Stock Indices:

| Dow Jones | 42,270 |

| S&P 500 | 5,911 |

| Nasdaq | 19,113 |

Bond Sector Yields:

| 2 Yr Treasury | 3.89% |

| 10 Yr Treasury | 4.41% |

| 10 Yr Municipal | 3.31% |

| High Yield | 7.26% |

YTD Market Returns:

| Dow Jones | -0.64% |

| S&P 500 | 0.51% |

| Nasdaq | -1.02% |

| MSCI-EAFE | 17.30% |

| MSCI-Europe | 21.20% |

| MSCI-Pacific | 10.50% |

| MSCI-Emg Mkt | 8.90% |

| US Agg Bond | 2.45% |

| US Corp Bond | 2.26% |

| US Gov’t Bond | 2.44% |

Commodity Prices:

| Gold | 3,313 |

| Silver | 33.07 |

| Oil (WTI) | 60.79 |

Currencies:

| Dollar / Euro | 1.13 |

| Dollar / Pound | 1.34 |

| Yen / Dollar | 144.85 |

| Canadian /Dollar | 0.72 |

Macro Overview

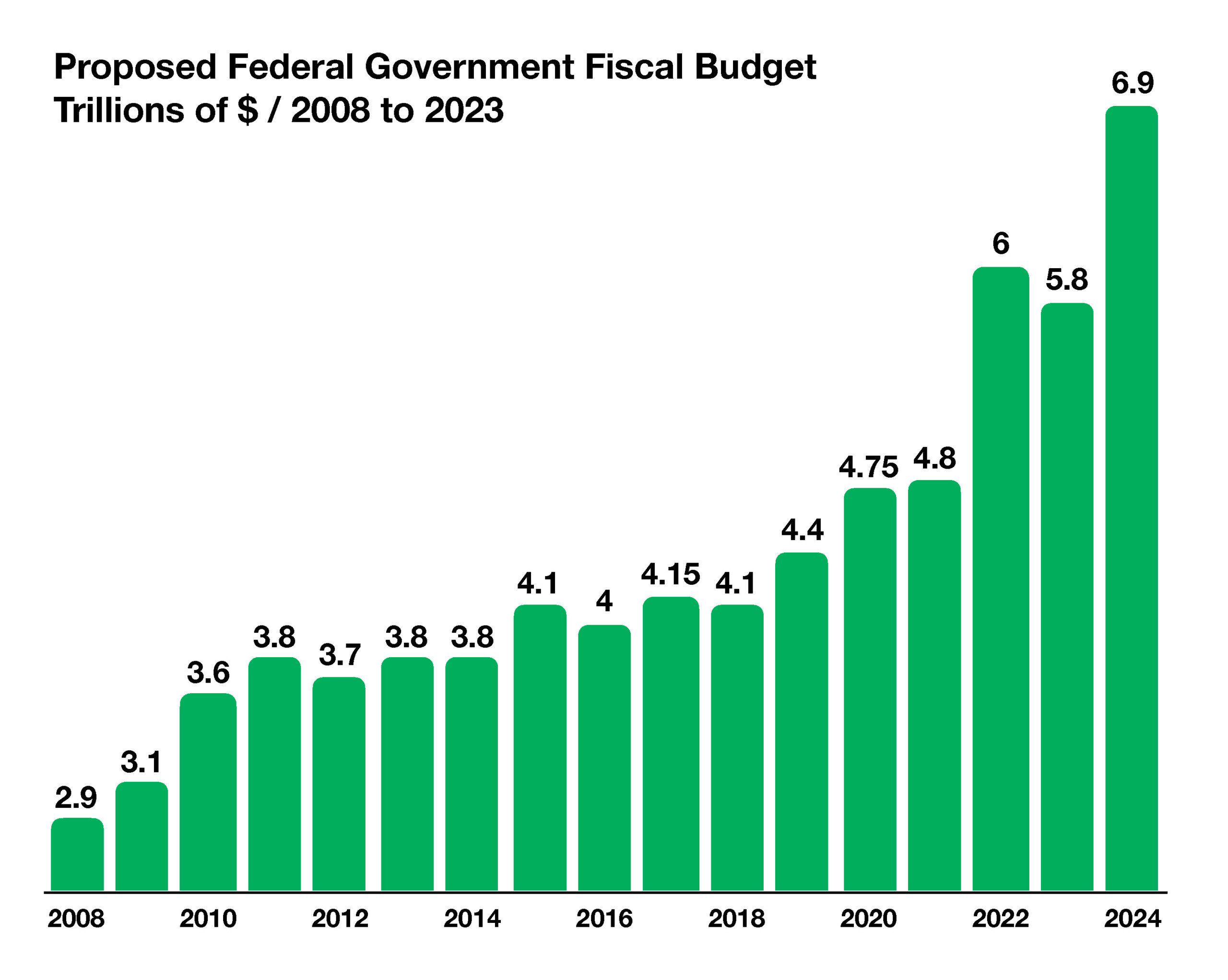

Congress is deliberating over the Federal Budget for fiscal year 2024 as a looming deadline approaches on September 30th. If an agreement is not reached, then a government shutdown may occur. The $6.9 trillion proposed budget encompasses 438 agencies and 15 executive branches of the Federal Government.

