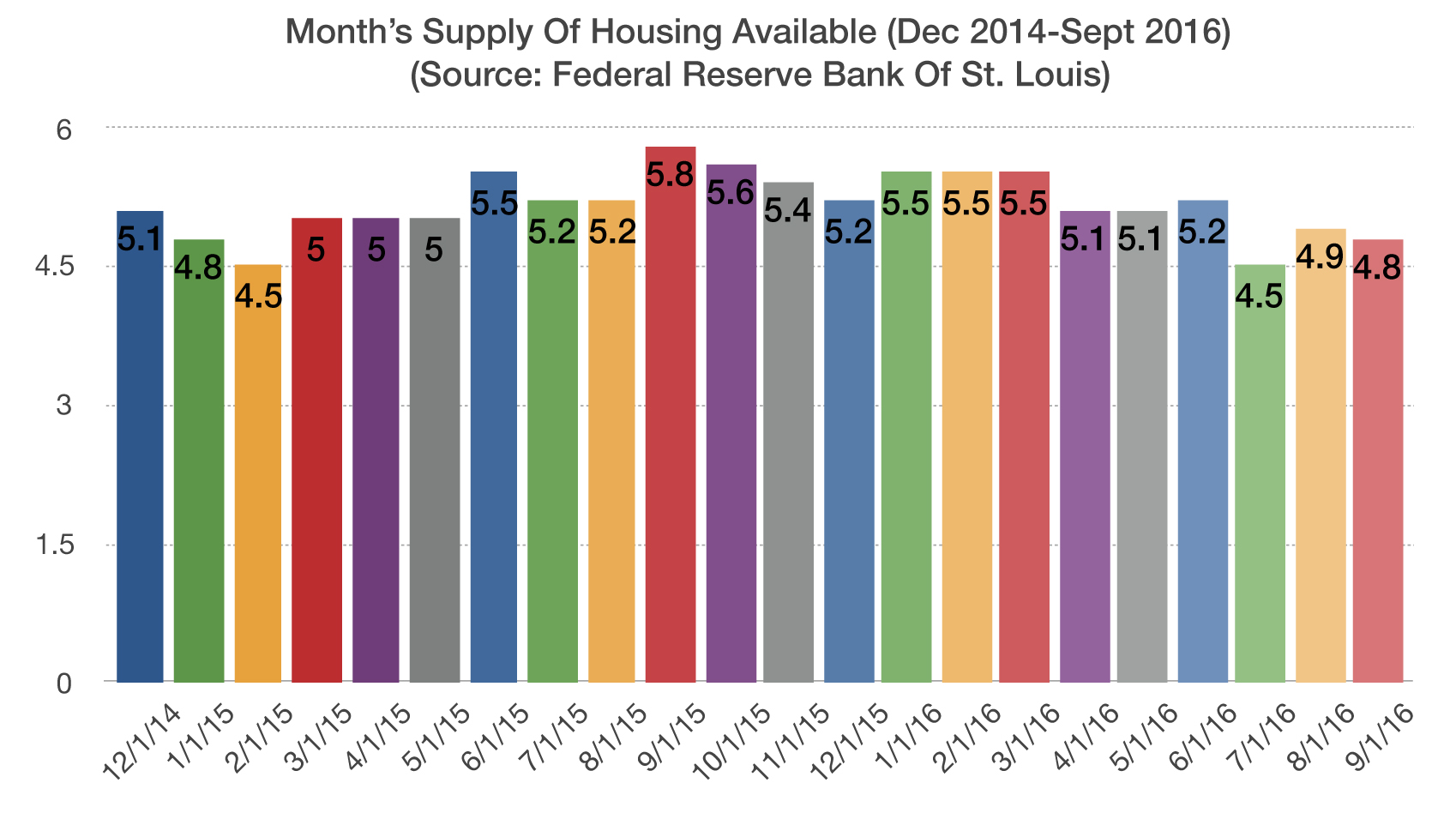

Macro Overview

Pre-election jitters led to market stagnation as equities struggled through October. With this extraordinary political year coming to a close, the results of the election will carry over to 2017 as markets digest new policies and legislative changes.

It has been eight years since the financial crisis climaxed in the fall of 2008 when tremendous uncertainty and pessimism lurked throughout the markets. Today, the stimulus efforts that were set into motion by the Fed are for the most part still in effect. Many agree that the markets today are far less precarious than they were in 2008, yet the Fed’s stimulus efforts have yielded minimal, if any, sustainable economic growth.

A topic of contention during the election was how to tax profits of large U.S. companies with overseas operations. About 50 U.S. companies account for $1.7 trillion of the $2.9 trillion of profits held overseas. So for every product a U.S. multi-national such as Apple, GE, or Microsoft sells in another country, any profits made are taxed when the money is brought back to into the U.S.

