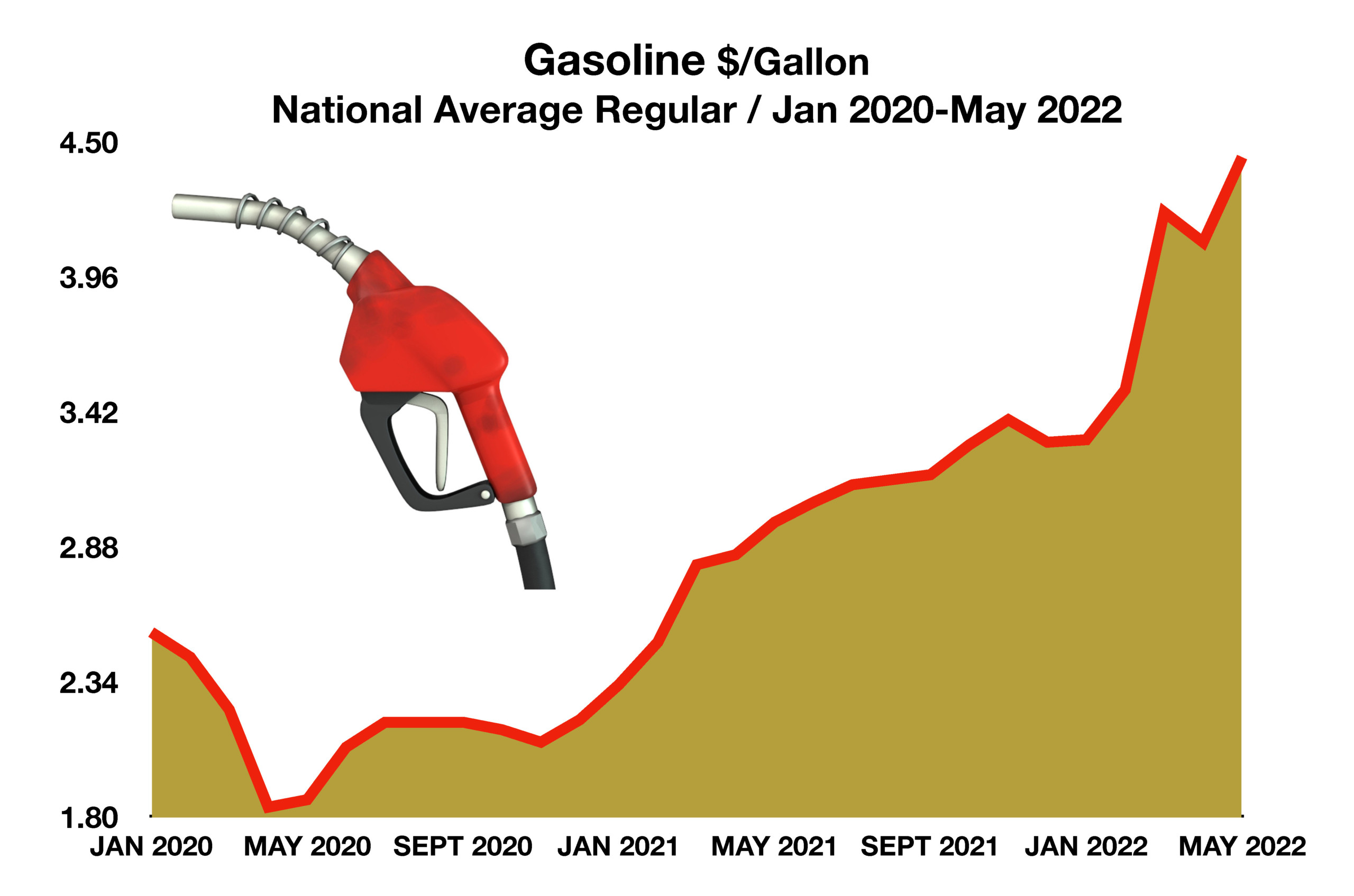

Surviving Inflation

While long term investors are accomplished at not putting too much importance on the day to day value of their accounts, ignoring inflation is another matter. Every day we pay more for the same goods and services than we did in the past. I can remember in the late 1970s taking a dollar to the 7-11 and walking out with 4 Full-Sized Candy Bars! (I did in-fact get a stomach ache). Higher prices are everywhere today and we experience that reality all day long. This is a great opportunity to sit down and analyze your own personal budget. Your credit card will offer you an online spending report that details where it all went. Print it out and look it over with your spouse. Make a goal of terminating a few recurring bills and to reduce spending in one category. Then, make sure the savings go into something you can use tomorrow to help keep up with inflation and keep your plan on track!

Sources: BLS, Labor Department, Federal Reserve Bank of Atlanta; HOAM, EIA