The most recent Federal Government shutdown lasted 35 days, from December 22, 2018, until January 25, 2019, making it the longest Federal Government shutdown in history. Partial government shutdowns have also occurred in the past, temporarily shuttering selected federal agencies and programs.

Recently released Federal Reserve data reveals an erosion in consumer credit quality, with a particular increase in retail store credit card delinquencies. Credit card usage accounted for roughly 20% of consumer spending growth over the past year.

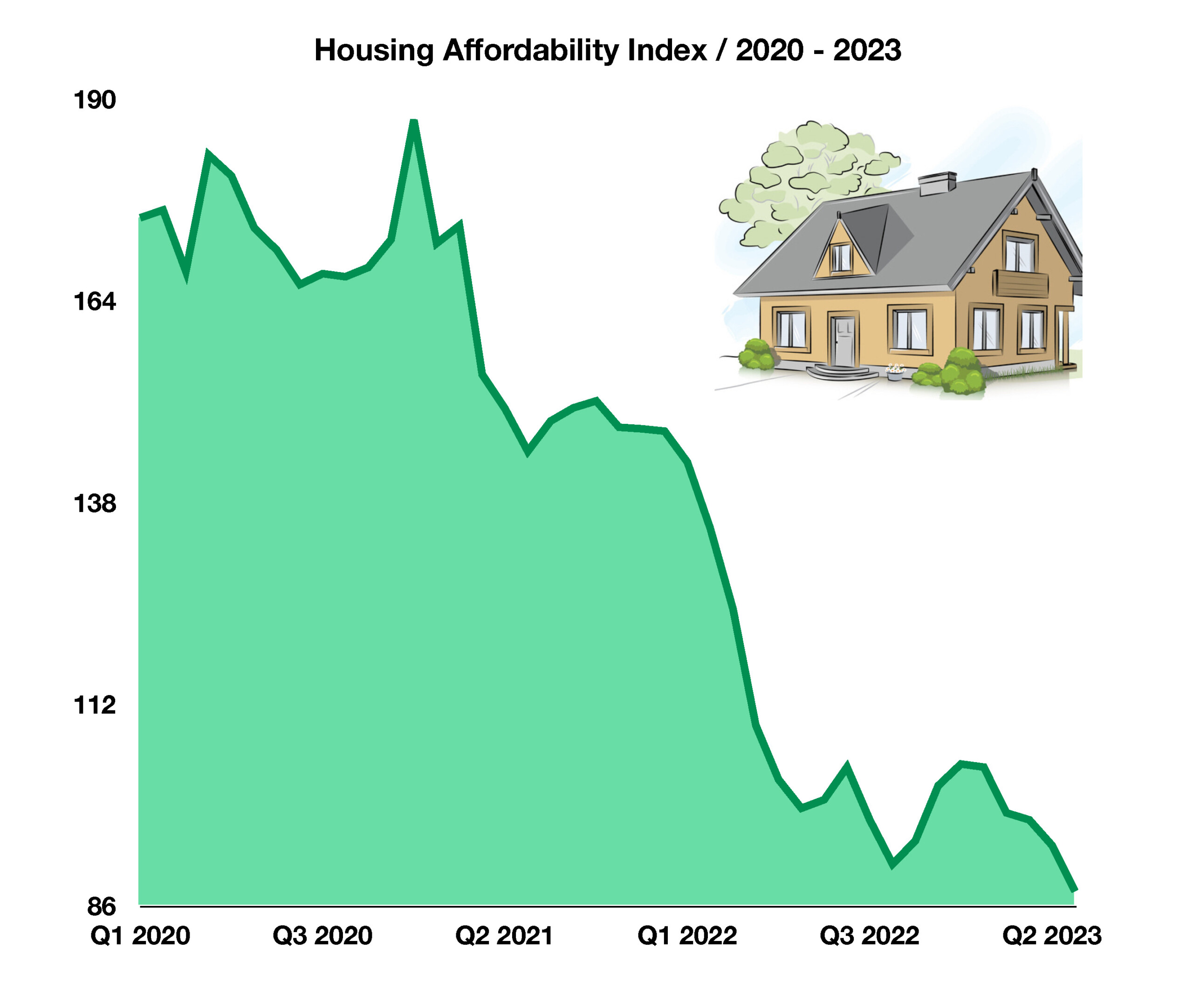

The rate on a 30-year fixed conforming mortgage fell to 7.18% in August, after reaching a 23-year high of 7.23%. Many economists increasingly question the resilience of the housing market, as elevated home prices make purchases unaffordable for millions of Americans. The cost of apartment and residential rentals are decreasing in various areas of the country, as an additional inventory of rentals comes into the market.

