Derek J. Sinani

Founder/Managing Partner

derek@ironwoodwealth.com

7047 E. Greenway Parkway, Ste. 250

Scottsdale, AZ 85254

480.473.3455

Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Macro Overview

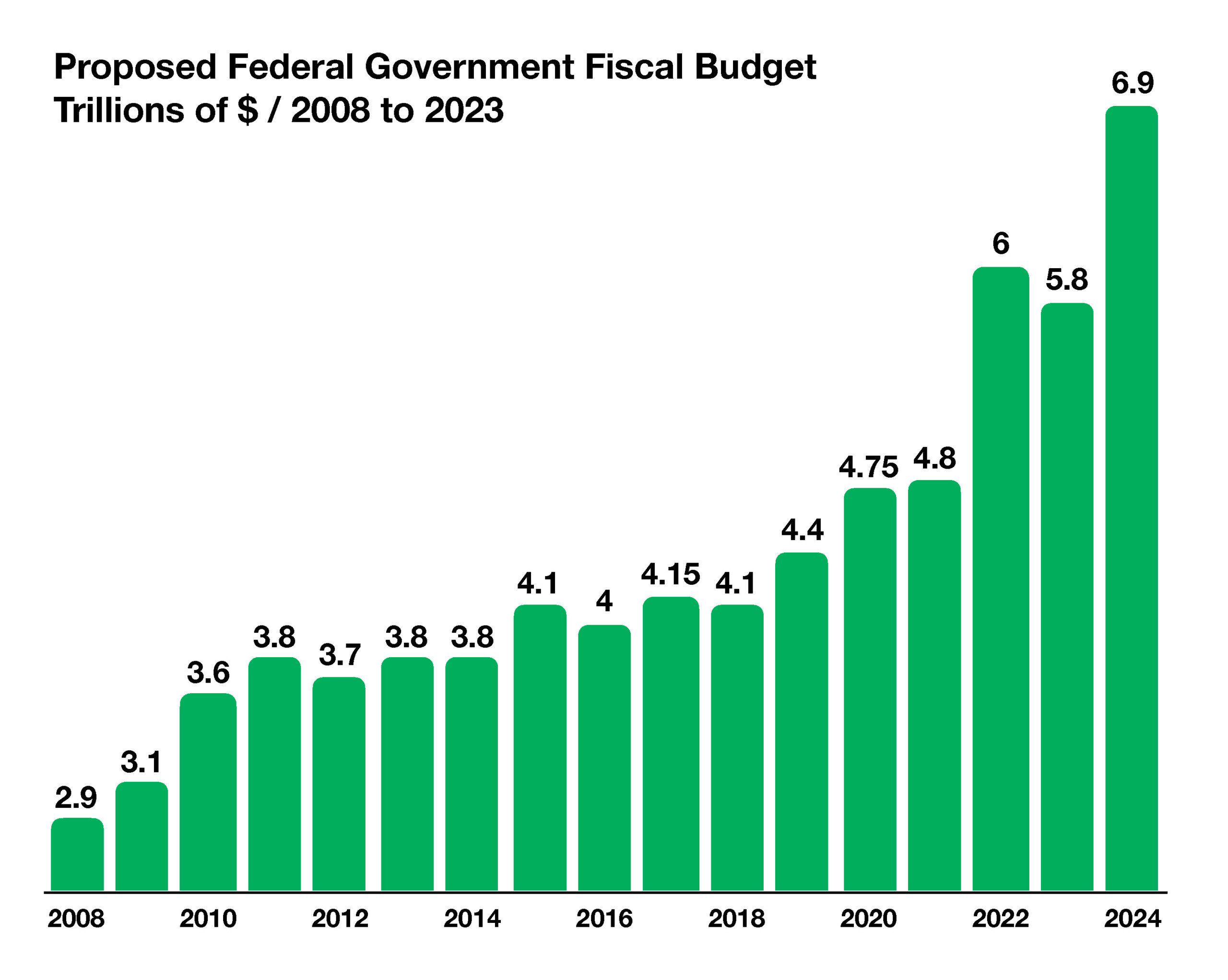

Congress is spending the bulk of September deliberating over the Federal Budget for fiscal year 2024 as a looming deadline on September 30th approaches. Should an agreement not be reached, a government shutdown could occur. The $6.9 trillion proposed budget encompasses 438 agencies and 15 executive branches of the Federal Government.

The last Federal Government shutdown lasted 35 days, from Dec. 22nd, 2018, until Jan. 25th, 2019, making it the longest Federal Government shutdown in history. Hardline republicans may dig their heels in during the deliberations – adding additional market volatility this month.

