Macro Overview

Worries regarding a second wave of infections heading into the fall, election uncertainties,

and wavering economic indicators contributed to a dubious September.

Equities paused from their upward trajectory in September, with technology stocks repelling

from their highs. Uncertainty surrounding vaccine deployment and the election are expected

to influence market momentum and investor confidence. Election results will help determine

the direction of fiscal policy and social program funding.

A growing number of pharmaceutical companies, universities, and biotech firms are

introducing and testing various forms of vaccines to combat COVID-19. According to the

Regulatory Affairs Professional Society (RAPS), there are currently over 40 COVID-19 vaccines

in trial phases worldwide.

California became the first state to require that all new autos sold be zero-emission by 2035.

The executive order issued by the state’s governor is expected to reverberate throughout the

country, possibly leading other states to follow suit.

The Centers for Disease Control and Prevention (CDC) issued detailed guidance for this

Halloween season. Among them, not to substitute a costume mask for a cloth mask, not to

attend crowded costume parties, avoid visiting indoor haunted houses, and refrain from

traditional door to door trick-or-treating.

With some schools resuming across the country, the CDC reported that COVID-19 cases in 19 year olds and younger have risen three-fold since May. The large increase may suggest that younger people may play an

increasingly important role in community transmission, even if their risk of serious illness is low relative to

the older population. The threat of a second wave of infections brought

about by COVID-19 are reminiscent of the fall of 1918, when the second wave of the Spanish

flu pandemic was more severe than the first.

Comments by Fed Chairman Jerome Powell indicated that additional aid to small businesses

and unemployed individuals was critical for economic expansion during the pandemic. The

Fed Chair urged for the passage of a second stimulus package, which has been delayed due

to a Congressional impasse.

Banks and finance companies have been imposing more stringent standards for consumer

and business borrowers, as noted by the Fed’s Senior Loan Officer Survey. The survey

identified reductions in credit card limits, as well as tougher qualifications for auto and home

loans. (Sources: www.cdc.gov/coronavirus/2019/html#halloween, CDC, Federal Reserve,

World Bank, www.gov.ca.gov/2020/09/23/governor-newsom)

THE FED PURCHASES $120 BILLION OF TREASURY AND MORTGAGE BONDS EACH MONTH

Equities Taper Off In September – Domestic Equity Overview

Despite a pullback in September, equities managed to end the third quarter with gains. The technology

sector was the primary contributor to the S&P 500 Index, which was up 8.93% for the third quarter.

Consumer discretionary and industrial stocks also performed well during the quarter, exemplifying some

economic recovery characteristics.

Following an upward surge during this summer, September witnessed a tapering of equity momentum,

leading to lower valuations. The three major equity indices, Dow Jones Industrial, S&P 500 Index, and the

Nasdaq were off in September, but positive for the third quarter ending September 30th. (Sources: S&P,

Bloomberg, Dow Jones, Nasdaq)

Rates Vacillate As Stimulus Efforts Unresolved – Fixed Income Overview

The Federal Reserve continues to purchase $120 billion of Treasury and mortgage agency bonds each

month, expanding its balance sheet to over $7 trillion as of the end of September. The monumental buying

is meant to facilitate bond market activity while maintaining a relatively low-rate environment.

Yields on government and corporate bonds vacillated in September as uncertainty surrounding additional

stimulus efforts influenced rates. Analysts and economists expect higher long-term rates to result from the

incremental debt issuance to pay for the next stimulus package. (Sources: U.S. Treasury, Federal Reserve,

Bloomberg)

