Many from Wall Street generally believe the U.S. is in the late stage of the economic cycle and thus can justify the high equity market prices, but they are concerned that valuations are stretched. Shamrock believes that the markets can go higher from here as long as the economy can continue to accelerate closer to 3% GDP growth rate. Economically-sensitive sectors such as materials and industrials have a big stake in this argument. And with the debate underway as to whether oil vs. renewables/electric vehicles is at the tipping point and all that means for oil prices, Saudi Arabia, OPEC, Texas, fracking, the demand side of the energy equation is more crucial than ever. Then there is the state of China’s economy.

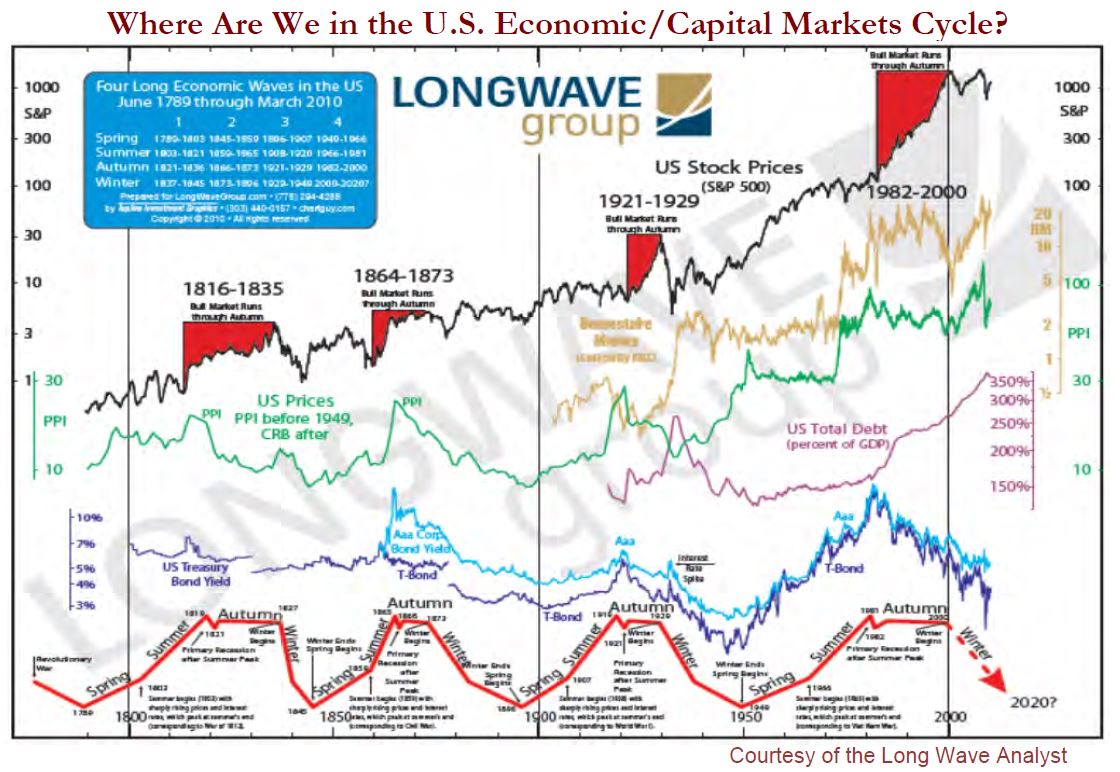

Looking at the U.S. economic cycle, one of our market strategists had us take another look at the Kondratieff cycle, that 55 – 60 year long wave, which the strategist believes, has influenced U.S., Europe and Japan for decades. (The portion of the following graph to look at is the bottom right hand corner, where the dotted line points to the year 2020.)

The Great Depression in the U.S. ran from 1929 – 1940. The years 1929 – 1932 were alleged to be the worst, though there was a second depression around 1936. It passed more quickly than the first phase, but it was the second blow which was unexpected and resulted in government social programs. The 1929 depression began when the stock market bubble popped. This is how the Kondratieff’s winter typically begins, a massive asset bubble pops. Since the banking sector at the time was almost unregulated, lending was prolific and there were almost no social safety nets in place. Thus began FDR’s establishment of the government’s safety programs for the public with Social Security, price supports for agricultural products, regulation of banks and deposit insurance.