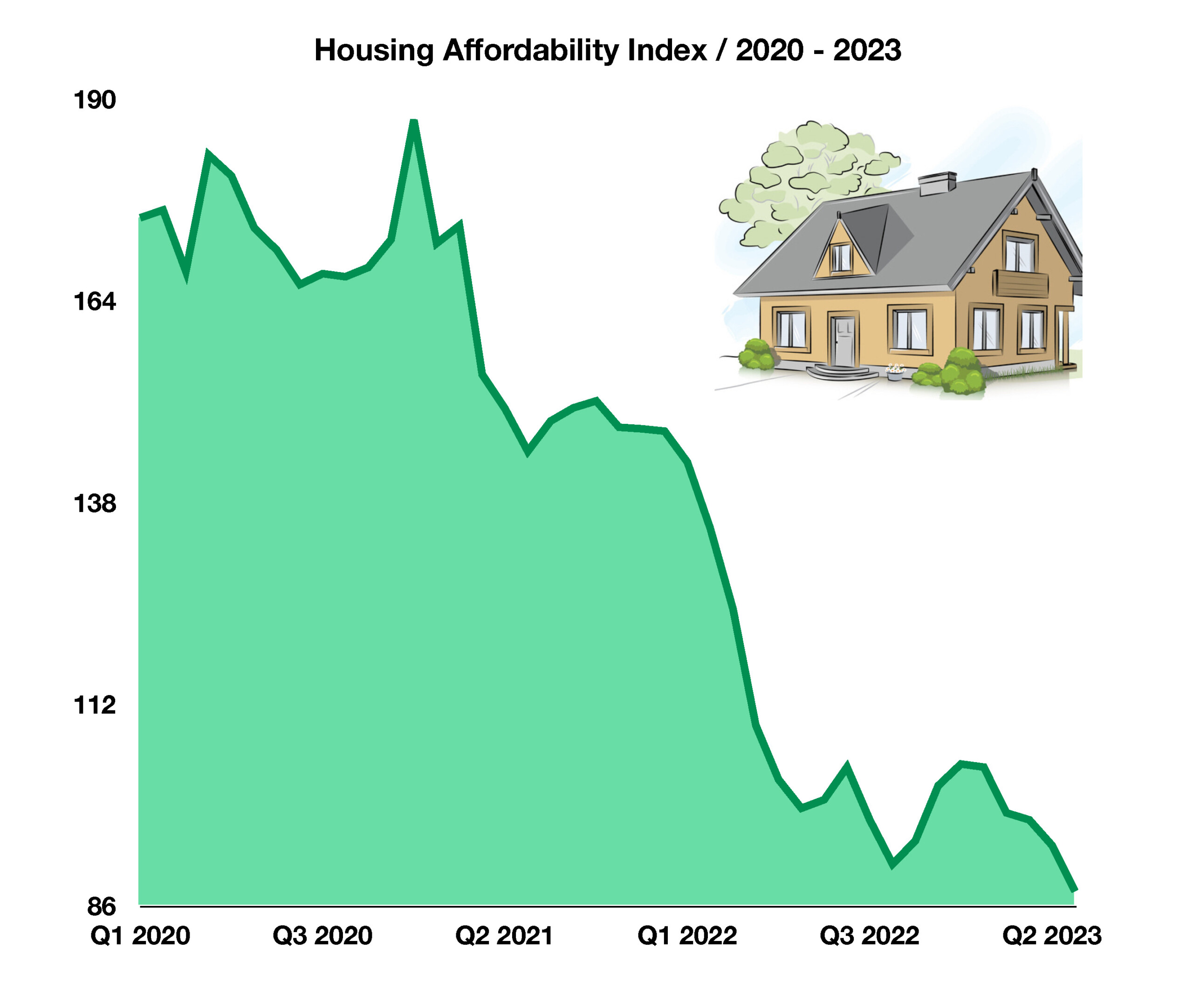

The 30-year fixed mortgage rate fell to 7.18% in August, after reaching a 23-year high of 7.23%. The housing market resiliency has been questioned by many analysts and economists, as elevated home prices continue to make purchases unaffordable for millions of Americans. Apartment and residential rental costs are starting to decline in various areas of the country. These trends positively impact the “rents” component of the government’s CPI gauge (consumer price index) – further evidence that we have entered a welcomed disinflationary environment.

Equities retracted in August as earnings estimates and lingering inflation concerns held stocks back. Supply constraints that existed a year ago have essentially vanished, yet have led many companies to explore new sourcing locations and domestic facilities. China, the world’s largest exporting country, is showing signs of a possible economic contraction, whose silver-lining is the exportation of deflationary prices to the US.

