Stock Indices:

| Dow Jones | 40,669 |

| S&P 500 | 5,569 |

| Nasdaq | 17,446 |

Bond Sector Yields:

| 2 Yr Treasury | 3.60% |

| 10 Yr Treasury | 4.17% |

| 10 Yr Municipal | 3.36% |

| High Yield | 7.69% |

YTD Market Returns:

| Dow Jones | -4.41% |

| S&P 500 | -5.31% |

| Nasdaq | -9.65% |

| MSCI-EAFE | 12.00% |

| MSCI-Europe | 15.70% |

| MSCI-Pacific | 5.80% |

| MSCI-Emg Mkt | 4.40% |

| US Agg Bond | 3.18% |

| US Corp Bond | 2.27% |

| US Gov’t Bond | 3.13% |

Commodity Prices:

| Gold | 3,298 |

| Silver | 32.78 |

| Oil (WTI) | 58.22 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 142.35 |

| Canadian /Dollar | 0.72 |

Macro Overview

Investment markets in September were pressured by concerns over a second wave of infections heading into the fall, election uncertainties, and wavering economic indicators.

Equities paused their upward trajectory in September, with technology stocks retreating from their highs. Uncertainty surrounding vaccine deployment and the election are expected to influence market momentum and investor confidence. Election results will help provide clarity on the direction of fiscal policy and social program funding.

A growing number of pharmaceutical companies, universities, and biotechnology firms are introducing and testing various forms of vaccines to combat COVID-19. According to the Regulatory Affairs Professional Society (RAPS), there are currently over 40 COVID-19 vaccines in trial phases worldwide.

California became the first state to require that all new autos sold be zero-emission by 2035. The executive order issued by the state’s governor is expected to reverberate throughout the country, potentially leading other states to follow suit.

The Centers for Disease Control and Prevention (CDC) issued detailed guidance for this year’s Halloween season. This guidance includes advice to refrain from substituting a costume mask for a cloth mask, avoid crowded costume parties and indoor haunted houses, and refrain from traditional door to door trick-or-treating.

