Ocean Park Capital Management

2503 Main Street

Santa Monica, CA 90405

Main: 310.392.7300

Daily Performance Line: 310.281.8577

Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Portfolio Overview

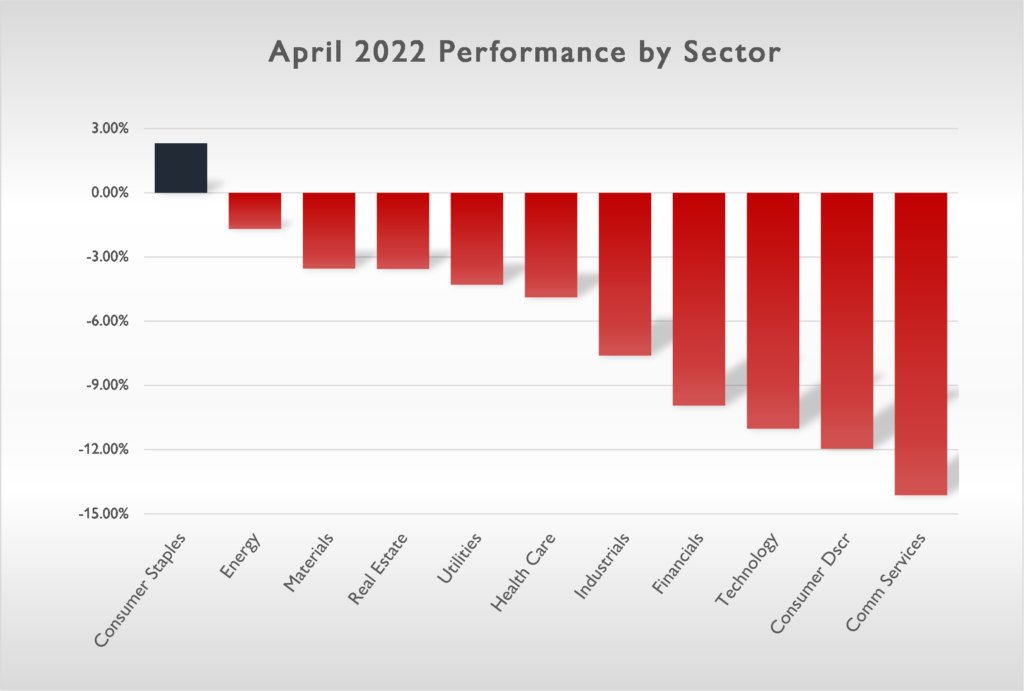

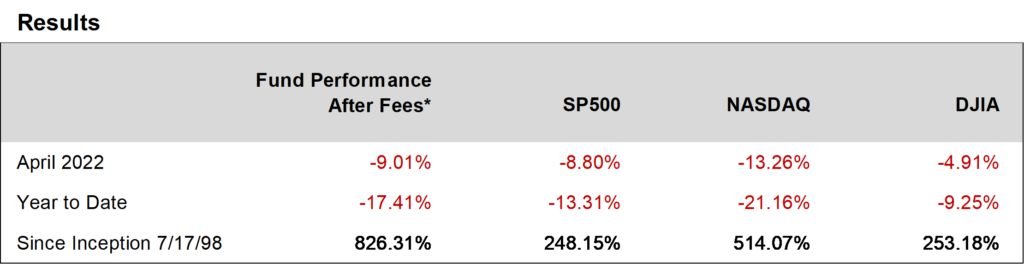

Ocean Park Investors Fund fell 9.01%* in April, while the S&P 500 fell 8.8% and the NASDAQ Composite fell 13.26%. High inflation, interest rate hikes, slowing economic growth, the war in Ukraine, and Covid shutdowns in China formed a perfect storm that swamped markets. Consumer and technology stocks, which have provided the greatest long-term gains for the portfolio, were particularly hard-hit.

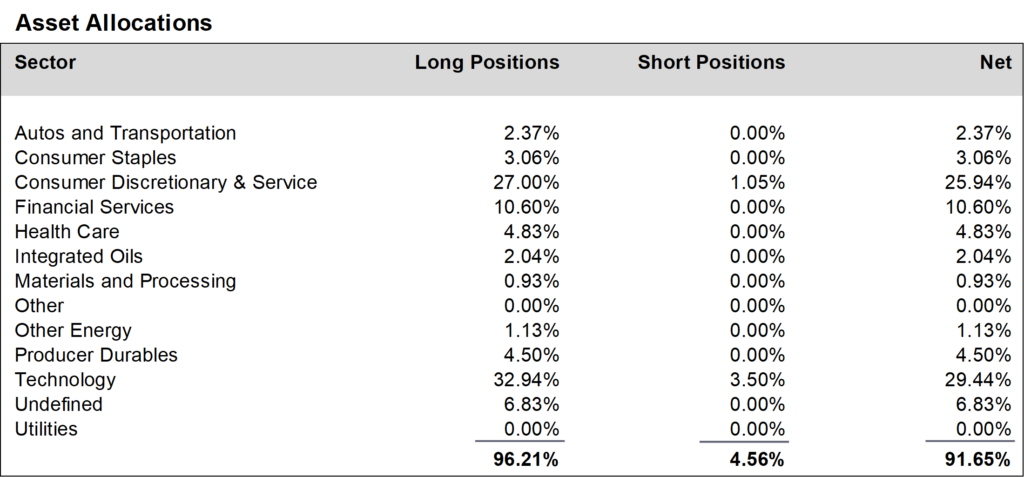

During April, we reduced positions in the technology sector and the consumer discretionary and service sector and increased exposure to the SPY ETF. More significantly, during the decline we maintained our 92% net long exposure, unchanged from March. We recognize that the downturn in the market is painful. However, we view it as transitory and therefore believe it is important to stick to our discipline of identifying stocks with better-than-expected earnings potential which have historically generated strong returns over the long run.

Daily updates on our activity are available on our Results Line, at 310-281-8577, and current information is also maintained on our website at www.oceanparkcapital.com. To gain access to the site enter password opcap.

*These results are pro forma. Actual results for most investors will vary. See additional disclosures on page 4. Past performance does not guarantee future results.