Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Macro Overview

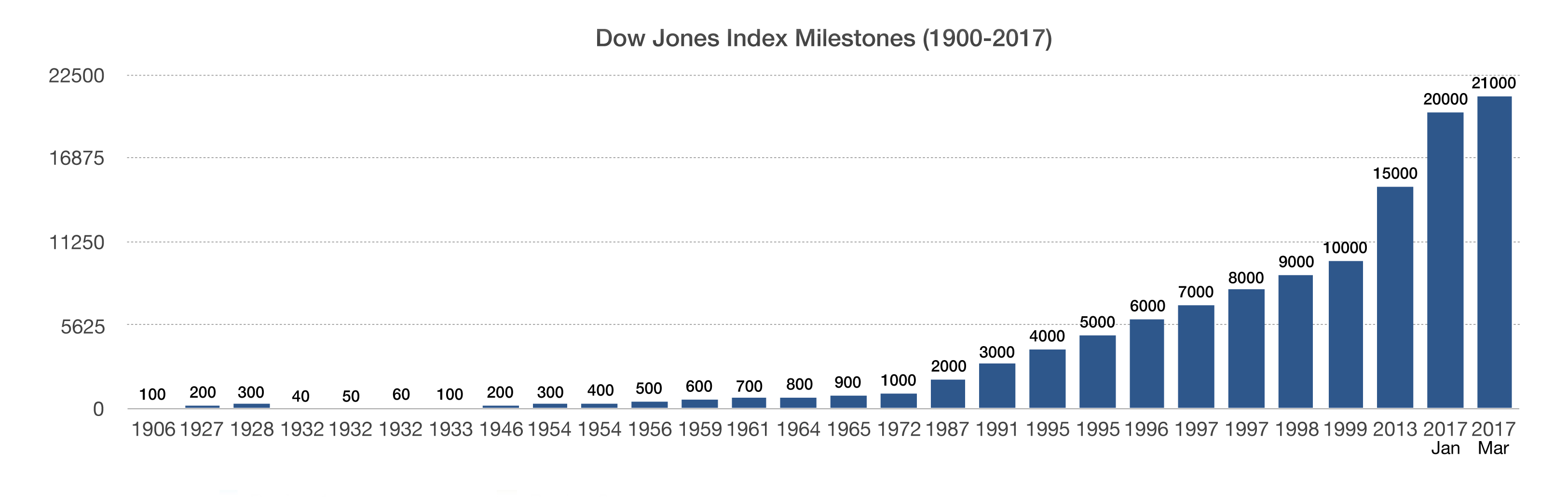

Equity indices had their longest streak of record closes since January 1987, with the Dow Jones Industrial Average reaching 21,000, its second milestone in less than 30 days after reaching 20,000. It took the Dow only 24 trading days to elevate from 20,000 to 21,000, tying a record set in 1999.

Executives from 16 major U.S. companies urged Congress to pass a comprehensive rewrite to the U.S. tax code, including implementing a controversial border tax. Many U.S. companies believe that a border tax would make their products more competitive in the international markets. The border tax proposal has also drawn criticism from U.S. companies such as automobile manufacturers and retailers that require imports and whose margins would fall with border tax payments.

Reflation has become the new inflation as growth expectations are heating up prices, production costs, and wages. Higher wages eventually lead to inflationary pressures because employers pass higher costs along to consumers. Some higher prices for consumers are expected with President Trump’s proposals, yet at the same time rising wages may offset higher prices.

U.S. retail stores are struggling due to e-commerce competition and slowing mall traffic. The downturn has led to the highest level of credit distress among the sector since the recession of 2008-2009, according to Moody’s Credit Rating agency.

The anticipation that Congress might start repealing portions of Dodd-Frank banking regulations, signed into law following the financial crisis, is driving bank sector stocks higher.

The Federal Reserve made its first rate decision under the Trump administration in February, leaning towards a rate increase as early as March.

The Tax Policy Center, a nonpartisan independent entity in Washington, believes that the tax proposals presented by the president may not become effective until 2018 at the earliest since passage by Congress takes time.

Due to IRS efforts to prevent fraud, tax refunds will be delayed for households claiming the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit (ACTC). It is estimated that about 25 – 30 million households will need to wait to get their refunds creating cash flow disruptions in February and March. Historically, tax payers receiving refunds tend to spend the funds almost immediately.

The Department of Labor is delaying the fiduciary rule from going into effect until June 9th. It was originally scheduled to become effective April 10th, but the department has decided to allow more time to solicit feedback from industry professionals and the public. The fiduciary rule is only affecting retirement accounts for the time being, requiring that investment advisors put the best interests of the investor first.

Sources: Labor Dept., IRS, Fed, Dow Jones, S&P

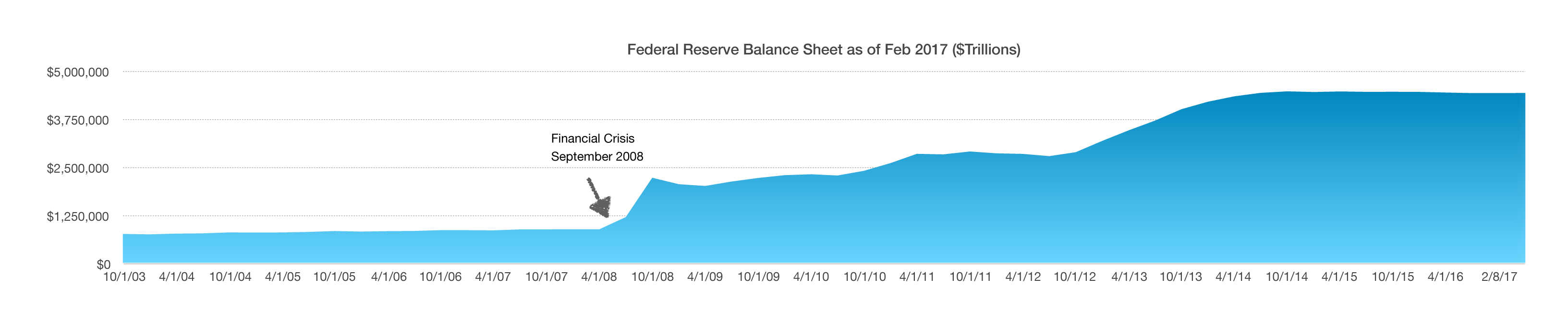

Many bond traders expect that as MBS bonds start to flow off the Fed’s balance sheet, it will allow private buyers such as mutual funds and pension funds to essentially take over the buying from the Fed. The hope is that in conjunction with alleviation of certain Dodd-Frank rules that limit trading by banks and financial institutions in government securities, these two dynamics may encourage new market participants to become buyers of what the Fed is selling. (Sources: Fed, U.S. Treasury)

Many bond traders expect that as MBS bonds start to flow off the Fed’s balance sheet, it will allow private buyers such as mutual funds and pension funds to essentially take over the buying from the Fed. The hope is that in conjunction with alleviation of certain Dodd-Frank rules that limit trading by banks and financial institutions in government securities, these two dynamics may encourage new market participants to become buyers of what the Fed is selling. (Sources: Fed, U.S. Treasury)