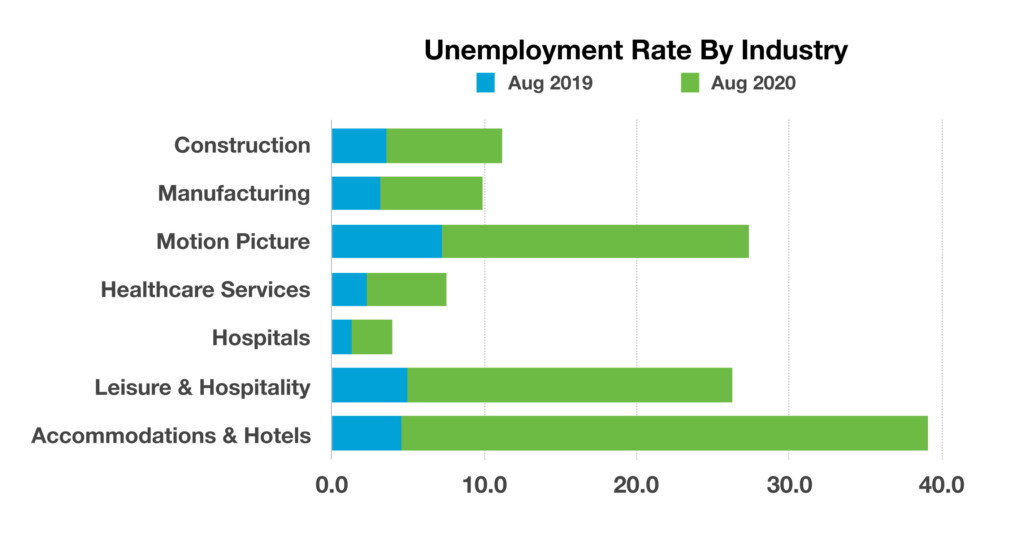

Industries That Are Experiencing Higher Unemployment Due To The Pandemic – Labor Market

Overview

The most recent labor statistics made available by the U.S. Department of Labor is identifying more

impactful increases in unemployment in certain industries than others. Economists and analysts believe

that the year-over-year increases in unemployment are attributable to the pandemic, where mandatory

closures and restrictions are continuing to hinder businesses and workers nationwide.

Unemployment is affecting various occupations differently, as the impact of the pandemic displaces

certain workers more than others. Economists believe that the disparity enhances the negative affects on lower

income workers versus higher earnings, creating even more inequality among the nation’s workforce.

Industries such as construction, motion pictures, hotel & leisure, and restaurants saw the most dramatic

increases in unemployment relative to a year prior. Hospitals and health services saw the least amount of

increases in unemployment, showing resistance to the current pandemic environment.

Source: U.S. Department of Labor

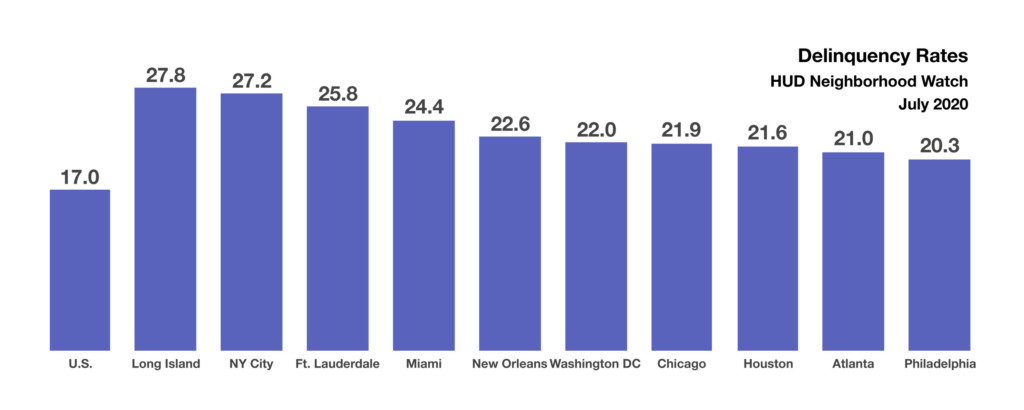

17% OF ALL FHA-INSURED LOANS WERE DELINQUENT IN JULY OF THIS YEAR

What’s In Store For The Housing Market – Housing Market Update

Euphoric media reports about the housing market are starting to come into question, as the fragility of the

housing market is gradually being exposed. The FHFA House Price Index revealed that housing prices

nationwide rose a paltry 5.4% in the past year, with some regions seeing much slower growth.

The onset of

the pandemic in March brought about

a flurry of

stimulus

efforts meant

to ease the

financial

burden for

millions of

Americans. Housing was a primary concern as the unemployment rate spiked and paychecks dwindled. In

response, the Federal Housing Finance Administration (FHFA) announced a moratorium for both evictions

and foreclosures through August 31, 2020. That moratorium has since been extended to the end of the

year to allow homeowners additional time to sort out and catch up on their rent and mortgage payments.

Any federally backed loans, such as FHA-insured loans, have allowed homeowners to skip their mortgage

payments by means of forbearance. According to the Mortgage Bankers Association, roughly 3.5 million

home loans were

in forbearance as

of September 6th,

representing

7.01% of all FHA insured

loans. In

addition to

homeowners in

forbearance,

there are those homeowners that are delinquent on the loans. It is expected that millions of homeowners on

forbearance will become delinquent on those loans by the end of 2020, including many who have not made

a payment since March of this year. Another government housing entity, the U.S. Department of Housing

and Urban Development (HUD) tracks loans in delinquency via its Neighborhood Watch list. The data

reported that 17% of all FHA-insured loans were delinquent in July of this year. The figure includes

mortgages in forbearance as well as those not in forbearance.