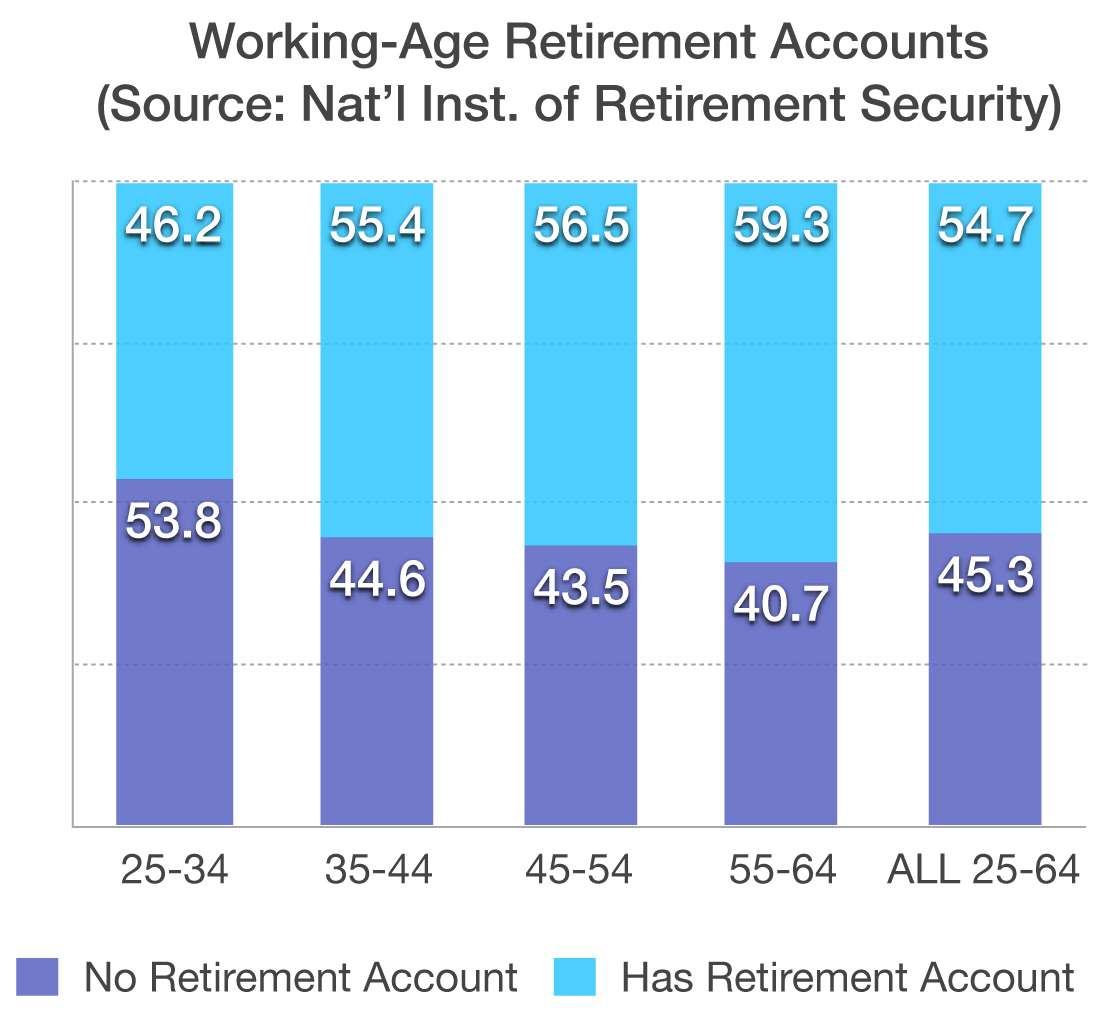

A research report released by the National Institute on Retirement Savings identified that working individuals are actually trying to save more as they approach retirement, while spending less at the same time. This is counterintuitive to what the Fed was hoping for as part of its stimulus efforts. (Sources: Fed, National Institute on Retirement Savings)

Election Day Trivia – Historical Note

During the mid 1800’s, the United States was mostly an agricultural society whose citizens were farmers and field workers. Since the country was very much a religious nation, voting day was established in the middle of the week, allowing citizens time to travel to and from polling places without interfering with Sunday religious services. Ample time was needed to travel because horse and buggy was the only form of travel.

Since farmers had such an influence over society and lawmakers, November was designated as the most convenient month for farmers and rural workers to travel to the polls. The fall harvest was over and throughout most of the nation the weather was still mild enough to allow travel over dirt and makeshift roads.

The right to vote wasn’t extended to all citizens for decades. In 1870, the 15th Amendment removed the restriction of race and color from voting. Women gained the right to cast ballots in 1920 with the ratification of the 19th Amendment. For decades, the minimum age to vote was 21, until the 26th Amendment took effect in 1971 granting voting rights to 18 year olds. (Source: U.S. National Archives)