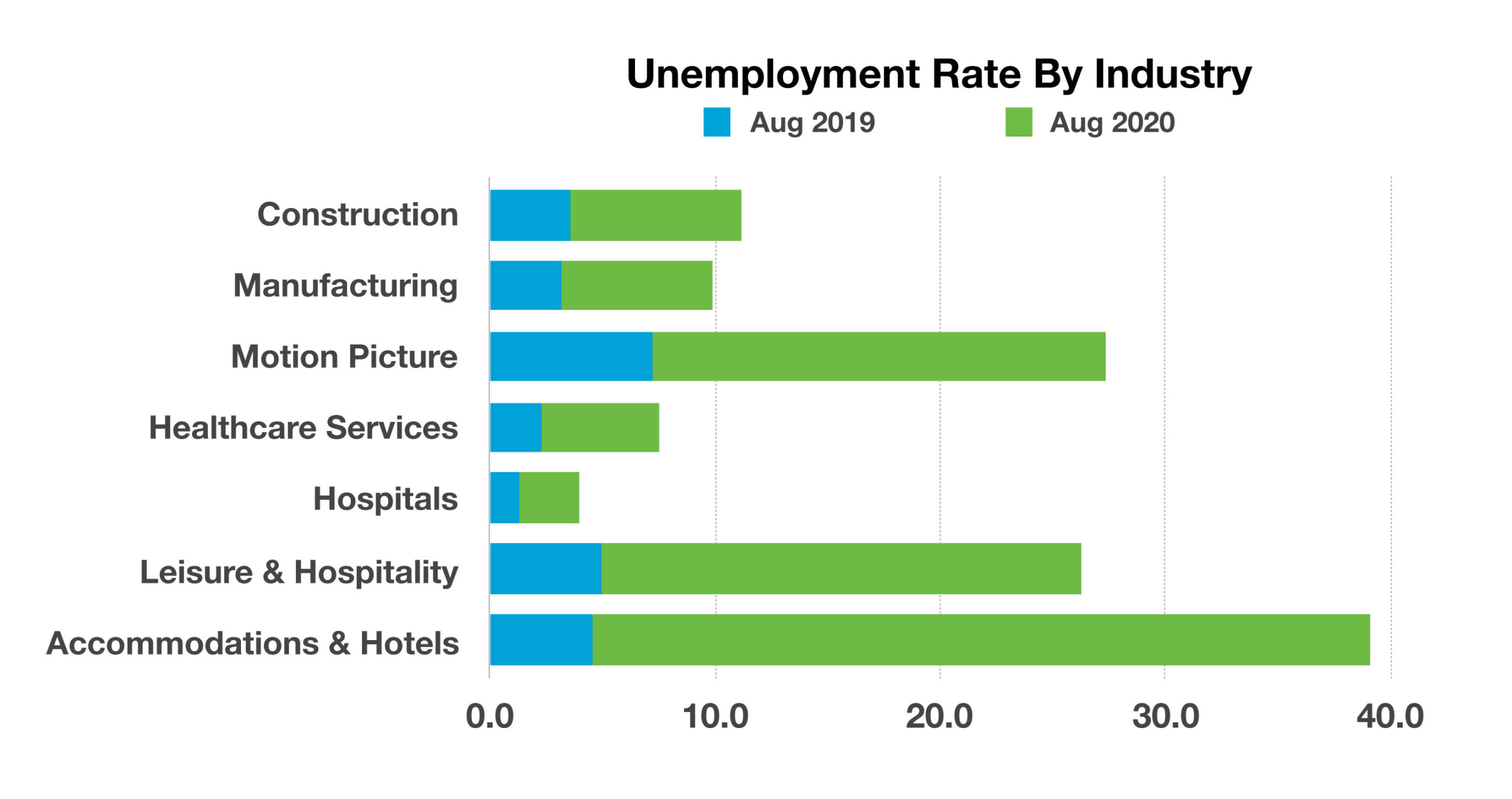

With some schools resuming across the country, the CDC reported that COVID-19 cases occurring with individuals 19 years of age and younger have risen three-fold since May. The large increase may suggest that younger people may play an increasingly important role in community transmission, even if their risk of serious illness is low relative to the older population. The threat of a second wave of infections brought about by COVID-19 has been compared to the fall of 1918, when the second wave of the Spanish flu pandemic was more severe than the first.