Sources: Federal Housing Finance Administration, Mortgage Bankers Association, U.S. Department of

Housing and Urban Development

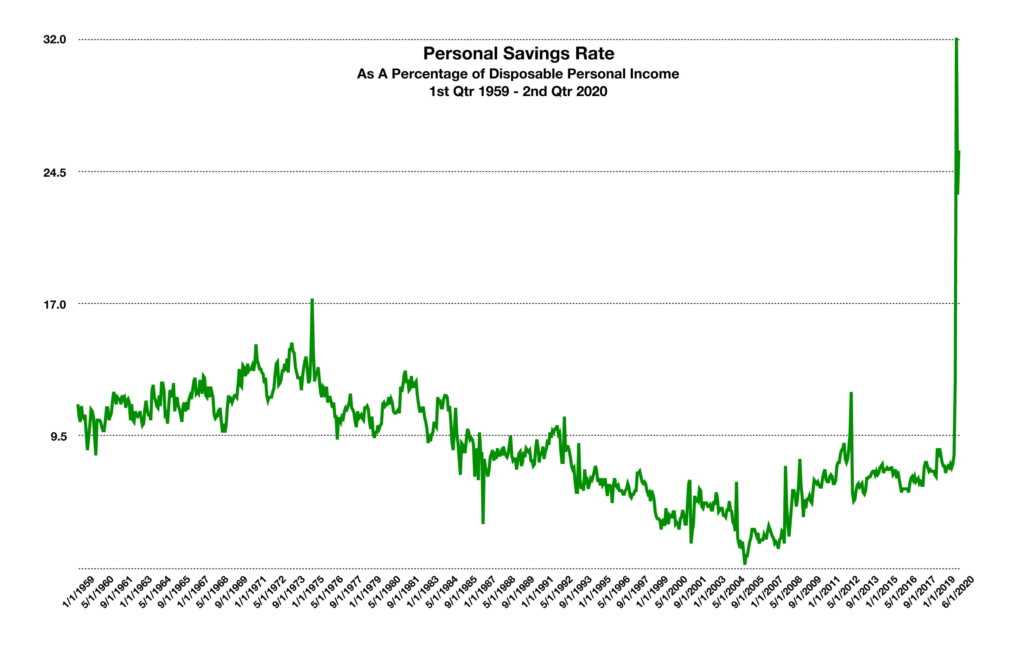

CURRENT SAVINGS RATE OF 25.7% IS NEARLY TRIPLE OF THE 60-YEAR AVERAGE

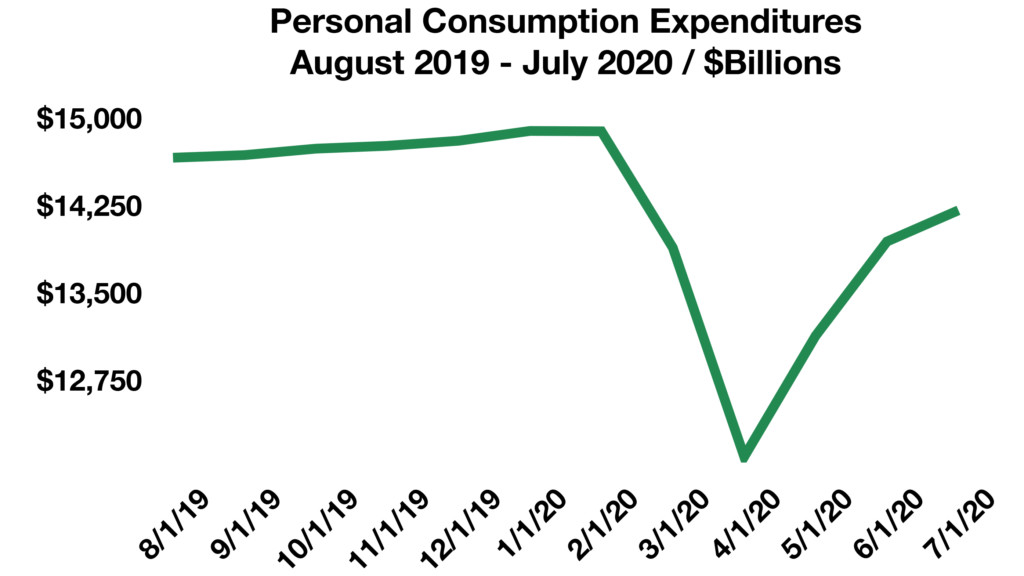

Americans Saving More Amid Pandemic – Consumer Behavior

Store and restaurant closures have prompted consumers nationwide to stay home, spend less, and save more. Dwindling consumer confidence along with uncertainty surrounding the job market, has shifted many from a spending mode to a saving mode. The average savings rate for the past 60 years since 1959,

has been 8.9%. The savings rate jumped from 8.4% in February this year to 32.2% in April as the pandemic took hold of the U.S. economy. The most recent data release shows the savings rate at 25.7% for the quarter ending June, nearly triple of the 60-year average.

