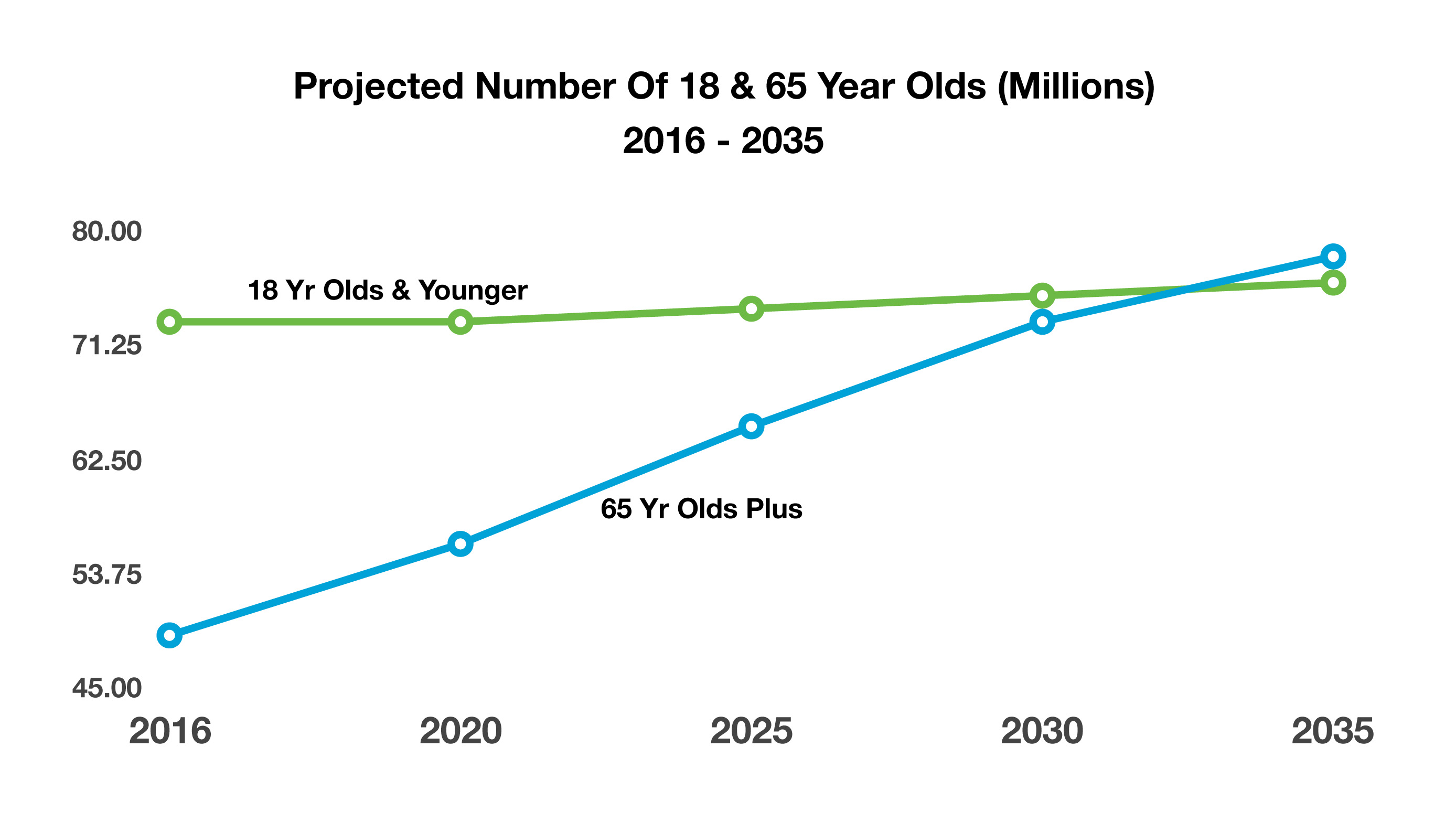

65 Year Olds Projected To Exceed 18 Year Olds – Demographics

Demographics and population data are carefully tracked by the Census Bureau in order to better determine what the United States may look like in the future.

Over 73 million minors, under 18 years of age, currently out number 49 million older Americans, 65 and over. Younger citizens help spur economic growth and provide essential workers for the l abor market. The demographical make-up of the country has been driven by the baby boom generation for decades. Those born between 1946 – 1964 have shaped the economic status of our country while providing economic growth and vitally skilled workers. The first wave of baby boomers reached 65 years of age in 2011, starting a massive shift of individuals from working status to retirement status.

abor market. The demographical make-up of the country has been driven by the baby boom generation for decades. Those born between 1946 – 1964 have shaped the economic status of our country while providing economic growth and vitally skilled workers. The first wave of baby boomers reached 65 years of age in 2011, starting a massive shift of individuals from working status to retirement status.