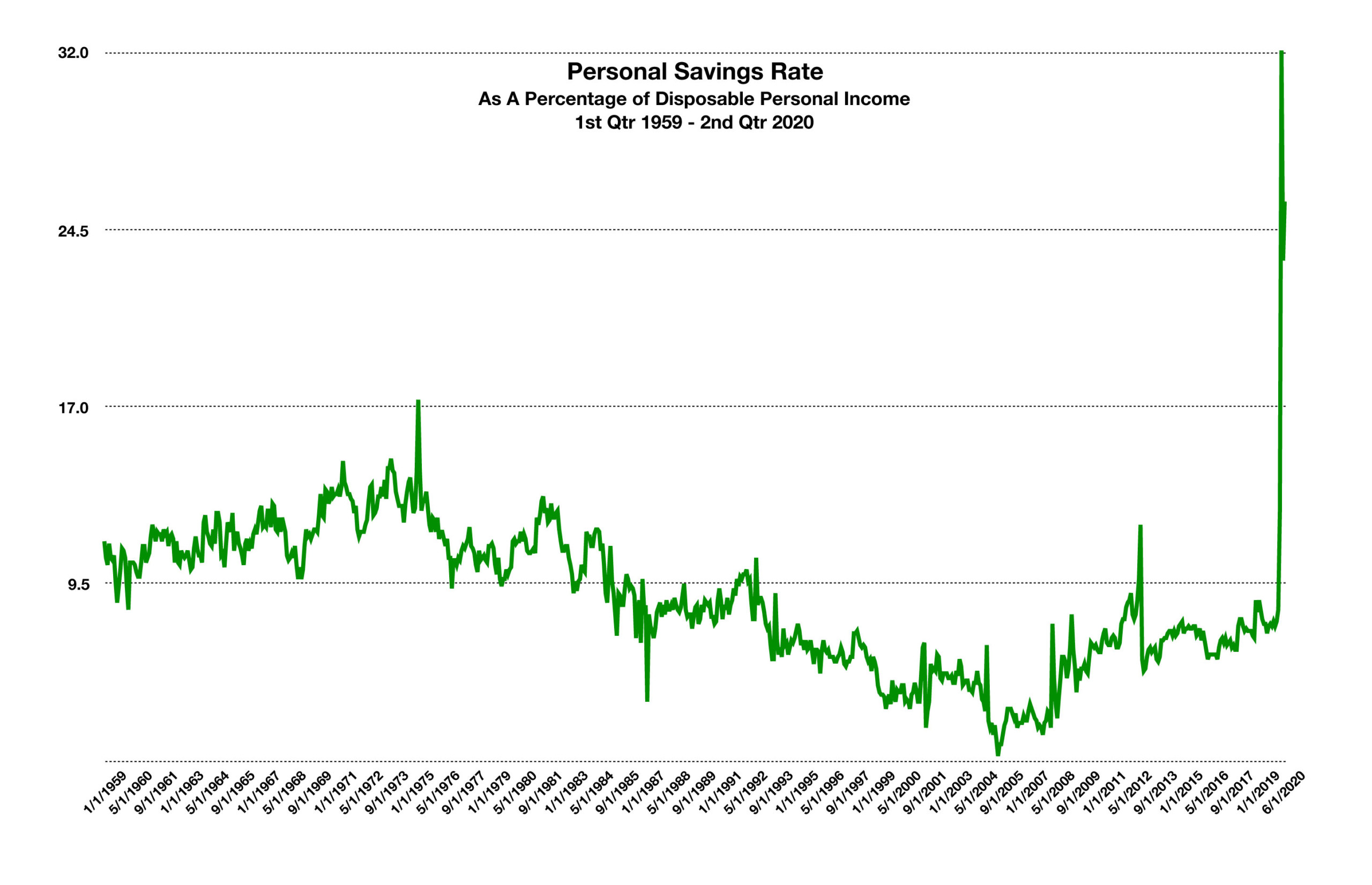

Comments by Fed Chairman Jerome Powell indicated that additional aid to small businesses and unemployed individuals was critical for economic expansion during the pandemic. The Fed Chair urged for the passage of a second stimulus package, which has been delayed due to a Congressional impasse.

Banks and other financial firms are imposing increasingly stringent standards for consumer and business borrowers, as noted by the Fed’s Senior Loan Officer Survey. The survey identified reductions in credit card limits, as well as tougher qualifications for auto and home loans. (Sources: www.cdc.gov/coronavirus/2019/html#halloween, CDC, Federal Reserve, World Bank, www.gov.ca.gov/2020/09/23/governor-newsom)