It is claimed by some, that the U.S. economy nearly missed another depression in 2008 because of the government policy actions taken at that time. Zero percent interest rates, quantitative easing (QEs), massive fiscal spending, resulted in $8 trillion of new debt that are all cited as elements of the cure. But was the cure almost worse than the disease? Would the U.S. economy have been better off in the long run, if it was left to pretty much sort itself out? In the 1930’s experience, there is a case to be made that government policy intervention elongated the depression, which might have ended in 1932, but reappeared in 1936 – 1937.

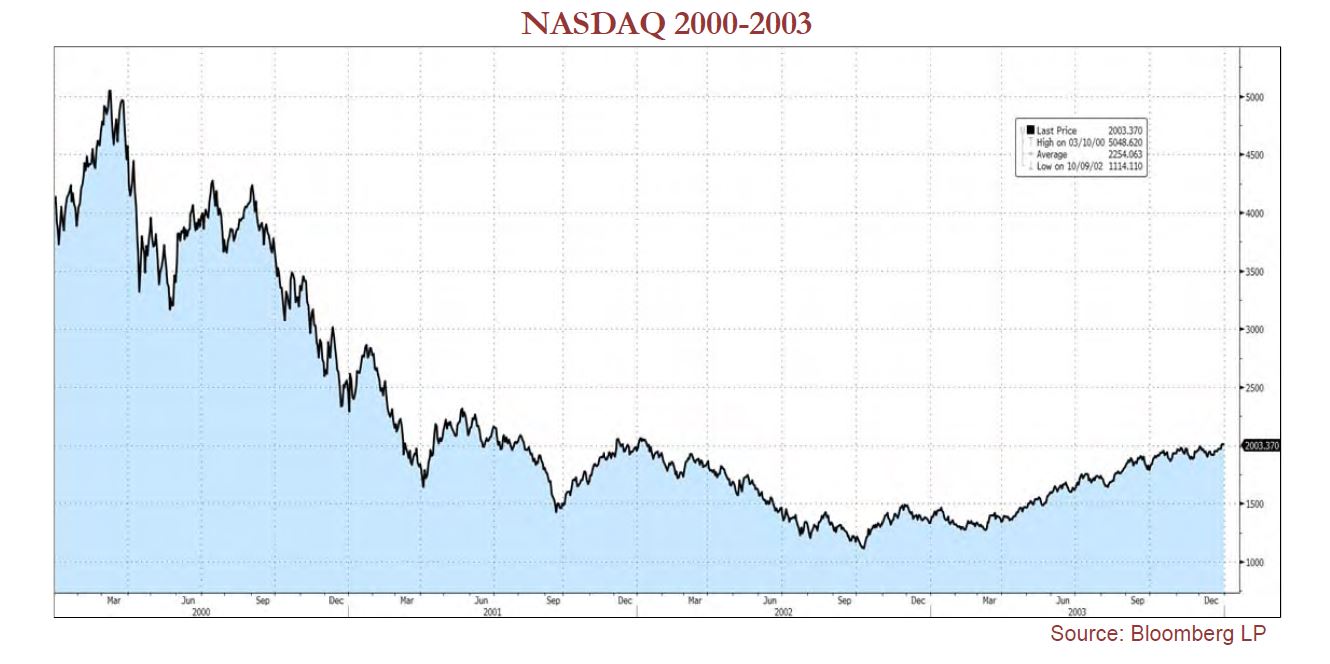

The most recent Kondratieff winter started in March 2000, when the internet bubble popped. The NASDAQ fell by 80% over the next three years, but the dagger in the economy was what happened after 9/11. After the equity market was closed for several days, the economy pretty much went straight south. Silicon Valley topped in March 2000 and the U.S. economy topped eighteen months later. The economy had a heart attack.