The Census Bureau estimates that by 2035, those age 65 and older will begin to out number 18 and under. The number of 65 year olds and older will rise much faster than those 18 and younger creating a strain on the U.S. job market and economy. The shrinking pool of minors will eventually lead to lower population growth thus creating a drag on economic growth. A growing elderly population is expected to impact already strained Medicare and Social Security benefits. (Source: U.S. Census Bureau)

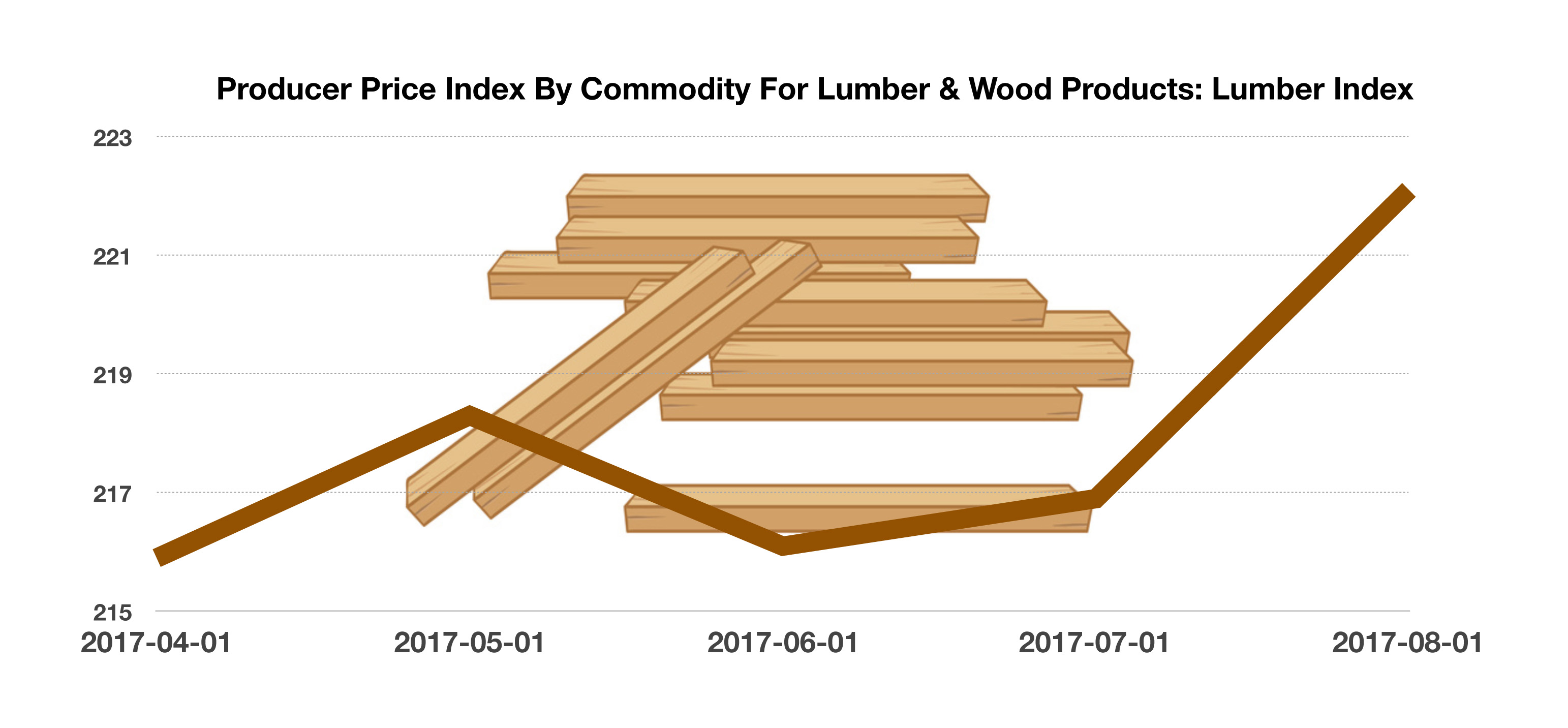

Lumber Supplies Pose Challenge For Housing – Housing Update

The fierce storms that ravaged Texas and Florida last year, in addition to the horrendous fires in Northern California, have led to a rise in demand for construction materials including lumber. Homebuilders use a multitude of raw and finished materials for the construction of homes, including wiring, plastic tubing, and lumber. The increase in demand has decre ased the supply forcing prices higher. Builders are passing along the higher costs to home buyers thus pushing housing prices upward. In addition to the lack of supply contributing to rising prices, a recent imposition of tariffs on Canadian timber is also adding pressure. Less expensive Canadian lumber has been a primary source for builders. Suppliers to homebuilders are essentially running low on levels of lumber all over the country, as lumber prices are on the rise with homebuilders also gearing up for the summer season. Various other factors are also affecting lumber prices nationwide, such as thousands of new homes under construction, and young families eager to purchase a new home before rising rates dampen their chances.(Source: Commerce Department)

ased the supply forcing prices higher. Builders are passing along the higher costs to home buyers thus pushing housing prices upward. In addition to the lack of supply contributing to rising prices, a recent imposition of tariffs on Canadian timber is also adding pressure. Less expensive Canadian lumber has been a primary source for builders. Suppliers to homebuilders are essentially running low on levels of lumber all over the country, as lumber prices are on the rise with homebuilders also gearing up for the summer season. Various other factors are also affecting lumber prices nationwide, such as thousands of new homes under construction, and young families eager to purchase a new home before rising rates dampen their chances.(Source: Commerce Department)