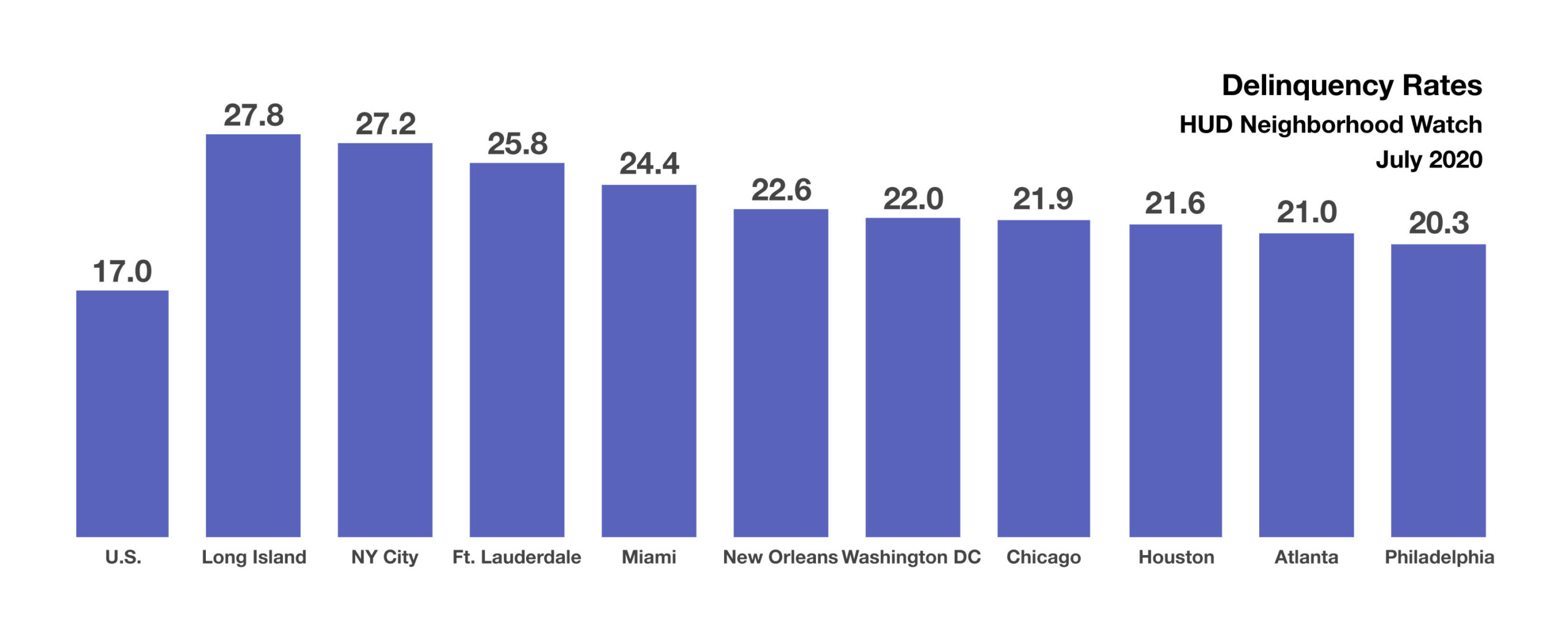

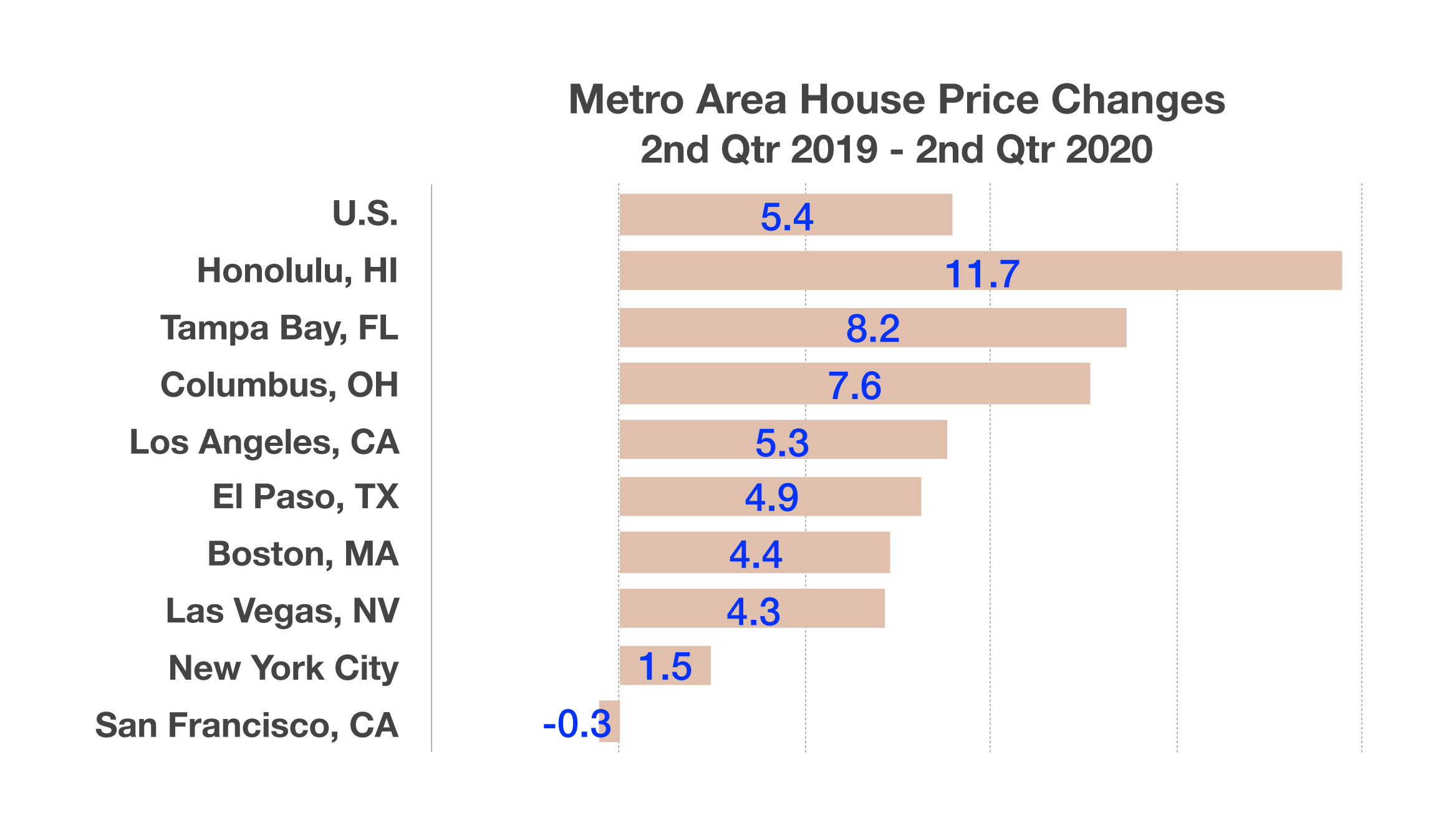

According to the Mortgage Bankers Association, roughly 3.5 million home loans were in forbearance as of September 6th, representing 7.01% of all FHA-insured loans. It is expected that millions of homeowners on forbearance will become delinquent on those loans by the end of 2020, including many homeowners who have not made a payment since March of this year. Another government housing entity, the U.S. Department of Housing and Urban Development (HUD) tracks loans in delinquency via its Neighborhood Watch list. The data reported that 17% of all FHA-insured loans were delinquent in July of this year. The figure includes mortgages in forbearance as well as those not in forbearance.

According to the Mortgage Bankers Association, roughly 3.5 million home loans were in forbearance as of September 6th, representing 7.01% of all FHA-insured loans. It is expected that millions of homeowners on forbearance will become delinquent on those loans by the end of 2020, including many homeowners who have not made a payment since March of this year. Another government housing entity, the U.S. Department of Housing and Urban Development (HUD) tracks loans in delinquency via its Neighborhood Watch list. The data reported that 17% of all FHA-insured loans were delinquent in July of this year. The figure includes mortgages in forbearance as well as those not in forbearance.