Economists view the heightened level of savings as restrictive to a sustained economic expansion.

Since nearly 70% of GDP is represented by consumer expenditures, higher savings tend to take away from spending throughout the economy. Consumer confidence is also a factor as a lack of confidence tends to increase savings while minimizing spending. (Source: https://fred.stlouisfed.org)

California To Become First State To Require Zero-Emission Vehicles – Auto Industry Overview

The governor of California issued an executive order in September requiring that all automobiles sold in the state would be zero-emission by 2035. The announcement gives auto manufacturers 15 years to transition from gasoline and diesel engines to zero-emission engines. The state order did not specify what

form of zero-emission engines would be required, such as battery or hydrogen powered. Sales of used gasoline powered vehicles, however, would still be allowed. California has become the first state to require a transition from gasoline to zero-emission vehicle sales, essentially outlawing new non zero-emission

vehicle sales. The new requirement may eventually affect other states as California has traditionally set trends with environmental regulations nationwide. Auto manufacturers will have to convert and expand production to produce the demand expected for zero-emission vehicles over the next 15 years. As of this

past August, there were only 543,610 registrations nationwide for electric automobiles, representing less than one percent of the 273.6 million vehicles currently registered in the United States. California has historically been the largest zero-emission auto market in the country, with Oregon and Washington states

a distant second and third.

In response to California’s executive order, the Environmental Protection Agency (EPA) argued that the mandate is impractical and possibly illegal under current Federal legislation. The EPA noted that California, like some other states, is already suffering from rolling blackouts, affecting residences and businesses

statewide. The additional electric automobiles would impose additional strain on the electric grid further crippling its ability to efficiently distribute energy. (Sources: www.library.ca.gov, U.S. Department of Energy)

OVER $1 TRILLION OF MORTGAGE BONDS HAVE BEEN PURCHASED BY THE FED SINCE MARCH

Pandemic Driven Spending May Not Be Consistent – Pandemic Effects

Spending soared in May to a record 8.2%, reported by the Commerce Department, accompanied by an increase in personal income which rose 10.5% in April.

Many analysts and economists believe that spending among U.S. consumers following the onset of the stimulus payments may be misleading, with any increase in spending merely temporary, as the benefits of the payments fade. Income figures may also be skewed as stimulus payments and generous unemployment benefits have artificially increased incomes for some lower income families.

Source: U.S. Commerce Department

Less Choices Are Here To Stay – Consumer Behavior

In response to the COVID-19 pandemic, American consumer choices have changed in the realm of diet, food preparation, and lifestyle habits. The transition into at-home cooking as a means of financial saving and risk reduction has expanded through American society and is projected to leave both short-term and long-term effects on consumer choices.

In addition to consumer impact, retailers are also experiencing drastic changes in food choices as a result of the pandemic; grocery stores have begun to reduce food options while large corporate retailers have also transitioned into limited offerings. Consumer choice reductions by American retailers have resulted from stressed supply chains and market preferences leaning towards familiar brands.

The short-term effects of the pandemic on consumer choices across industries are projected to shift long-term as some companies plan to commit to fewer choices post pandemic. The desire for retailers to limit product variety stems from efforts to manage demand increase by simplifying. In-house dining is another realm of industry that has adjusted on the basis of the pandemic as more employees face job security threats. Restaurants have begun reducing menu options in order to mitigate extensive labor or supply costs that would often be needed in a growing and expanding food industry. The automotive industry is also feeling the effects of the pandemic and many automakers have begun the transition to limited supply and variety in hopes to salvage extraneous costs within the supply chain and decreased sales.

Uncertainty regarding the long-term effects of consumer choices remains, though some retailers have approached the transition with permanence and voiced limited desires to return to broadened product choices. The immediacy and simplicity created by fewer choices for both the retailers and consumers lends the debate towards the permanence or temporary incentives behind retailers’ consumer choice reductions long term.