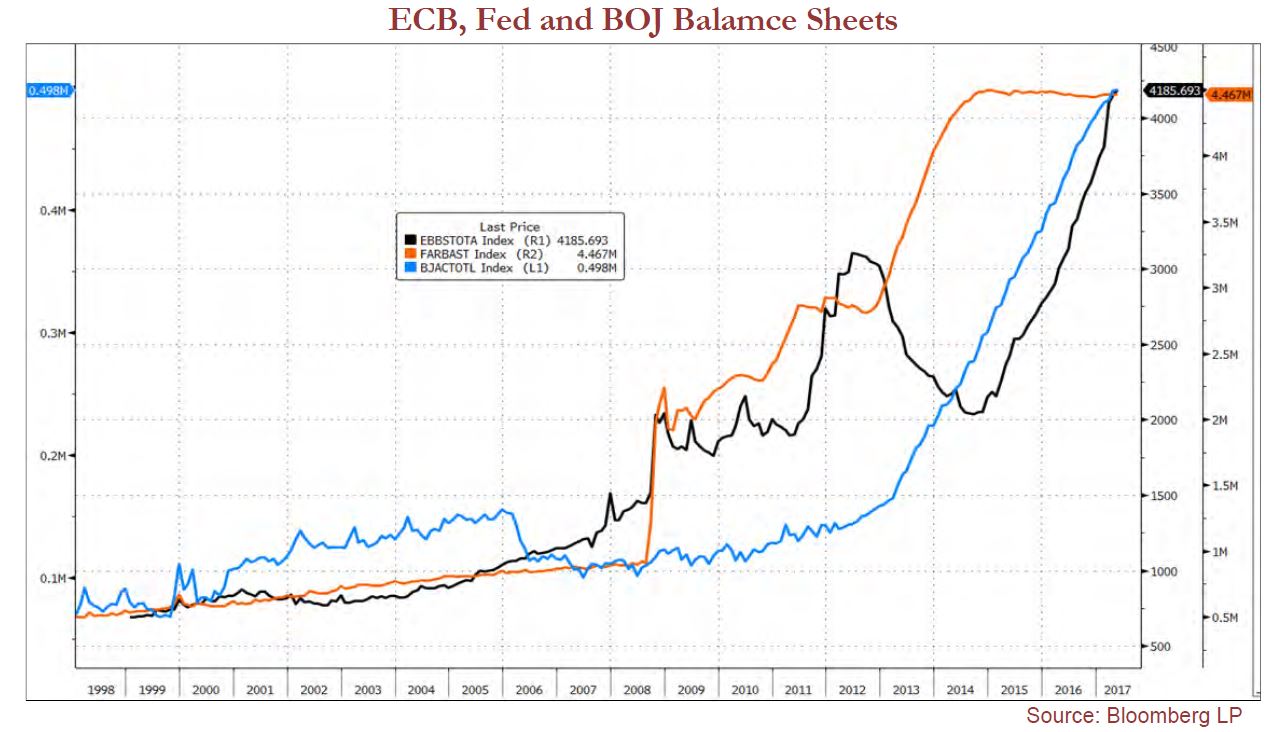

The Fed responded after 9/11, not after NASDAQ popped, making their policy turn too late. By 2003/2004, looking for assets to reflate, the Fed, banks and government agencies targeted housing as the way to stimulate the economy. So in this Kondratieff wave, the second asset bubble to pop was housing in 2008/2009. But inside the recovery of housing/the economy/stocks, lie the cure (zero percent interest rates, QEs), which are fueling the third bubble, government debt and inflated bond prices worldwide. This is not just a U.S. problem, it also exists in Japan and Europe after years of QEs, zero percent interest rates, negative rates and essentially price fixing of the government bond markets. This one is the biggest bubble of all. The balance sheets of the European Central Bank, Bank of Japan and U.S. Federal Reserve now total $13.4 trillion. But those three central banks control less than one third of their government’s outstanding bonds, leaving plenty of room for prices to move. Compared to the size of the U.S. Housing market in 2008 ($12 trillion) and NASDAQ’s market cap in 2000 (about $6 trillion), the Big 3 government bond markets are huge (potentially $30 trillion).

