Market Update

(all values as of 03.29.2024)

Stock Indices:

| Dow Jones | 39,807 |

| S&P 500 | 5,254 |

| Nasdaq | 16,379 |

Bond Sector Yields:

| 2 Yr Treasury | 4.59% |

| 10 Yr Treasury | 4.20% |

| 10 Yr Municipal | 2.52% |

| High Yield | 7.44% |

Commodity Prices:

| Gold | 2,254 |

| Silver | 25.10 |

| Oil (WTI) | 83.12 |

Currencies:

| Dollar / Euro | 1.08 |

| Dollar / Pound | 1.26 |

| Yen / Dollar | 151.35 |

| Canadian /Dollar | 0.73 |

2017 Mid-Year Update & Outlook

- We believe solid earnings growth, low oil prices and a weaker dollar were the primary drivers of markets in the second quarter. Stocks around the world are benefiting from a backdrop of stable growth and falling inflation.

- The resounding victory by President Macron in France and the poor showing by the Conservatives in the UK turned the tide against the forces of isolation in Europe. European markets and the Euro responded positively and began to unlock the value we believe exists there.

- In the US, President Trump’s political agenda has been stymied by Republicans’ failure to agree on healthcare reform. Tax reform will have the biggest impact on risk assets and a stock market correction could be triggered if progress on tax reform is pushed out into 2018.

- Commodity prices fell, led by oil as US production continues to ramp up, driven by ever improving technological advances, even as OPEC tried to maintain production cuts. This provided a benign inflation backdrop.

- 10-year Treasury Note yields were little changed even as the Federal Reserve raised interest rates by a further 0.25%. The yield ended the quarter at 2.3%.

Remain Overweight to Equities and Added to Emerging Markets

- Our tactical and strategic portfolios are positioned to reflect our belief that stocks will outperform bonds this year, but that the best returns will come from the international markets. Our momentum indicators support our overweight position as the primary trends for most major stock markets are up.

- Our preference for non-US stocks increased during Q2. The relative value case has been apparent to us for several years, but relative momentum has been lacking until this year. We added to emerging markets early in the quarter, and expect the recent trend of positive relative price and economic momentum to continue.

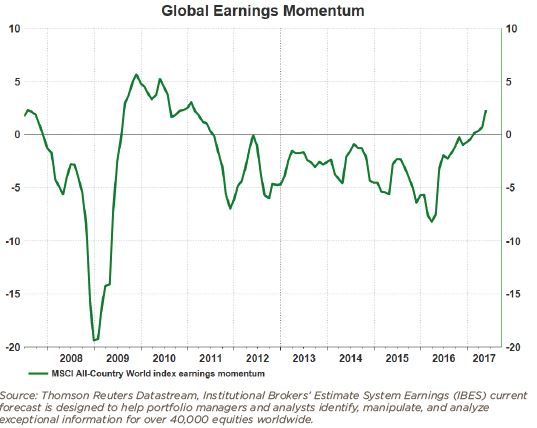

- We are seeing global earnings momentum improve to its strongest level since 2010, with a particular emphasis on areas like the Eurozone, Japan and emerging markets. We view this as positive for global stock markets.