Sources: U.S. Department of Agriculture; Economic Research Service

IRS COLLECTED $28 BILLION IN 2010 FROM AUDITS & ONLY $11 BILLION FROM AUDITS IN 2019

COVID Is Making It Difficult For The IRS To Audit & Collect Taxes Owed – Fiscal Policy

As the pandemic has taken a toll on income for individual businesses, companies, and families across the country, it has also taken a toll on U.S. government income. The IRS releases a disclosure annually of the sources of income collected from taxes. Part of the revenue generated by the IRS is the enforcement of tax collections primarily via audits. The IRS report revealed that the number of audits in 2019 was among the lowest in decades for individual returns, the single largest source of income for the IRS.

Fewer audits means less revenue for the U.S. government, which has this year already issued over $3 trillion in debt since March of this year. The IRS collected roughly $28 billion in 2010 from audits, versus $11 billion that was collected in 2019.

This year has become that much more challenging, as IRS employees and agents have been removed from the field due to pandemic restrictions. The inability to perform face to face audits has made it that more difficult for the IRS to collect on taxes owed.

Source: IRS Annual Disclosure Report, IRS Data Book 2019 Release)

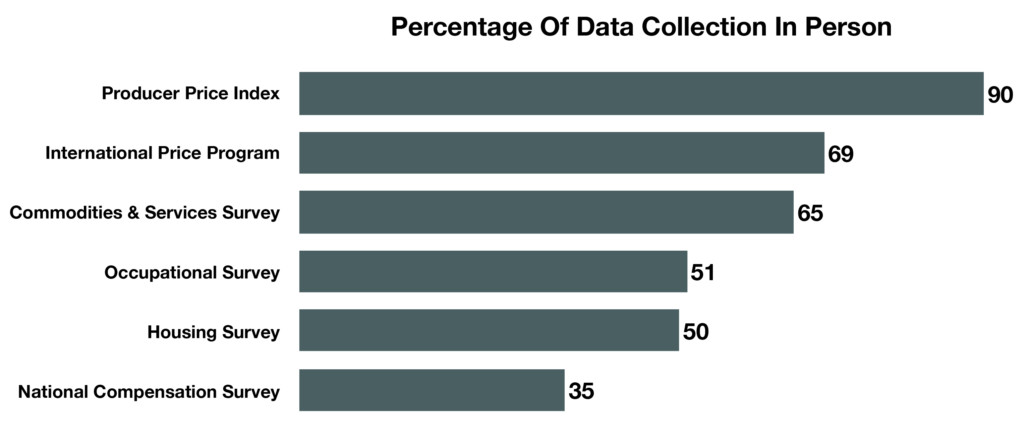

Government Data Collection Hindered By The Pandemic – Economic Dynamics

Among the many disruptions caused by the pandemic, government data collection has been hindered considerably. Various agencies and departments of the federal government have relied on personal collection of data for decades as a reliable and validated process of gathering data. Numerous economic indicators and indices are vital for economists and government officials to decipher what the economic condition of the country might be. The pandemic has now raised the question as to whether data collection has been flawed and if certain government provided reports are truly accurate.

Natural disasters such as hurricanes and fires have affected data collection efforts in the past as face to face surveys have been delayed if not limited in scope. The significance of the current pandemic though, has created data collection challenges that have never occurred before.

The Bureau of Labor Statistics has acclimated to the new environment by instituting surveys by telephone and by examining publicly available data. Inflation has been difficult to gauge, as random price spikes over the past few months have misled economist and the Federal Reserve. The Consumer Price Index (CPI) not only is the leading indicator for inflation, but it is also used to modify and establish tax rates, Social Security benefits, poverty thresholds, and eligibility requirements for food stamps.

This year, the Census of 2020 has been delayed and jeopardized, as in-person surveys have been essentially canceled. Instead the U.S. Census is relying on self-response rates, where U.S. citizens effectively count themselves via the Census 2020 internet portal. The Census, which only occurs every 10 years, helps determine the number of seats in the House of Representatives for each state, voting districts, and the allocation of federal funds nationwide.

Sources: BLS, U.S. Census, Dept of Labor, Federal Reserve

younger have risen three-fold since May. The large increase may suggest that younger people may play an

younger have risen three-fold since May. The large increase may suggest that younger people may play an

The onset of

The onset of hly 3.5 million

hly 3.5 million

Numerous economic indicators and indices are vital for economists and government officials to decipher what the economic condition of the country might be. The pandemic has now raised the question as to whether data collection has been flawed and if certain government provided reports are truly accurate.

Numerous economic indicators and indices are vital for economists and government officials to decipher what the economic condition of the country might be. The pandemic has now raised the question as to whether data collection has been flawed and if certain government provided reports are truly accurate.