Within the fixed income market, there are massive derivative positions which are more sensitive to changes in interest rates. This is when the third bubble in the Kondratieff wave forms as banks try to control interest rates through derivatives. Volatile interest rate moves will significantly impact the prices of derivatives and occur in a very short time frame. Margin calls start, creating a negative loop cycle, that has led to almost every large scale market decline. Watch for margin calls!

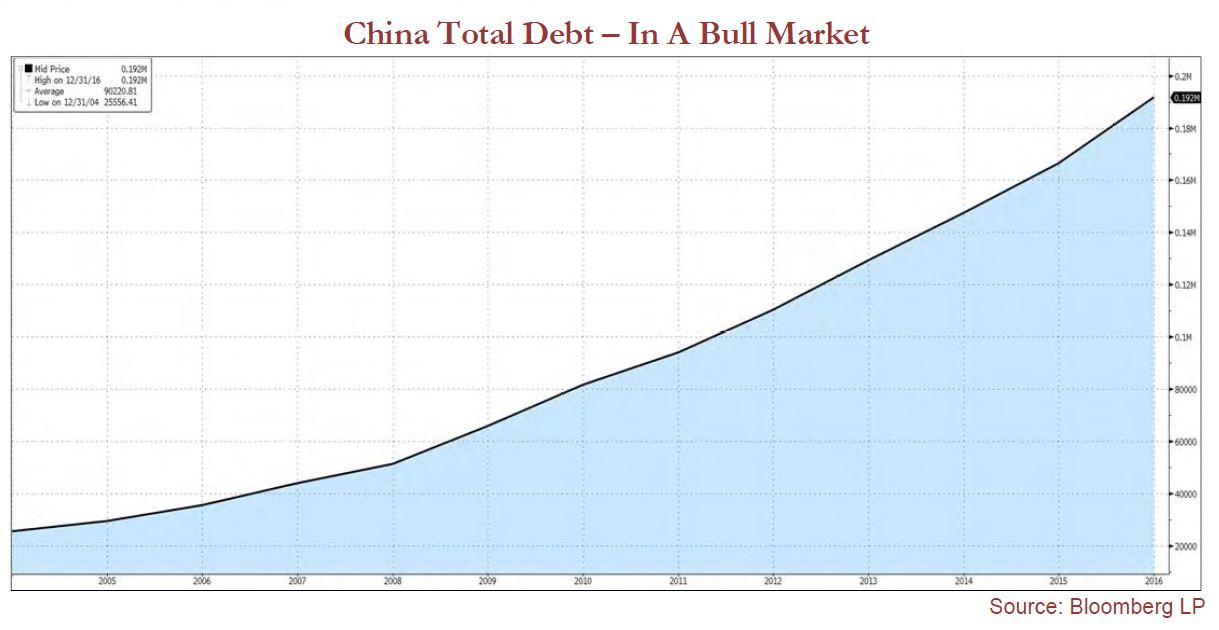

The next big asset bubble to pop could occur around 2020 as the approximate date. The margin call should occur within derivatives market. The location is most likely Europe or the U.S. The principal suspects are U.S. pension funds which have a $3.8 trillion funding shortfall, European banks with heavy derivative exposure, or China where debt is increasing at a rapid rate just to keep their economy growing.

When the next asset bubble pops, markets will decline significantly and traditional asset allocation will not protect portfolios. Investors will need to dramatically shift assets via a tactical investment strategy to cash to protect wealth until the next Kondratieff spring begins and market stability is restored.

Because cycles can last 55 to 60 years and with the cost of living increasing, investors are not able to sit in cash as they wait for the bond bubble to pop. Shamrock believes investors need not only to diversify across all asset classes but also between investment strategies. Our portfolios are designed to be invested when the markets are stable and rising in order to protect against inflationary forces. In addition, our tactical strategies have the ability to protect wealth and purchasing power during severe bear markets by reducing exposure to risk assets and raising cash in portfolios.

You Deserve the Peace of Mind……We Deliver!

The best compliments we receive are referrals to friends and family members. Help us grow by sharing our name. Your team at Shamrock hope you have a wonderful Memorial Day Weekend.