Equities retracted in August as cautious earnings estimates and lingering inflation risks held stocks back from advancing. Supply constraints that existed a year ago have essentially vanished, but led many companies to explore new sourcing locations and facilities. China, the world’s largest exporting country, is showing signs of a possible economic contraction, seen by analysts as a potential hindrance to global economic expansion.

Petroleum production cuts by OPEC and other oil-producing countries propelled oil and gasoline prices higher in August. Other factors affecting oil prices include seasonality, demand, and supply constraints. Oil ended August at $83.60 per barrel, lower than recent highs of over $120 per barrel in June 2022. (Sources: U.S. Congress, Federal Reserve Bank of St. Louis, IMF, Bureau of Labor Statistics, FreddieMac)

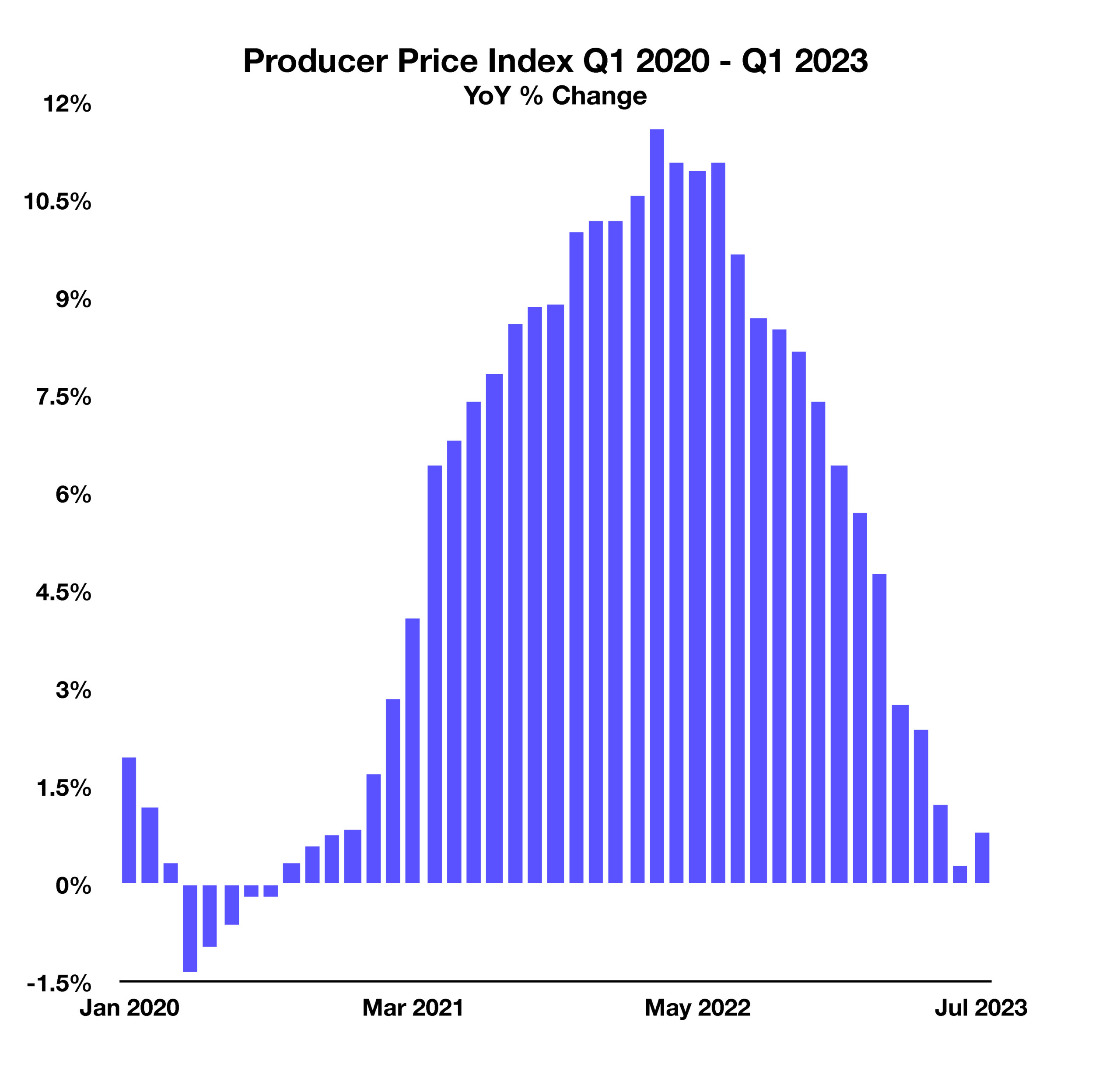

The Producer Price Index (PPI) measures the selling prices that domestic companies pay when purchasing anything from raw materials to finished products. Similar to how the Consumer Price Index (CPI) tracks prices consumers pay for goods, the PPI tracks prices for corporations.

The Producer Price Index (PPI) measures the selling prices that domestic companies pay when purchasing anything from raw materials to finished products. Similar to how the Consumer Price Index (CPI) tracks prices consumers pay for goods, the PPI tracks prices for corporations.