Petroleum production cuts by OPEC and other oil-producing countries propelled oil and gasoline prices higher in August – which will likely add upward pressure to the August 13th inflation report = potentially adding downside pressure to the overall stock market. Other factors affecting oil prices as fall approaches include seasonality, demand, and supply constraints. Oil ended August at $83.60 per barrel, yet still lower than the recent highs of over $120 per barrel in June 2022.

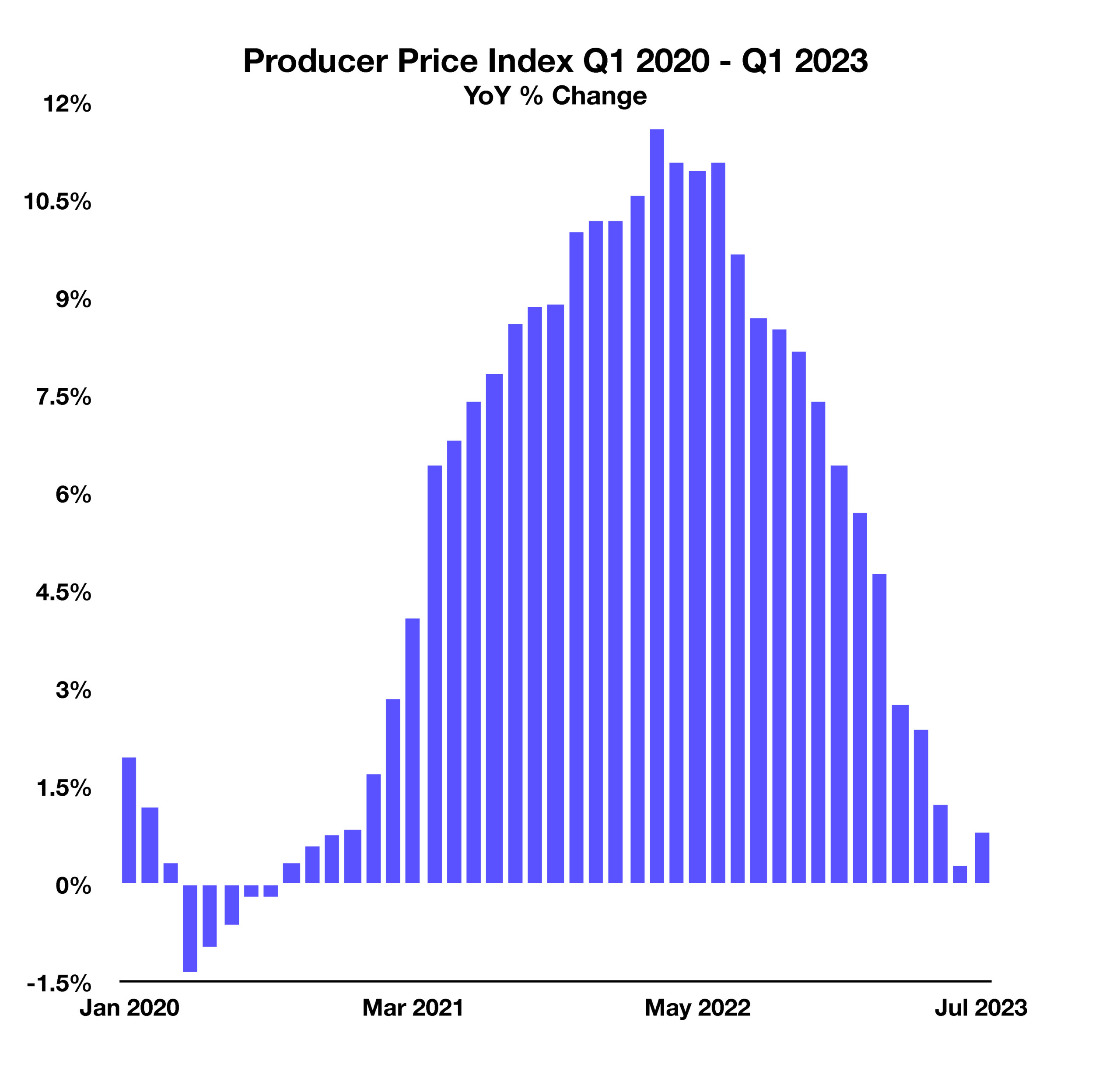

The Producer Price Index (PPI) measures the selling prices domestic companies receive when purchasing everything from raw materials to products themselves. Similar to how the Consumer Price Index (CPI) tracks prices consumers pay for goods, the PPI tracks prices that corporations pay.

The Producer Price Index (PPI) measures the selling prices domestic companies receive when purchasing everything from raw materials to products themselves. Similar to how the Consumer Price Index (CPI) tracks prices consumers pay for goods, the PPI tracks prices that corporations pay.