Michael McCormick

5 West Mendenhall, Ste 202 | Bozeman, MT 59715

406.920.1682 mike@mccormickfinancialadvisors.com

Sustainable Income Planning | Investments | Retirement

Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Dear Friends,

Masks on (except for distanced selfies)!

As of this writing, I haven’t gotten the virus yet (knock on wood, salt over shoulder, etc.), but I know a lot of good people that have. Somedays it feels like a game, other days it feels like a Twilight Zone episode. All days are a lesson in managing risk. And like investing, each decision is calculated, but uncertain. Some activities can be avoided, but living a life of purpose requires taking on at least some risk, even during normal times. One of the risks that I am willing to assume is continuing to donate my time to coach youth sports. This past Fall I helped out with the running club and this winter I hope to coach kids for BSF Nordic. Being around middle schoolers makes me laugh, and when they work hard as a team it’s magical. Hopefully we can pull it off safely!

It’s Going to be OK – for those on the upper leg of the ‘K’

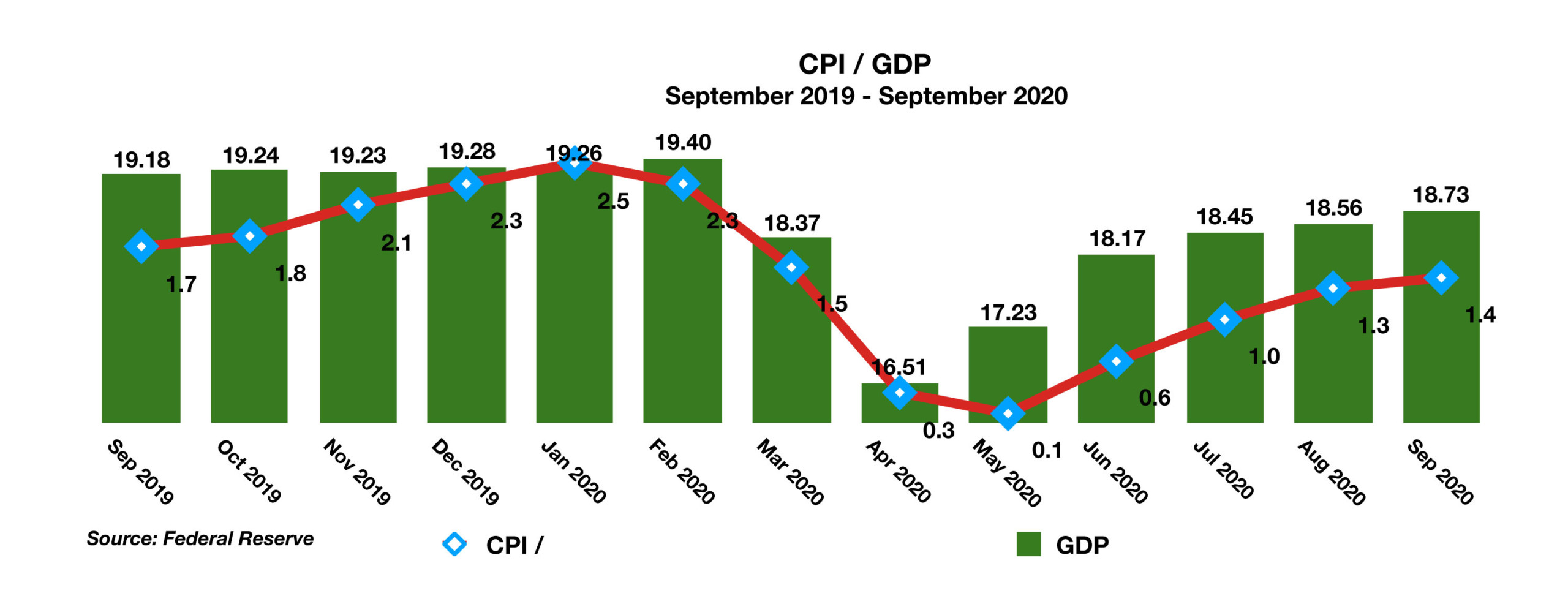

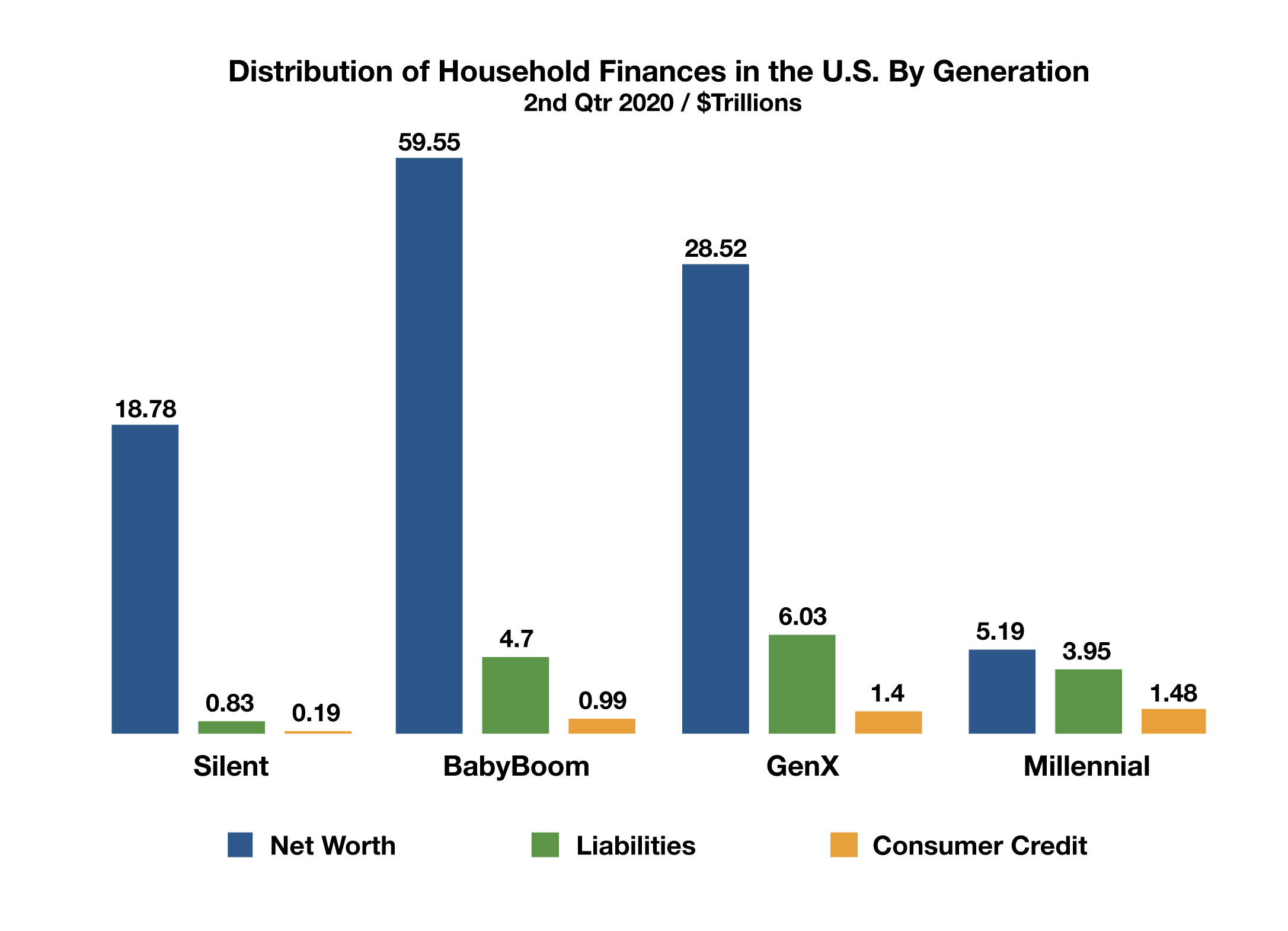

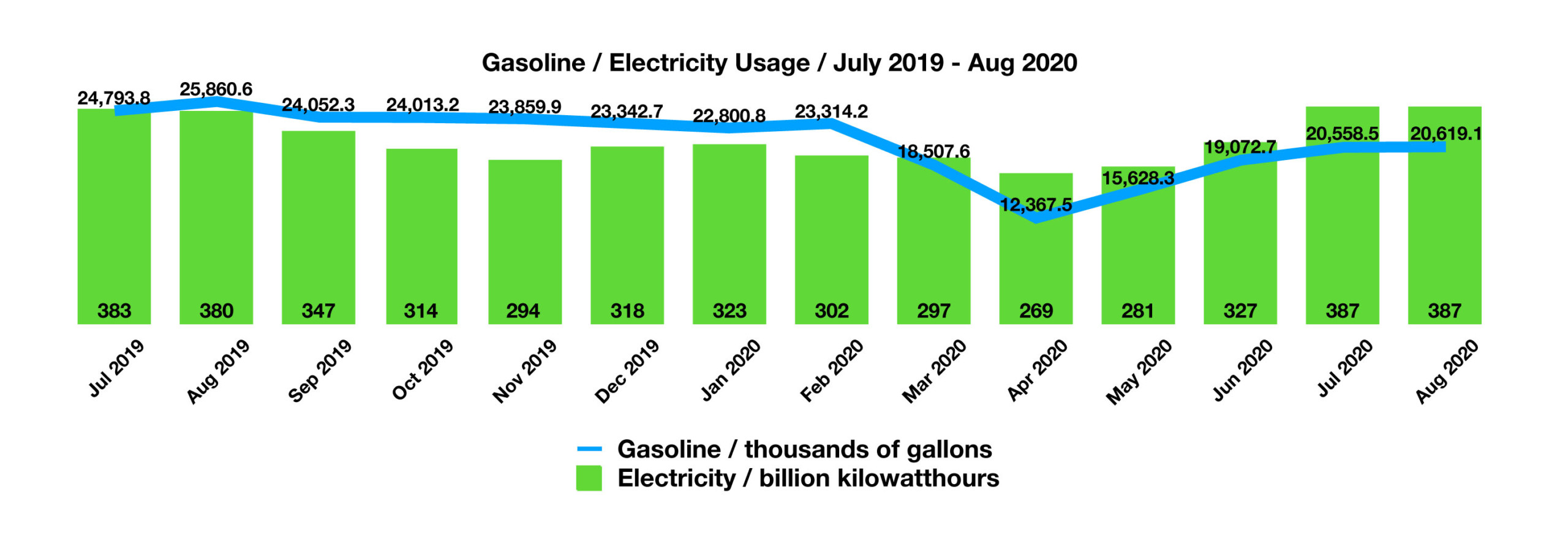

When economists talk about a ‘K’ shaped recovery, they mean that there are people on the lower leg who are really suffering, while others are doing just fine. COVID-19 has brought about possibly some of the largest shifts in consumer trends ever, as demand for online shopping, eating out, and energy consumption have dramatically changed in a matter of months. Gasoline usage cratered as electricity usage simultaneously soared, the result of millions of workers transitioning to home based offices. It sure seems that a vaccine is on its way, but many of these trends will persist. Against the backdrop of a changing political landscape there is much to be wary of.

We believe that over time stocks and real estate will continue their gains, somewhat irrespective of normal valuation metrics (e.g. stay expensive). Here are a few tips that might help you weather this long dark stretch on our way to the light: pay down debt rather than invest in bonds or CD’s. keep your retirement accounts exposed to stocks, and overweight your normal savings. The market has never been this high before, and that’s a good thing. It’s supposed to go up!

Cybersecurity is getting easier with password managers like ‘Last Pass’. I’ve used the free version of this app and found it to work well. Imagine, only having to remember ONE password and having all of your payment information secure as well. Save yourself from a possible digital catastrophe and please make this a family effort over the holiday.

Sincere wishes of peace, health, and optimism.

-Mike

Save up to $10,000 on your Montana Taxes with the Montana Endowment Tax Credit

Save up to $10,000 on your Montana Taxes with the Montana Endowment Tax Credit