Stock Indices:

| Dow Jones | 48,977 |

| S&P 500 | 6,878 |

| Nasdaq | 22,668 |

Bond Sector Yields:

| 2 Yr Treasury | 3.38% |

| 10 Yr Treasury | 3.97% |

| 10 Yr Municipal | 2.49% |

| High Yield | 6.55% |

YTD Market Returns:

| Dow Jones | 1.90% |

| S&P 500 | 0.49% |

| Nasdaq | -2.47% |

| MSCI-EAFE | 9.93% |

| MSCI-Europe | 7.68% |

| MSCI-Far East | 14.80% |

| MSCI-Emg Mkt | 14.69% |

| US Agg Bond | 1.75% |

| US Corp Bond | 1.47% |

| US Gov’t Bond | 1.64% |

Commodity Prices:

| Gold | 5,296 |

| Silver | 94.38 |

| Oil (WTI) | 67.29 |

Currencies:

| Dollar / Euro | 1.18 |

| Dollar / Pound | 1.35 |

| Yen / Dollar | 156.05 |

| Canadian /Dollar | 0.73 |

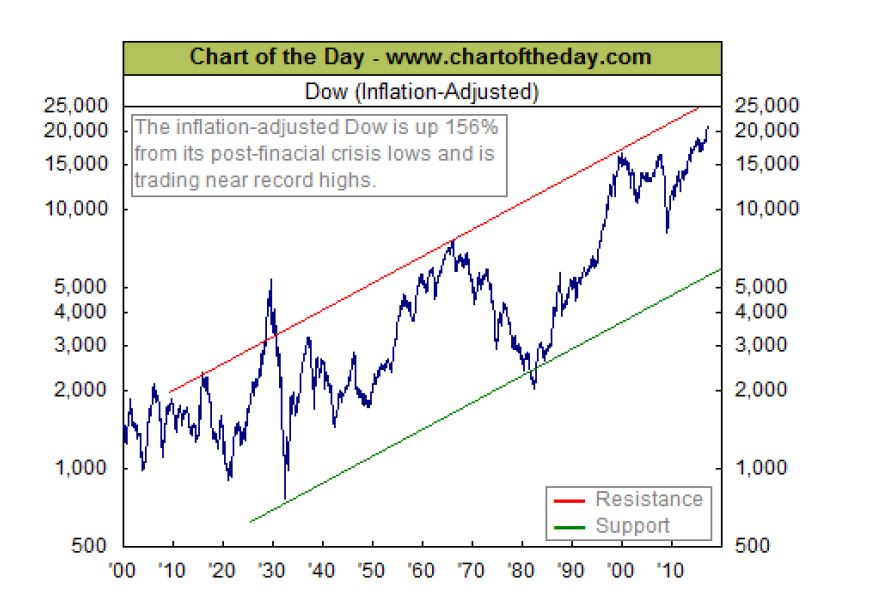

A Little More to Go For?

The chart below shows the inflation adjusted Dow has risen by 156% since the market lows in 2009. Of more interest are the trend lines (channels), which have identified the tops and bottoms over the years. The DJIA is approaching the top end of the channel, which with one exception (2000-2001), has called the top. On this chart, there is a little more to go for on the Dow. There is not a lot of room on the upside, so we would look at this as an early warning signal that the big cap/blue chip part of the market is pricing in a lot of good news. An example is Apple, which announced $210 billion in share buybacks over the next two years and the stock fell after the news. Buy the rumor, sell the news. Sell in May and go away. Bulls make money, bears make money, pigs don’t.

International Allocation

The uncertainty regarding the French elections was removed with the victory by Emmanuel Macron over Marine Le Pen. The Macron win probably sets up at least one year of clear sailing from a political viewpoint- no Hollande, some French reform, Merkel looks safer in Germany and there is time to sort out Italy/Spain. The Brexit negotiation with the UK may not go smoothly, but we doubt the markets will price a negative outcome for another twelve months. Meanwhile, business is pretty good in Europe. So the breakout pattern which has appeared in European equities and their outperformance vs. U.S. stocks may well accelerate with the Macron win. Shamrock’s tactical strategy will be adding exposure back to European equities. It is important to remember that the recovery in the Eurozone is only 3 years old, interest rates are zero, and the European and Japanese central banks are still buying bonds to promote growth. The Eurozone feels like the U.S. in 2012-2013 and thus we believe European economy is picking up momentum.